Management and Administration Rules (Rule 11-20)

Rule 11. Annual Return

(1).

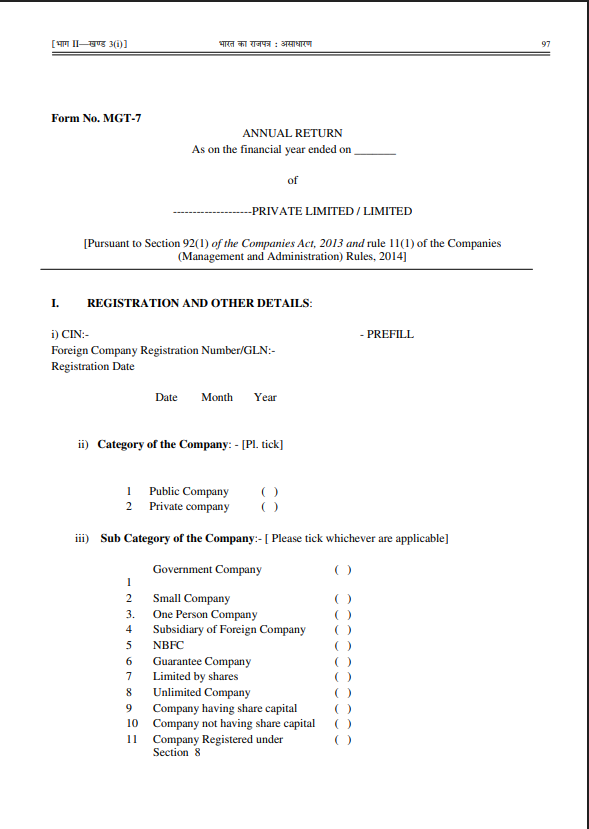

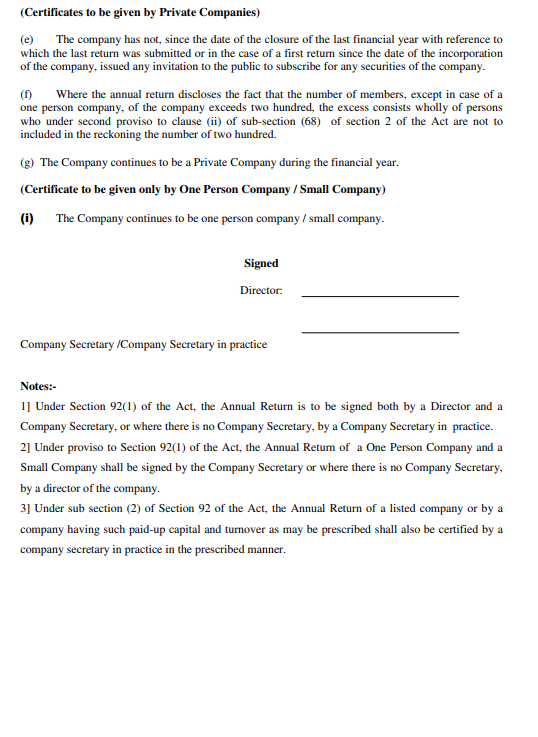

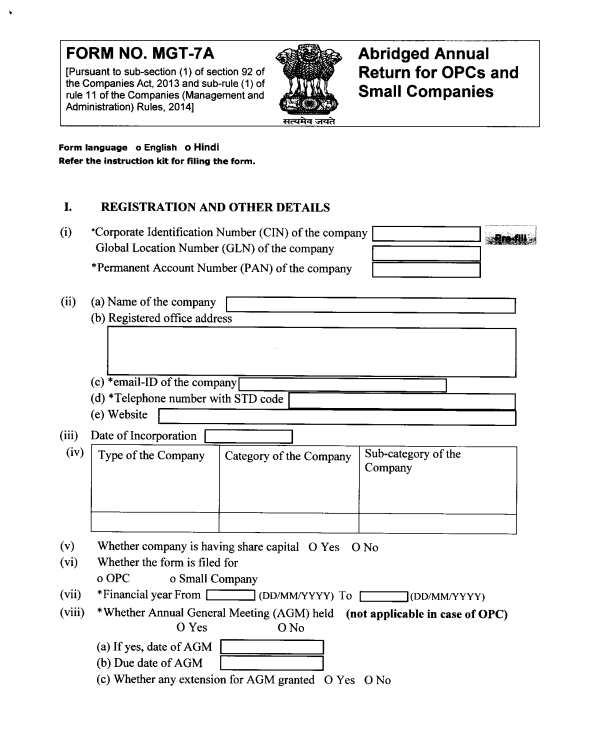

Every company must file its annual return in Form MGT-7.

One Person Companies (OPCs) and Small Companies do not file Form MGT-7.

OPCs and Small Companies must file their annual return in Form MGT-7A.

This requirement applies from the financial year 2020–21 onwards.

(2).

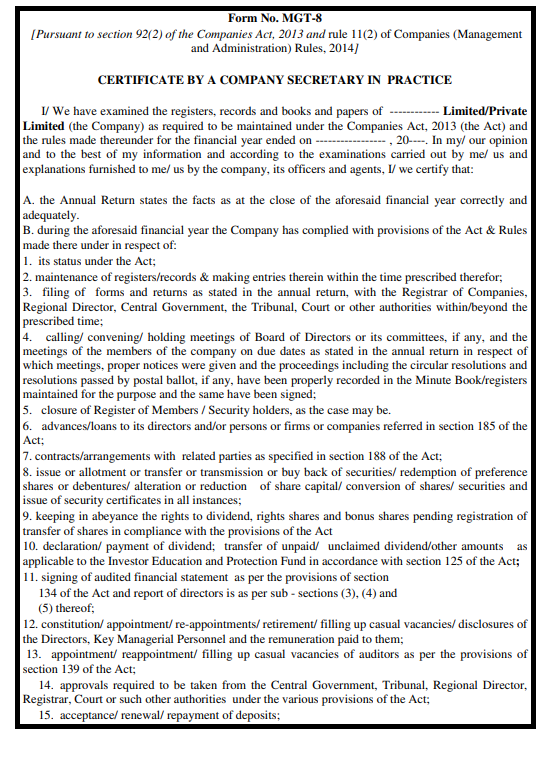

Certain companies must get their annual return certified by a practising Company Secretary (PCS).

This requirement applies to:

Listed companies.

Companies with paid-up share capital of ₹10 crore or more.

Companies with turnover of ₹50 crore or more.

The certification must be given in Form MGT-8.

MGT-8 is attached along with the annual return to confirm that the return is accurate and compliant with the Act and rules.

To Access Form MGT - 7: https://ca2013.com/wp-content/uploads/2015/07/mgt-7.pdf

To Access Form MGT - 7A: https://ca2013.com/wp-content/uploads/2021/03/MGT-7-A-05032021.pdf

To Access Form MGT -8: https://ca2013.com/returns/mgt-8/

Please note that all the forms mentioned herein above are supposed to be filed electronically.

Since it forms are long and it would disrupt , the forms have been added at the end.

Rule 12. Extract of annual return

A copy of the annual return must be filed with the Registrar, along with the fees prescribed for this purpose.

Rule 13. Return of changes in shareholding position of promoters and top ten shareholders - Omitted

Rule 14. Inspection of registers, returns etc

(1).

The registers and indices under section 88 and the copies of annual returns under section 92 must be available for inspection during business hours.

The Board of Directors may fix the exact inspection time, but it must be reasonable.

The following persons can inspect these documents without paying any fee:

Members (shareholders).

Debenture holders.

Other security holders.

Beneficial owners (persons holding securities through a depository)

Any person who is not in the above categories may inspect the documents by paying a fee.

The fee amount must be specified in the articles of association.

It cannot exceed ₹50 per inspection.

