Management & Administration Rules (Rule 21-30)

Rule 21. Manner in which the Chairman of meeting shall get the poll process scrutinised and report thereon

(1).

The Chairman of a meeting shall ensure that:

(a). The Scrutinizers shall be provided with the Register of Members, specimen signatures of the members, the Attendance Register, and the Register of Proxies.

(b). The Scrutinizers shall be provided with all documents received by the Company under sections 105, 112, and 113.

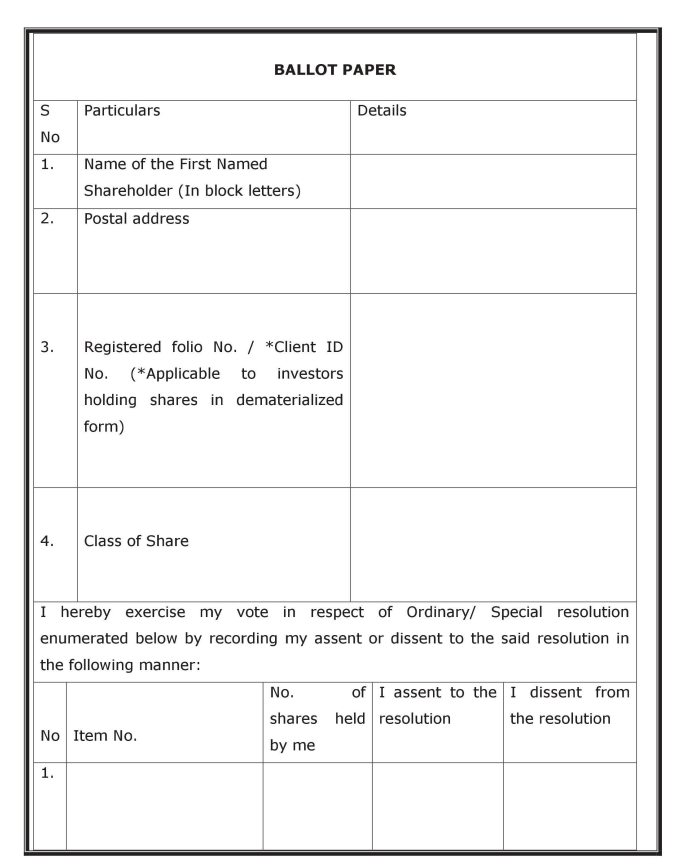

(c). The Scrutinizers shall arrange polling papers and distribute them to members and proxies present at the meeting.

In the case of joint shareholders, the polling paper shall be given to the first-named holder.

If he is absent, to the next joint holder attending the meeting, following the chronological order in the folio.

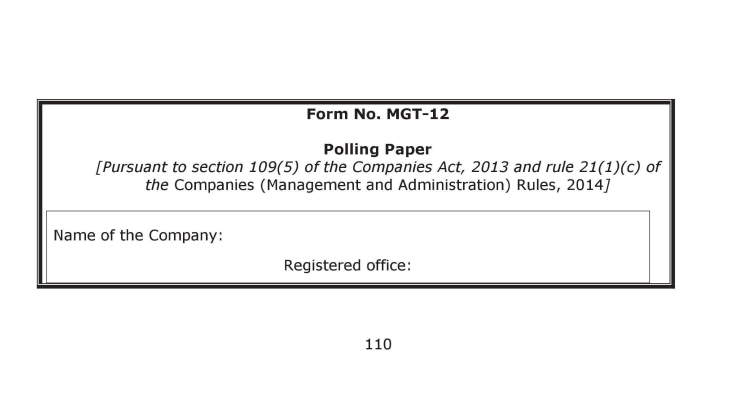

The polling paper shall be in Form MGT-12.

(d). The Scrutinizers shall keep a record of all polling papers received for the poll by initialing each one.

(e). The Scrutinizers shall lock and seal an empty polling box in the presence of the members and proxies.

(f). After the voting process is completed, the Scrutinizers shall open the polling box in the presence of two witnesses.

(g). If there is any ambiguity regarding the validity of a proxy, the Scrutinizers shall decide the matter in consultation with the Chairman.

