Share Capital & Debenture Rules (Rule 10-15)

Rule 10. Issue and redemption of preference shares by company in infrastructural projects.

Companies involved in setting up and dealing with infrastructural projects are allowed to issue preference shares for a longer period than usual.

They may issue preference shares for a tenure greater than 20 years, but not more than 30 years.

However, from the 21st year onward, the company must start redeeming these preference shares.

he company must redeem at least 10% of the total preference shares every year.

Redemption must be done on a proportionate basis, so all preference shareholders are treated equally.

Redemption may also happen earlier, if the preference shareholders choose to exercise their option.

Rule 11. Instrument of transfer.

(1).

When securities are held in physical form, they must be transferred using Form SH-4.

The transfer instrument (Form SH-4) must clearly show the date on which it was executed / signed.

After execution, the duly filled and signed transfer form must be delivered to the company within 60 days from that execution date.

(2).

• Some companies do not have share capital.

• For such companies, the rule in 11(1) still applies.

• However, since these companies do not issue securities, the rule must be read differently.

• Any reference to securities in 11(1) should be understood as referring to the member’s interest in the company.

(3).

When a partly paid share is being transferred then:

The company cannot register the transfer immediately.

First, the company must send a notice in Form SH-5 to the transferee (the person receiving the shares).

The transferee must be given an opportunity to respond.

The transferee must give no objection to the transfer.

The transferee has two weeks from the date they receive the notice to give this no-objection.

If the transferee does not object within two weeks, the company may proceed with registering the transfer.

If the transferee raises an objection, the company cannot register the transfer.

To Access Form SH - 4: https://ca2013.com/returns/sh-4/

To Access Form SH - 5: https://ca2013.com/returns/sh-5/

Rule 12. Issue of employee stock options.

Unlisted companies are not required to follow SEBI’s Employee Stock Option Scheme (ESOS) Guidelines which apply only to listed companies.

Even though they are exempt from SEBI ESOS rules, such unlisted companies cannot grant Employee Stock Options (ESOPs).

Although , ESOPs can be granted if they follow certain mandatory requirements under the Companies Act and these rules.

(1).

The issue of Employees Stock Option Scheme should have been approved by the shareholders of the company by passing a special resolution.

Explanation:

(a).

An employee includes any permanent employee of the company, working in India, or outside India.

(b)

An employee also includes any director of the company, whether whole-time, or part-time, but excludes independent directors.

(c)

An employee also includes:

Any person covered under (a) or (b) who works for a subsidiary, whether in India or abroad.

Any person covered under (a) or (b) employed by the holding company.

Any person covered under (a) or (b) employed by an associate company.

Persons not included as an employee for the purposes of ESOPs

(i).

An employee who is a promoter, or who belongs to the promoter group is considered an employee.

(ii).

A director who, either Himself, or through a relative, or through a body corporate, directly or indirectly holds more than 10% of the outstanding equity shares of the company is not considered an employee.

For a startup company as defined in Notification G.S.R. 127(E), dated 19 Feb 2019 – DPIIT

The disqualifications in (i) (promoter or promoter group) and (ii) (director holding >10% shares) do not apply.

This relaxation applies for 5 years (updated from 10 years) from the date of incorporation or registration of the startup.

(2).

When a company proposes to pass a resolution for issuing ESOPs, the explanatory statement must disclose the following:

(a). The total number of stock options that the company plans to grant.

(b). The classes of employees who will be eligible to participate in the ESOP scheme.

(c). Details of the appraisal process used to determine which employees qualify for ESOPs.

(d). The vesting requirements and the vesting period for the options.

(e). The maximum period within which all options must vest.

(f). The exercise price, or the formula used to determine the exercise price.

(g). The exercise period and the procedure employees must follow to exercise their options.

(h). The lock-in period, if any, applicable to the shares issued after exercise.

(i). The maximum number of options that may be granted: per employee, and in total (aggregate limit).