The company must allow inspection for at least two hours on every working day.

This two-hour minimum is considered “reasonable time” under this rule.

(2).

A member, debenture holder, security holder, beneficial owner, or any other person may request a copy of:

Any register.

Any entry in the register.

The annual return.

To obtain the copy, the person must pay a fee specified in the company’s articles of association, but the fee cannot exceed ₹10 per page.

Once the fee is deposited, the company must supply the requested copy within 7 days.

(3).

Even though the registers and returns are open for inspection and copying, some specific personal information of members cannot be shown to anyone.

The following details must not be made available for inspection or copying:

Address or registered office address (if the member is a company/body corporate)

Email ID.

Unique Identification Number.

PAN (Permanent Account Number.

Rule 15. Preservation of register of members etc. and annual return

(1).

The register of members and its index must be kept permanently & they can never be destroyed.

These records must be kept in the custody of the company secretary.

If the company does not have a company secretary, or if the Board decides otherwise then:

The Board may authorise any other person to keep these records safely.

(2).

The register of debenture holders or other security holders, along with the index, must be preserved for eight years.

This eight-year period is counted from the date of redemption of the debentures or securities.

These records must be kept in the custody of the company secretary.

If the Board decides, it may authorise any other person to keep these records instead.

(3).

The company must keep copies of all annual returns prepared under section 92.

It must also preserve all certificates and documents that are required to be attached to those annual returns.

These records must be kept for eight years.

The eight-year period is counted from the date the annual return was filed with the Registrar.

(4).

The foreign register of members must be preserved permanently.

This permanent preservation continues unless the register is discontinued.

If it is discontinued, all its entries must be transferred either to:

Another foreign register, or The company’s principal register in India.

The foreign register of debenture holders or other security holders must be preserved for eight years.

This eight-year period is counted from the date the debentures or securities are redeemed.

(5).

The foreign register shall be kept in the custody of the company secretary or person authorised by the Board.

Rule 16. Copies of the registers and annual return

Any of the following persons may request copies:

A member

A debenture holder

Any other security holder

A beneficial owner

Any other person

They may request copies of:

Registers maintained under section 88.

Entries in those registers.

The annual return filed under section 92.

Fee for obtaining copies

A fee may be charged as specified in the company’s Articles of Association.

The fee cannot exceed ₹10 per page.

Time limit for supplying copies

The company must provide the requested copies within 7 days from the date the fee is deposited.

Rule 17. Calling of Extraordinary general meeting by Requistionists

(1).

Members can demand (requisition) an Extraordinary General Meeting (EGM) under section 100(4).

The requisition must be given in writing or through electronic mode.

The requisition must be submitted at least 21 clear days before the proposed date of the EGM.

Clear 21 days means 21 full days excluding:

The day the requisition is given, and The day of the meeting.

(2).

The notice for the requisitioned EGM must clearly state:

The place of the meeting.

The date.

The day.

The time (hour).

The business to be discussed or decided at the meeting.

The requisitionists must hold the EGM at the registered office of the company or in the same city or town where the registered office is located.

The meeting must be held on a working day.

It cannot be held on a national holiday.

(3).

If the resolution is to be proposed as a special resolution, the notice shall be given as required by 114(2).

(4).

The notice must be signed by all the requisitionists.

It may also be signed by one requisitionists who has been authorised in writing by all the other requisitionists to sign on their behalf.

The requisitionists may also send the notice electronically.

In such a case, a scanned copy of the requisition that has been duly signed by all requisitionists must be attached.

(5).

When an extraordinary general meeting (EGM) is called by the requisitionists (members who demanded the meeting), they do not have to attach an explanatory statement under section 102.

So , the usual requirement of giving detailed explanations for each resolution does not apply to requisitioned EGMs.

However, the requisitionists may choose to disclose the reasons for the resolutions they plan to move at the meeting.

Such disclosure is optional, not mandatory.

(6).

The requisitionists first deposit a valid requisition with the company to call an EGM.