(h). The Scrutinizers shall ensure that if a member who appointed a proxy votes in person, the vote cast by the proxy shall be disregarded.

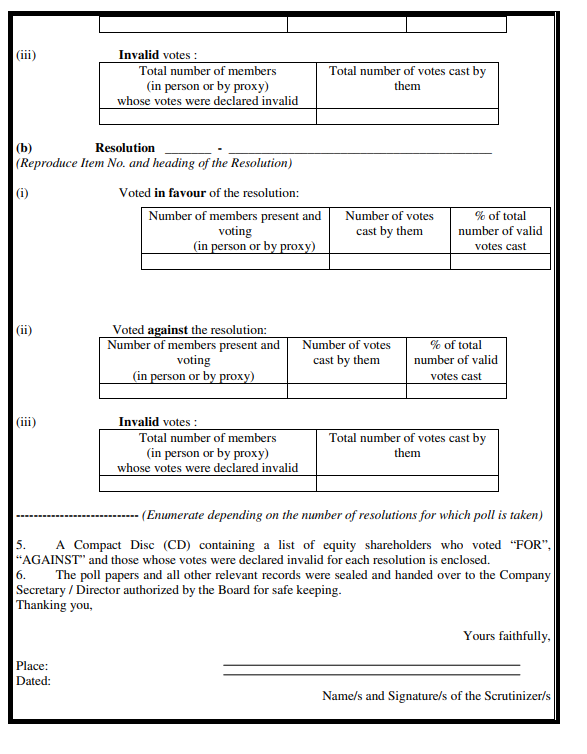

(i). The Scrutinizers shall count all votes cast on the poll and prepare a report addressed to the Chairman.

(j). When voting is conducted by electronic means under section 108 and the related rules:

The company shall provide all necessary support, technical and otherwise, to the Scrutinizers for orderly voting and accurate counting of results.

(k). The Scrutinizers’ report shall state the total votes cast, valid votes, votes in favour and against the resolution.

The report should also state all the details of invalid polling papers and the votes contained in them.

(l). The Scrutinizers shall submit their report to the Chairman, who shall countersign it.

(m). The Chairman shall declare the result of the poll. The result may be announced either by him or by a person authorised by him in writing.

(2).

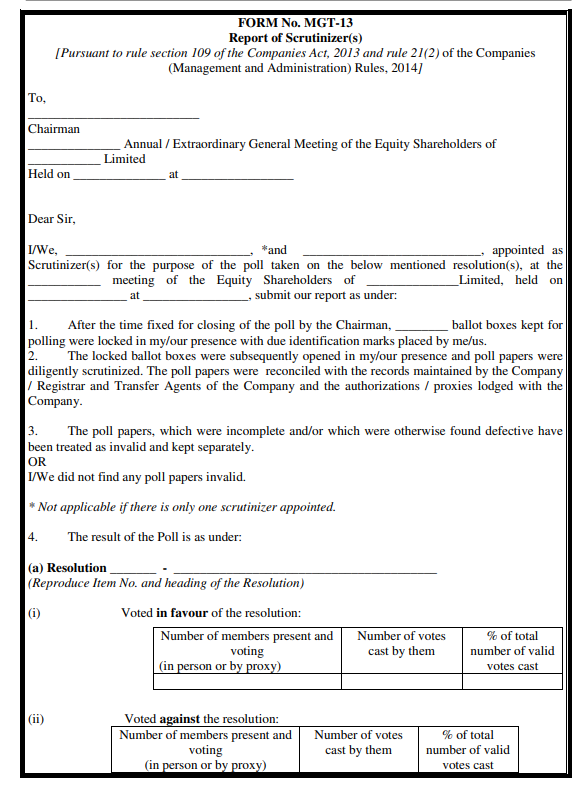

The Scrutinizers appointed for the poll shall submit a report to the Chairman of the meeting in Form MGT.13.

The report shall be signed by the Scrutinizer, and if more than one Scrutinizer is appointed, it shall be signed by all of them.

The report must be submitted to the Chairman within seven days from the date the poll is taken.