(j). The valuation method the company will use for pricing or accounting for its stock options.

(k). The conditions under which vested options may lapse, such as termination due to misconduct.

(l). The time period within which an employee must exercise vested options if:

The employee is proposed to be terminated, or the employee resigns.

(m). A statement confirming that the company will comply with applicable accounting standards for ESOPs.

(3).

A company offering ESOPs has the freedom to decide the exercise price of the stock options.

There is no mandatory formula prescribed by the rules for determining the exercise price.

However, the exercise price must be set in accordance with the applicable accounting policies or standards (if any apply).

The exercise price of ESOPs (Employee Stock Option Plans) is the price at which an employee can buy the company’s shares when they exercise their options.

(4).

(a). Granting ESOP options to employees of the subsidiary or holding company

A company is allowed to give ESOPs not only to its own employees but also to:

Employees of its subsidiary company, and Employees of its holding company.

(b). Granting a large number of ESOPs to a single employee (1% rule)

A company must take special shareholder approval if it plans to grant a large ESOP allocation to any one employee in a year.

It is required when the ESOP grant to a single employee in one financial year is:

Equal to or more than 1% of the company’s issued share capital,

While calculating issued share capital, you must exclude:

Outstanding warrants,

And outstanding convertible instruments (like CCDs, FCCBs, etc.),

The 1% must be calculated based on the issued share capital on the exact date of the ESOP grant.

(5).

(a).

A company may change or modify the terms of its Employees Stock Option Scheme (ESOP), but only by passing a special resolution.

Such variation is allowed only for options that have not yet been exercised.

The variation must not harm or disadvantage the employees who hold those options.

(b)

When proposing the special resolution to vary ESOP terms, the notice must clearly disclose:

The full details of the proposed variation.

The reason or justification for the variation.

The details of the employees who will benefit from the variation.

(6).

(a).

There must be a minimum gap of 1 year between the grant of ESOP options, and the vesting of those options.

If options are granted by a company in exchange for options from another company (due to merger or amalgamation), then:

The period for which the employee already held the options in the merging/amalgamating company will count toward the 1-year minimum vesting period.

So , the employee does not need to restart the 1-year vesting clock.

(b).

The company is free to set a lock-in period (if any) for the shares issued after an employee exercises the ESOP options.

This period is not prescribed by law and the company decides it.

(c).

Until the employee actually receives shares which is until the option is exercised and shares are allotted:

The employee cannot receive dividends.

The employee cannot vote.

The employee cannot enjoy any shareholder rights.

(7).

Amount paid at the time of grant may be forfeited if the employee does not exercise the option

Sometimes, companies ask employees to pay a small amount when ESOP options are granted.

If the employee later does not exercise the option within the allowed exercise period, the company is allowed to keep (forfeit) that amount.

So, If you don’t use your option in time, you lose the money you paid at grant.

Amount may be refunded if the options do not vest

ESOPs vest only if certain conditions are met (such as completing a minimum service period or achieving performance targets).

If the employee fails to meet the vesting conditions, the options will not vest.

In such cases, the company may return the amount paid at the time of grant.

(8).

(a).

ESOP options granted to an employee cannot be transferred to any other person.

(b).

ESOP options also cannot be pledged, mortgaged, hypothecated, or otherwise encumbered in any manner.

So, the employee cannot use the options as security or collateral.

(c).

Only the employee to whom the option was originally granted is allowed to exercise the option.

No one else may exercise it except as permitted under clause (d).

(d).

If an employee dies while in employment then:

All options granted up to the date of death shall vest immediately, and the deceased employee’s legal heirs or nominees may exercise those options.

(e)

If an employee suffers permanent incapacity while still employed, then all options granted up to that date shall vest immediately on the day of incapacity.

(f)

If an employee resigns or is terminated, then:

All unvested options lapse/expire immediately.

Vested options may still be exercised, but only within the period specified in the ESOP scheme.