Once the valid requisition is received, the company must send the notice of the meeting.

The notice must be sent within 3 days from the date the requisition is deposited.

The notice must be given to all members whose names appear in the Register of Members on that date.

(7).

If the Board does not convene the EGM after receiving a valid requisition, the requisitionists have the right to obtain certain information from the company.

They are entitled to receive a list containing:

Names of all members.

Their registered addresses.

The number of shares held by each member.

The company is bound to provide this list.

The list must be:

Prepared as on the 21st day from the date the company received the valid requisition, and

Must include any changes that occurred up to the date of handing over the list.

The company must give this list before the expiry of 45 days from the date it received the valid requisition.

(8).

The notice of the requisitioned EGM must be sent through one of the following:

Speed post.

Registered post.

Electronic mode.

If the company accidentally fails to send notice to a member, or

If a member does not receive the notice due to postal or technical issues then:

This does not invalidate the meeting or its proceedings.

Rule 18. Notice of the meeting

(1).

A company is allowed to send a meeting notice through electronic mode.

Electronic mode refers to any communication sent by the company using its authorised and secure computer system.

This system must be able to:

Generate confirmation that the notice was sent.

Maintain a record of the communication.

The notice must be sent to the member’s last email address that the member has provided to the company.

(2).

A company may send a notice directly in the body of an e-mail as text.

The notice may also be sent as an attachment to the e-mail.

The notice may alternatively be sent as a notification that provides:

An electronic link.

A URL (Uniform Resource Locator) which the recipient can click to access and view the notice online.

(3).

(i).

The notice e-mail must be sent to the email address of the person entitled to receive it.

This email address must be taken from:

The company’s records.

The depository’s records (for demat holders).

Opportunity to register or update email address

The company must give members an advance opportunity at least once every financial year to:

Register their email address.

Update any changes in their email address.

Only the following members may make such a request:

Members who have not yet registered their email ID.

Members who want to update their email with a new one.

Members whose email IDs are already registered and unchanged cannot make repeated requests.

(ii).

When a company sends a meeting notice by e-mail, the subject line must clearly mention:

The name of the company.

The type of meeting.

The place where the meeting will be held.

The date of the meeting.

(iii).

If the notice is sent as a non-editable attachment to an e-mail, it must be in:

PDF format, or

Any other non-editable file format.

The e-mail must also include either:

A link, or Instructions to help the recipient download the required software needed to open and read the attachment.

(iv).

When a company sends notices or notifications of notice through e-mail, it must use a system that can confirm how many recipients the email was sent to.

The system must also keep a record of each specific recipient to whom the notice was e-mailed.

If any e-mail fails to deliver, the company must retain:

A notice of the failed transmission, and

A record of the re-sending of the notice to that recipient.

All these records such as:

Confirmation of total recipients.

List of individual recipients.

Failed delivery notices.

Records of re-sending must be kept by or on behalf of the company as proof that the notice was sent.

(v).

The company’s responsibility is fulfilled once it sends (transmits) the e-mail notice using its authorised system.

After the e-mail is transmitted, the company is not liable if the notice fails to reach the member due to reasons beyond the company’s control.

A member is responsible for providing or updating their correct email address with:

The company.

The depository participant (for demat holders).

If the member fails to provide or update their email address, and the company therefore cannot deliver the notice by e-mail.

The company will not be treated as being in default for non-delivery of the notice.

(vii).

The company may send e-mail through in-house facility or its registrar and transfer agent or authorise any third party agency providing bulk e-mail facility.

(viii).

If the notice is provided through an electronic link or URL, the document must be readable when the recipient opens it.

The recipient must be able to download, save, and keep a copy of the notice.

The company must provide the full URL or complete website address where the notice is hosted.

The company must also give clear instructions explaining how the recipient can access the notice or information on that link.

(ix).

When a company issues a notice for a general meeting, it must also upload the notice online.

The notice must be placed:

On the company’s own website (if the company has one).