To Access Form MGT -12: https://ca2013.com/wp-content/uploads/2015/08/MGT-12.pdf

Please note that this form should be filed electronically.

To Access Form MGT - 13: https://ca2013.com/wp-content/uploads/2015/07/mgt-13.pdf

Please note that this form should be filed electronically.

Rule 22. Procedure to be followed for conducting business through postal ballot

(1).

When a company is required or chooses to pass a resolution by postal ballot, it must send a notice to all shareholders.

The notice must include the draft resolution and an explanatory statement giving the reasons for the resolution.

The notice must request shareholders to send their assent or dissent in writing on a postal ballot.

Postal ballot means voting by post or through electronic means.

Shareholders must send their vote within 30 days from the date the notice is dispatched.

(2).

The notice shall be sent either:

(a). By Registered Post or speed post.

(b). Through electronic means like registered e-mail id.

(c). Through courier service for facilitating the communication of the assent or dissent of the shareholder w.r.t resolution within the said period of 30 days.

(3).

The company must publish an advertisement about the dispatch of ballot papers.

The advertisement must be published:

At least once in a vernacular newspaper in the principal vernacular language of the district where the registered office is located.

This newspaper must be widely circulated in that district.

At least once in an English newspaper with wide circulation in that same district.

The advertisement must also specify certain matters, including other required details.

The other details are:

(a). A statement that the business is to be transacted by postal ballot, which includes voting by electronic means.

(b). The date on which the dispatch of notices was completed.

(c). The date on which voting begins.

(d). The date on which voting ends.

(e). A statement that any postal ballot received after the end date will not be valid.

Voting, whether by post or electronic means, will not be allowed after that date.

(f). A statement that members who have not received the postal ballot form may apply to the company and obtain a duplicate.

(g). The contact details of the person responsible for addressing grievances related to voting by postal ballot, including electronic voting.

(4).

The notice of the postal ballot must be placed on the company’s website immediately after it is sent to the members.

The notice must remain available on the website until the last date for receiving postal ballots from the members.

(5).

The Board of Directors must appoint one scrutinizer for the postal ballot process.

The scrutinizer must not be an employee of the company.

The Board must be satisfied that the scrutinizer can conduct the postal ballot voting process in a fair and transparent manner.

(6).

The scrutinizer shall be willing to be appointed and be available for the purpose of ascertaining the requisite majority.

(7).

If the requisite majority of shareholders approve a resolution through a postal ballot (including electronic voting),

The resolution is considered validly passed.

It is treated as if it has been passed at a general meeting convened specifically for that purpose.

(8).

Postal ballots returned by shareholders must be kept in the safe custody of the scrutinizer.

After a shareholder has submitted their assent or dissent in writing, no person is allowed to:

Deface the ballot paper.

Destroy the ballot paper.

Disclose the identity of the shareholder who cast that vote.

(9).

The scrutinizer shall submit his report as soon as possible after the last date of receipt of postal ballots but not later than seven days thereof.

(10).

The scrutinizer must maintain a register, either manually or electronically, to record all assents and dissents received through postal ballot.

The register must include the following details of each shareholder:

Name.

Address.

Folio number or client ID.

Number of shares held.

Nominal value of the shares.

Whether the shares carry differential voting rights, if applicable

The register must also record:

Details of postal ballots received in a defaced or mutilated condition.

Details of invalid postal ballot forms

(11).

The scrutinizer must keep the postal ballots and all other related papers, including those for electronic voting, in safe custody.

These documents must remain with the scrutinizer until the Chairman reviews, approves, and signs the minutes of the meeting.

After the minutes are signed, the scrutinizer must return the ballot papers, related documents, and the register to the company.

The company must then preserve these papers and registers safely.

(12).

Any assent or dissent (vote) received after 30 days from the date the notice was issued will not be counted.

Such a late reply will be treated as if the member did not respond at all.

(13).

The results shall be declared by placing it, along with the scrutinizer’s report, on the website of the company.

(14).

A postal ballot resolution is treated as passed on the same date as a meeting held for passing that resolution.

(15).

The provisions of rule 20 regarding voting by electronic means shall apply, as far as applicable, mutatis mutandis to this rule in respect of the voting by electronic means.

(16).

Under clause (a) of sub-section (1) of section 110, the following items of business must be transacted only through postal ballot:

(a) Changing the main objects of the company in the memorandum.

(b) Changing the articles to add or remove provisions that make the company a private company. (In accordance with Section 2(68)).

(c) Shifting the registered office to a different city, town, or village.(In accordance with Section 12(5)).

(d) Changing the purpose for which public money (raised through a prospectus) was to be used, when some of that money is still unused. (13(8).)

(e) Issuing shares that have different voting or dividend rights. (In accordance with 43(a)(ii).)

(f) Changing the rights attached to any class of shares, debentures, or other securities. (In accordance with Section 48)

(g) Buying back the company’s own shares. (In accordance with section 68(1))

(h) Electing a director by small shareholders. (In accordance with Section 151)

(i) Selling the whole or a major part of the company’s undertaking. (In accordance with section 180(1)(a).)

(j) Giving loans, guarantees, or security beyond the permitted limit. (In accordance with 186(3).)

Some items of business are normally required to be passed only through a postal ballot.

However, if a company is required to provide e-voting under section 108:

Those items may instead be taken up at a general meeting.

The company must provide e-voting facility for that meeting.

The e-voting must fully comply with the procedure laid down in section 108.

One Person Companies (OPCs) and Other companies with up to 200 members are not required to transact any business through postal ballot.

Rule 23. Special Notice

(1).

A special notice must be signed by member(s) who meet either of the following requirements:

They hold not less than 1% of the total voting power.

They hold shares on which an aggregate paid-up amount of at least ₹5 lakh has been paid on the date of the notice.

The members may sign the notice individually or collectively.

(2).

The special notice must be sent by the members to the company not earlier than 3 months before the meeting date.

It must also be sent at least 14 days before the meeting.

While calculating the 14 days, exclude:

The day the notice is given, and the day of the meeting.

(3).

Once the company receives a valid special notice, it must immediately notify all its members about the proposed resolution.

This notice to members must be given at least 7 days before the meeting.

While calculating the 7 days, exclude:

The day the notice is dispatched, and the day of the meeting.

The notice must be given in the same manner as notices of any general meeting.

(4).

If it is not practicable for the company to give the special notice in the same manner as a general meeting notice, then the company must publish the notice in newspapers.

The notice must be published:

In an English newspaper in English language & in a vernacular newspaper in the regional language.

Both having wide circulation in the State where the company’s registered office is located.

The notice must also be posted on the company’s website, if the company has one.

(5).

The notice shall be published at least seven days before the meeting, exclusive of the day of publication of the notice and day of the meeting.