On the website notified by the Central Government, if such a site is prescribed.

These uploads must be done at the same time the notice is issued.

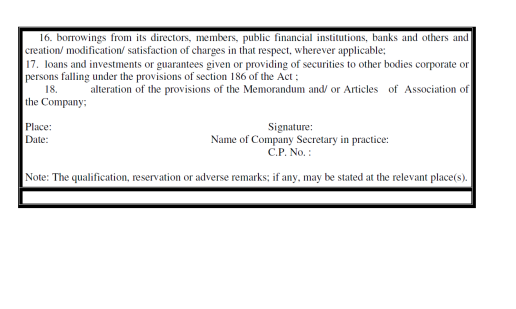

Rule 19, Proxies

(1).

A member of a section 8 company cannot appoint an outsider as a proxy.

The member is allowed to appoint a proxy only if the proxy is also a member of the same section 8 company.

(2).

One person can act as a proxy for up to 50 members.

In total, the shares held by all the members who appoint that proxy must not exceed 10% of the company’s voting share capital.

If a member holds more than 10% of the company’s voting share capital:

That member may appoint only one person as their proxy.

The person appointed by such a large shareholder:

Cannot act as proxy for anyone else.

They must represent only that one member.

(3).

The appointment of proxy shall be in the Form No. MGT.11.

To Access Form - MGT 11 - https://ca2013.com/returns/mgt-11/

Rule 20. Voting through electronic means

(1).

The following rule applies only to general meetings.

It applies only when the notice for the meeting is issued on or after the date the rule comes into force.

If a notice was issued before the rule commenced, the rule does not apply to that meeting.

(2).

The following companies are required to provide electronic voting (e-voting) to their members for resolutions at any general meeting:

Every listed company.

Every company having 1,000 or more members (even if unlisted).

So, if a company falls into either category, e-voting is compulsory.

The following do not have to provide e-voting:

Nidhis

Enterprises or institutional investors covered under Chapter XB or XC of the SEBI (ICDR) Regulations, 2009.

This means even if they are large companies or listed, these entities are exempt from the e-voting requirement.

Explanation I:

For this rule:

A Nidhi is a company:

Incorporated specifically as a Nidhi company.

Whose objective is to promote thrift and savings among its members.

Which receives deposits from and lends only to its members, for their mutual benefit.

And which follows the rules prescribed by the Central Government for Nidhi companies.

Explanation-II.

For the purpose of the rule:

(i).

Agency refers to:

National Securities Depository Limited (NSDL).

Central Depository Services (India) Limited (CDSL).

Any other entity approved by the Ministry of Corporate Affairs (MCA).

Such an entity can be treated as an agency only if it has obtained a certificate from the Standardisation Testing and Quality Certification (STQC) Directorate/

This certificate is issued under the Department of Information Technology, Ministry of Communications and Information Technology.

This certification must include compliance with the parameters specified in Explanation (vi).

(ii).

The cut-off date is a specific date fixed by the company.

This date must be not earlier than 7 days before the general meeting.

The purpose of the cut-off date is to determine who is eligible to vote, either:

By electronic voting (e-voting) before the meeting.

By voting at the general meeting itself.

Only those members whose names appear in the register (or depository records) as on the cut-off date are allowed to vote.

(iii).

Cyber security refers to protecting:

Information.

Equipment and devices.

Computers and computer resources.

Communication devices.

Any information stored in them.

The protection is specifically against:

Unauthorised access.

Unauthorised use.

Unauthorised disclosure.

Disruption,

Modification.

Destruction.

(iv).

Electronic Voting system It is a secure, system-based process used for electronic voting by members.

The system must be capable of:

Displaying electronic ballots to members.

Recording the votes cast.

Showing how many votes were cast in favour or against each resolution.

All votes cast electronically must be:

Registered, and Counted in an electronic registry stored on a centralised server.

The entire system must have adequate cyber security to prevent unauthorised access, tampering, or data loss.