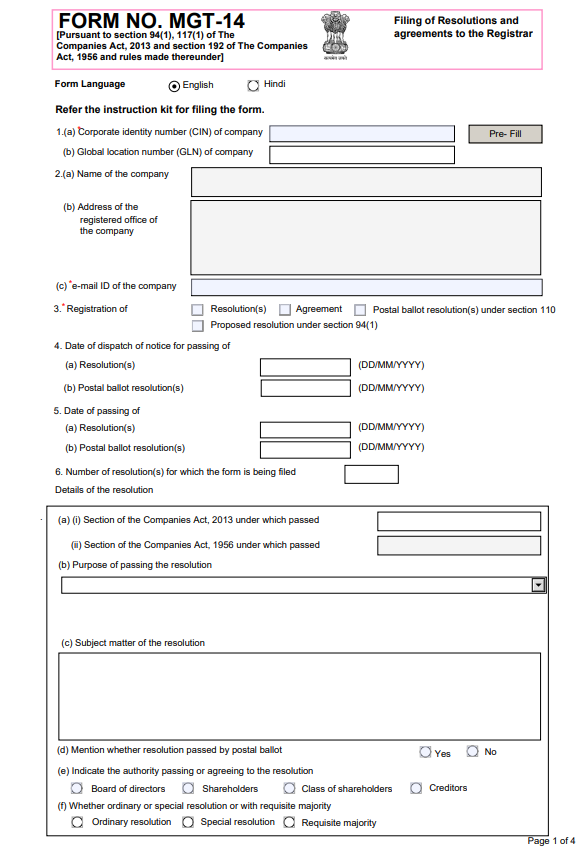

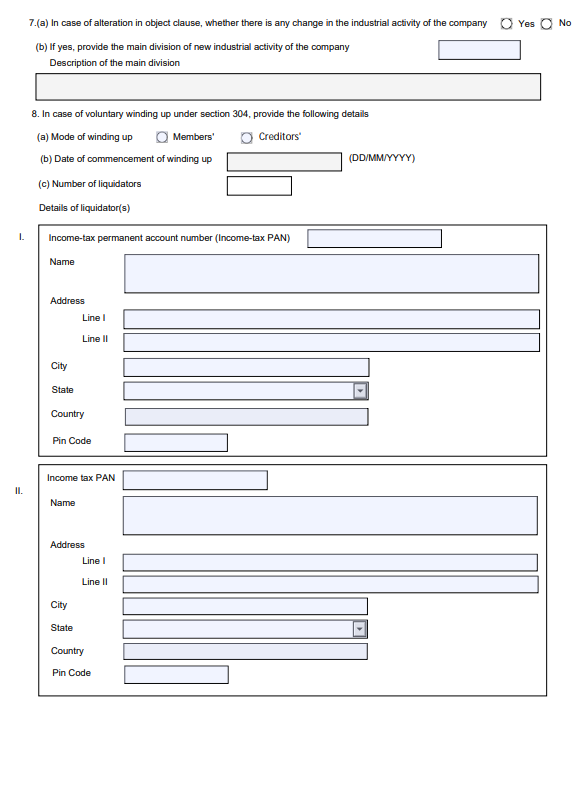

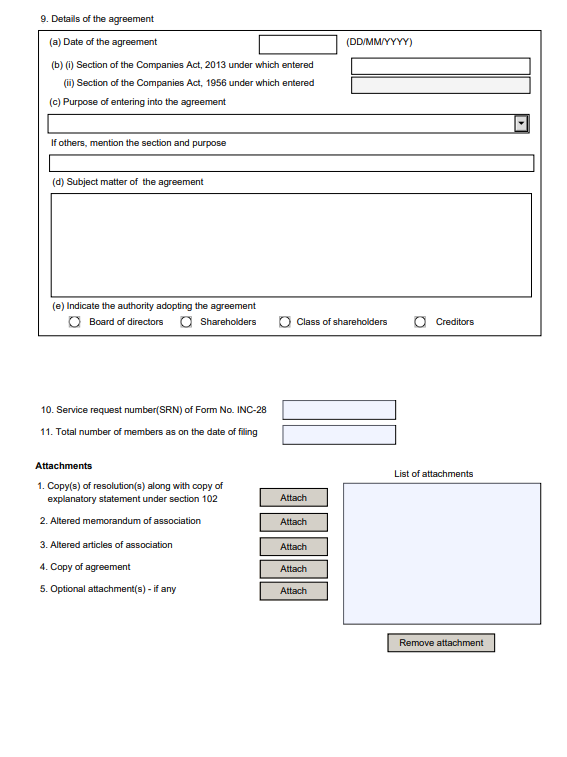

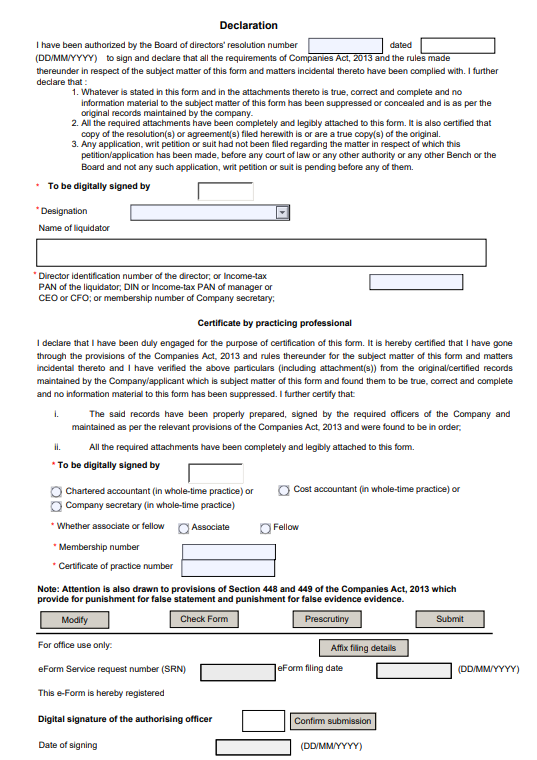

Rule 24. Resolutions and agreements to be filed

Certain resolutions or agreements are required to be filed with the Registrar.

A copy of such resolution or agreement must be filed along with any explanatory statement under section 102, if applicable.

The filing must be done in Form MGT-14.

The form must be submitted along with the prescribed fee.

To Access Form MGT-14: https://ca2013.com/wp-content/uploads/2015/08/Form_MGT-14.pdf

Please note that this form should be filed electronically.

Rule 25. Minutes of proceedings of general meeting, meeting of Board of Directors and other meetings and resolutions passed by postal ballot

(1).

(a). A distinct minute book shall be maintained for each type of meeting namely:

(i). General meetings of the members.

(ii). Meetings of the creditors.

(iii). Meetings of the Board.

(iv). Meetings of each of the committees of the Board.

Explanation:

Any resolution that is passed through a postal ballot must be entered in the minute book of general meetings.

When it is recorded, it should be treated as though the resolution was passed in an actual general meeting, even though the members voted remotely.

In effect, postal ballot resolutions get the same legal status and recording method as resolutions passed in a physical or virtual general meeting.

(b)

(i).

The minutes of every meeting must be written/entered in the designated minute book.

This entry has to be made within 30 days from the date the meeting concluded.

The minute book must be specifically maintained for recording the proceedings of such meetings.

(ii).

For every resolution passed through a postal ballot, a brief report of the postal ballot process must be recorded in the minute book of general meetings.

This report should include:

The resolution proposed,

The voting result, and

A summary of the scrutinizer’s report.

The entry must also state the date on which it was made.

This entire entry must be completed within 30 days from the date the resolution is deemed passed.

(c). Omitted

(d).

Every page of the minute book must be initialled or signed.

For each meeting’s proceedings or each postal-ballot report recorded in the book, the last page of that specific entry must be dated and signed.

(i). For minutes of a Board meeting or a committee meeting:

The minutes must be signed either by the chairman of the same meeting in which the proceedings occurred or

By the chairman of the next meeting that takes place after it.

(ii). For minutes of a general meeting:

They must be signed by the chairman of that same meeting, and this must be done within the 30-day period.

If the chairman dies or is unable to sign within that period, then a director authorised by the Board may sign the minutes instead.

(iii). For every resolution passed by postal ballot:

The entry in the minutes must be signed by the chairman of the Board within the 30-day period.

If there is no chairman, or if the chairman dies or is unable to sign within that period, then a director authorised by the Board may sign it.

(e).

The minute books of general meetings must be kept at the registered office of the company.

These minute books must be preserved permanently.

They must remain in the custody of the company secretary, or if there is none / or as authorised, a director authorised by the Board to keep them.

(f).

The minute books of Board meetings and committee meetings must be preserved permanently.

They must be kept in the custody of the company secretary, or a director authorised by the Board for this purpose.

These minute books must be kept either at the registered office of the company or at any other place that the Board decides.

Rule 26. Copy of minute book of general meeting

Any member of the company has the right to obtain a copy of the minutes of any general meeting.

The company must provide this copy within seven working days after the member makes a request.

The member must pay the amount specified in the company’s AOA, but the company cannot charge more than ₹10 per page (or part of a page).

Any member who requests a soft copy of the minutes of general meetings held during the last three financial years is entitled to receive it.

The company must provide this soft copy free of cost.

Rule 27. Maintenance and inspection of document in electronic form

(1).

Every listed company, and every company that has 1,000 or more shareholders, debenture holders, or other security holders,

may maintain its records in electronic form, if required under the Act or the rules made under it.

Explanation:

For existing companies, records that are currently in physical form may be converted into electronic form.