(v).

Remote e-voting means allowing a member to cast their vote electronically

From any location other than the venue of the general meeting.

The member uses an electronic voting system to vote before or during the meeting, without being physically present at the meeting place.

vi).

Secured system means computer hardware, software, and procedures that:

(a) Are reasonably secure from unauthorised access and misuse.

(b) Provide a reasonable level of reliability and correct operation.

(c) Are reasonably suited to performing the intended functions.

(d). Adhere to generally accepted security procedures.

(vii).

Voting by electronic means” includes:

Remote e-voting (voting electronically from a place other than the meeting venue).

Electronic voting at the general meeting, using an electronic voting system.

The system used at the meeting may be the same system that was used for remote e-voting.

(3).

A member can use electronic voting (e-voting) to vote on the resolutions covered under sub-rule (2).

The company must ensure that these resolutions are passed following all the requirements and procedures laid down in this rule.

(4).

A company that provides electronic voting to its members shall follow this procedure:

(i)

The notice of the meeting shall be sent to all members, directors, and auditors of the company either:

(a). By registered post or speed post.

(b). Through electronic means, namely, the registered e-mail ID of the recipient; or

(c). By courier service.

(ii).

The notice shall also be uploaded on the company’s website, if it has one, and on the website of the agency, immediately after the notice is sent to the members.

(iii).

The notice of the meeting shall clearly state:

(a). That the company is providing the facility for voting by electronic means and that the business may be transacted through such voting.

(b). That the facility for voting, either through an electronic voting system or by ballot or polling paper, will also be available at the meeting.

Members attending the meeting who have not already cast their vote by remote e-voting will be able to vote at the meeting.

(c). That members who have cast their vote by remote e-voting prior to the meeting may also attend the meeting, but they will not be allowed to vote again.

(iv).

The notice shall:

(a). Indicate the process and manner for voting by electronic means.

(b). Indicate the time schedule, including the time period during which votes may be cast by remote e-voting.

(c). Provide the details about the login ID.

(d). Specify the process and manner for generating or receiving the password and for casting the vote in a secure manner.

(v).

The company shall publish a public notice by advertisement immediately after completing the despatch of meeting notices under clause 4(i).

The public notice should be published at least 21 days before the general meeting.

This advertisement must be published:

Once in a vernacular newspaper in the principal vernacular language of the district where the registered office is located.

The newspaper should be widely circulated in that area.

Once in an English newspaper having nationwide circulation.

The advertisement shall specify, among other things, the following:

(a). A statement that the business may be transacted through voting by electronic means.

(b). The date and time of commencement of remote e-voting.

(c). The date and time of end of remote e-voting.

(d). The cut-off date.

(e). The manner in which persons who acquire shares and become members after despatch of the notice may obtain the login ID and password.

(f). The statement that:

(A). Remote e-voting shall not be allowed beyond the said date and time.

(B). The manner in which the company shall provide for voting by members present at the meeting.

(C). A member may participate in the general meeting even after exercising his right to vote through remote e-voting, but shall not be allowed to vote again in the meeting.

(D). A person whose name is recorded in the register of members or in the register of beneficial owners maintained by the depositories as on the cut-off date only shall be entitled to avail the facility of remote e-voting as well as voting in the general meeting.

(g). The website address of the company, if any, and of the agency where the notice of the meeting is displayed.

(h). The name, designation, address, email ID Ph. No. of the person responsible for addressing grievances related to the electronic voting facility.

Provided that:

The public notice shall also be placed on the website of the company, if any, and on the website of the agency.

(vi).

The facility for remote e-voting shall remain open for not less than three days and shall close at 5.00 p.m. on the date preceding the date of the general meeting.

(vii).

During the period when remote e-voting is available, any member holding shares in physical or dematerialised form on the cut-off date may use the remote e-voting facility.

Once a member casts his vote through remote e-voting, he cannot change it or vote again.