This conversion must be completed within six months from the date on which the provisions of section 120 of the Act are notified.

(2).

The records maintained in electronic form shall be kept in a manner the Board of Directors considers appropriate.

Provided that:

(a). The records must follow the same formats and comply with all requirements prescribed in the Act and the rules.

(b). All information required under the Act or rules must be properly recorded for future reference.

(c). The records must be readable, retrievable, and capable of being reproduced in printed form.

(d). The records must be capable of being digitally dated and signed wherever required under the Act or rules.

(e). Once a record is digitally dated and signed, it must not be capable of being edited or altered.

(f). The records must be capable of being updated as per the Act or rules, and each update must record the date of updating.

For the purpose of this rule, the term records refers to:

Any register.

Any index.

Any agreement.

Any memorandum.

Any minutes.

Any other document , that a company is required to keep under the Act or the rules made under it.

Rule 28. Security of records maintained in electronic form

(1).

The Managing Director, Company Secretary, or any other director or officer designated by the Boar shall be:

Responsible for maintaining and ensuring the security of the company’s electronic records.

(2).

The person who is responsible for the maintenance and security of electronic records shall:

(a). Provide adequate protection against unauthorized access, alteration or tampering of records.

(b). Ensure against loss of the records as a result of damage to, or failure of, the media on which the records are maintained.

(c). Ensure that the signatory of electronic records does not repudiate the signed record as not genuine.

(d). Ensure that computer systems, software and hardware are adequately secured and validated to ensure their accuracy, reliability and consistent intended performance.

(e). Ensure that the computer systems can discern invalid and altered records.

(f). Ensure that records are accurate, accessible, and capable of being reproduced for reference later.

(g). Ensure that the records are at all times capable of being retrieved to a readable and printable form.

(h). Ensure that records are kept in a non-rewritable and non-erasable format like PDF version or some other version which cannot be altered or tampered.

(i). At least one backup of the updated electronic records must be taken at intervals not exceeding one day.

Every backup must be authenticated and dated.

All backups must be securely stored at locations decided by the Board.

(j). Access to the records must be restricted.

Only the following may access them:

The Managing Director.

The Company Secretary.

Any other director or officer.

Any person performing work for the company who is authorised by the Board.

(k). Ensure that any reproduction of non-electronic original records in electronic form is complete, authentic, true and legible when retrieved.

(l). Arrange and index the records in a way that permits easy location, access and retrieval of any particular record.

(m). Take necessary steps to ensure security, integrity and confidentiality of records.

Rule 29. Inspection and copies of records maintained in electronic form

If a company keeps its records in electronic form, then any legal duty to allow inspection or provide copies applies to the electronic records as well.

The company must make such records available for inspection in electronic form.

When copies are requested, the company must provide clear, readable reproductions of the whole or part of the electronic records.

The company may charge a fee, but not more than ten rupees per page.

Rule 30. Penalty

If the company fails to comply with any provision of this rule, it will be liable for punishment.

Every officer or any other person responsible for the default will also be liable.

The fine may go up to five thousand rupees.

If the violation continues, an additional fine of up to five hundred rupees per day (after the first day) may be imposed.