A member may still attend and participate in the general meeting even after voting through remote e-voting, but he will not be allowed to vote again at the meeting.

(viii).

At the end of the remote e-voting period, the e-voting facility must be immediately blocked.

If the company uses the same electronic voting system during the general meeting, that system shall remain active until all resolutions are considered and voted on at the meeting.

This facility at the meeting can be used only by members who are present at the meeting and who have not already voted through remote e-voting.

(ix).

The Board of Directors must appoint one or more scrutinisers.

A scrutiniser may be:

A Chartered Accountant in practice.

A Cost Accountant in practice.

A Company Secretary in practice.

An Advocate, or any other reputable person who is not employed by the company and who, in the Board’s opinion, can scrutinise the voting and remote e-voting process fairly and transparently.

The scrutiniser appointed may take the assistance of a person who is not employed by the company and who is well-versed with the electronic voting system.

(x).

The scrutiniser must express willingness to be appointed.

The scrutiniser must also be available to carry out the work of ascertaining the requisite majority during the voting process.

(xi)

At the general meeting, after the discussion on the resolutions is completed, the Chairman must allow voting.

The voting shall be allowed in the manner specified in clauses (a) to (h) of sub-rule (1) of rule 21, as applicable.

The Chairman shall conduct this voting with the assistance of the scrutiniser.

Voting may be done by ballot, polling paper, or an electronic voting system.

This voting is only for members who are present at the meeting and have not already cast their vote through remote e-voting.

(xii).

After voting at the general meeting ends, the scrutiniser must first count the votes cast at the meeting.

After that, the scrutiniser must unblock the remote e-votes, and this must be done in the presence of at least two witnesses who are not employees of the company.

The scrutiniser must prepare a consolidated report of all votes (both at the meeting and remote e-voting) and submit it to the Chairman or a person authorised by the Chairman in writing.

This must be done within three days of the conclusion of the meeting.

The Chairman or the authorised person must declare the results immediately.

(xiii).

To ensure that members who have already voted through remote e-voting do not vote again at the general meeting, the scrutiniser must be given certain details.

The scrutiniser shall be allowed access to these details after the remote e-voting period closes and before the general meeting begins.

The details may include:

Names of members.

Folio numbers.

Number of shares held.

Any other information the scrutiniser requires

The scrutiniser will receive only the information needed to identify who has already voted.

The scrutiniser will not be given any information about how those members voted.

(xiv).

The scrutiniser must maintain a register, either in manual form or electronic form.

This register must record all assent or dissent (votes in favour or against a resolution) received.

The register must include the following details of each member:

Name.

Address.

Folio number or client ID.

Number of shares held.

Nominal value of the shares

Whether the shares carry differential voting rights.

(xv).

The scrutiniser must keep the register and all other documents related to electronic voting in safe custody.

These documents must remain with the scrutiniser until the Chairman reviews, approves, and signs the minutes of the meeting.

After the minutes are signed, the scrutiniser must hand over the register and all related papers to the company.

(xvi).

Once the Chairman declares the results, the results along with the scrutiniser’s report must be placed immediately on the website of the company (if the company has a website).

The results must also be placed on the website of the agency providing the e-voting platform.

If the company’s equity shares are listed on a recognised stock exchange, the company must at the same time send the results to the concerned stock exchange(s).

The stock exchange(s) must then place the results on their website.

(xvii).

A resolution is considered passed on the date of the general meeting, provided the requisite number of votes has been received.

The term “requisite number of votes” means the number of votes needed to pass:

An ordinary resolution, or a special resolution, as required under section 114 of the Companies Act.

(xviii).

A resolution that is proposed to be considered through electronic voting cannot be withdrawn.

Access Form MGT - 7: https://ca2013.com/wp-content/uploads/2015/07/mgt-7.pdf

To Access Form MGT - 7A: https://ca2013.com/wp-content/uploads/2021/03/MGT-7-A-05032021.pdf

To Access Form MGT -8: https://ca2013.com/returns/mgt-8/