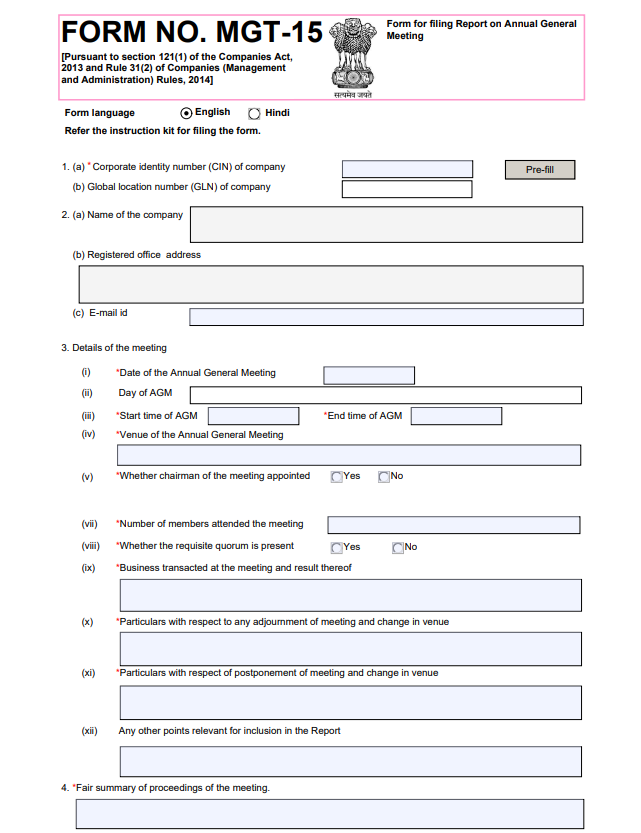

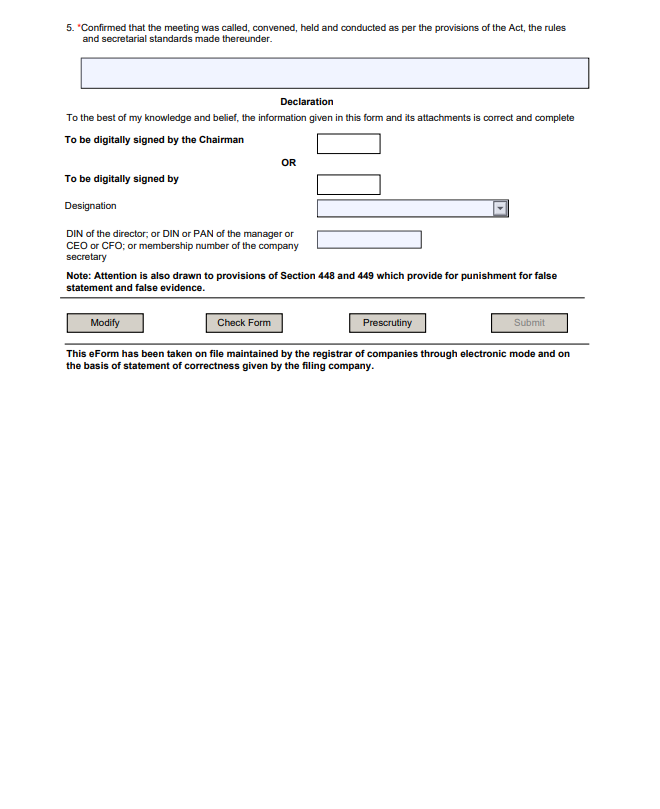

Rule 31. Report on Annual General Meeting

(1).

The report required under section 121(1) must be prepared.

It must be prepared in the manner specified in this rule.

The following clauses describe how the report should be prepared.

(a).

The report under this section shall be prepared in addition to the minutes of the general meeting;

(b).

The report must be signed and dated.

Normally, it should be signed by the Chairman of the meeting.

If the Chairman is unable to sign, then it must be signed by:

Any two directors.

Any of them must be the Managing Director, if the company has one.

The Company Secretary must also sign the report.

(c).

The report shall contain details of the following:

(i). The day, date, hour and venue of the annual general meeting.

(ii). Confirmation regarding the appointment of the Chairman of the meeting.

(iii). The number of members who attended the meeting.

(iv). Confirmation that quorum was present.

(v). Confirmation of compliance with the Act, the Rules, and the applicable secretarial standards relating to calling, convening and conducting the meeting.

(vi). The business transacted at the meeting and the results of such business.

(vii). Details of any adjournment, postponement of the meeting, or change in venue.

(viii). Any other relevant points that should be included in the report.

(d).

The Report shall contain fair and correct summary of the proceedings of the meeting.

(2).

A copy of the report prepared under section 121(1) and sub-rule (1) must be filed with the Registrar.

It must be filed in Form MGT-15.

The filing must be done within thirty days from the conclusion of the annual general meeting.

The prescribed fee must be paid along with the form.

To Access Form MGT - 15: https://ca2013.com/wp-content/uploads/2015/08/Form_MGT-15.pdf

Please note that this form should be filed electronically.