Exercising vested options must follow the terms approved by the Board.

(9).

The Board of Directors must disclose the following details about the ESOP scheme in the Directors’ Report for that financial year:

(a). The number of options granted during the year.

(b). The number of options that vested during the year.

(c). The number of options exercised by employees.

(d). The total number of shares issued as a result of employees exercising options.

(e). The number of options that lapsed.

(f). The exercise price of the options.

(g). Any variation to the terms of the ESOP during the year.

(h). The amount of money received by the company from employees upon exercise of options.

(i). The total number of options currently in force.

(j). Employee-wise details of options granted, including:

(i). Key managerial personnel (KMP) who received ESOP grants.

(ii). Any employee who received ESOP grants in a single year amounting to 5% or more of the total options granted that year.

(iii). Any identified employee who received ESOP grants in a single year equal to or more than 1% of the company’s issued share capital.

This excludes outstanding warrants/conversions), calculated at the time of grant.

(10).

(a).

The company must maintain a Register of Employee Stock Options in Form SH-6.

This register must record all details of ESOP options granted under Section 62(1)(b).

The entries must be made immediately (forthwith) whenever options are granted.

(b).

The Register of Employee Stock Options must be kept at the registered office of the company, or any other place decided by the Board of Directors.

(c).

All entries in the register must be authenticated (signed/verified) by the company secretary, or any other person authorised by the Board for this purpose.

(11).

If a company’s equity shares are listed on a recognised stock exchange, then:

Its Employee Stock Option Scheme (ESOP) must comply with the SEBI regulations made specifically for ESOPs.

So, listed companies must follow SEBI’s ESOP framework, not just the Companies Act rules.

(12A).

This rule relates to rights issues under Section 62(1)(a).

When a company offers shares to existing shareholders (a rights offer), the offer period must be:

At least 7 days from the date of the offer.

So , shareholders must be given a minimum of seven days to decide whether they want to accept or decline the offer.

The offer period cannot be shorter than 7 days.

Rule 13. Issue of shares on preferential basis.

(1).

A company may issue shares in any manner, including by way of a preferential offer.

This is allowed only if the company is authorised by a special resolution passed in a general meeting.

Shares on a preferential basis may be issued to any persons, whether or not they include the persons mentioned in Section 62(1)(a) / 62(1)(b).

62(1)(a) refers to Rights Issue and 62(1)(b) refers to ESOPs.

Any preferential issue must also comply with the requirements of section 42 (private placement rules).

Relaxation for offers made only to existing members

If the preferential offer is made only to one or more existing members, then:

Rule 14(1) of the Companies (Prospectus and Allotment of Securities) Rules, 2014, and the proviso to Rule 14(3) do not apply.

Essentially , some private placement procedural requirements are relaxed when preferential shares are offered only to existing shareholders.

Valuation for Listed Companies

If the company is listed, the price of shares issued on a preferential basis does not need to be determined by a registered valuer’s report.

Listed companies follow SEBI pricing guidelines, so a valuer’s report is not required under this rule.

Explanation:

Preferential Offer refers to:

An issue of shares or other securities to a select person or a selected group of persons.

These are issued on a preferential basis and not offered to all shareholders or the public

A preferential offer does NOT include the following types of issues:

Public issue

Rights issue

Employee Stock Option Scheme (ESOS)

Employee Stock Purchase Scheme (ESPS)

Sweat equity shares.

Bonus shares.

Depository receipts issued outside India.

Foreign securities

Shares or other securities include:

Equity shares.

Fully convertible debentures.

Partly convertible debentures.

Any other security that can later be:

Converted into equity shares, or exchanged for equity shares

(2).

If a company’s shares or other securities are listed on a recognised stock exchange, any preferential offer must follow:

The provisions of the Companies Act, and the SEBI regulations applicable to preferential issues.

If the company’s shares are not listed, then the preferential offer must follow:

The provisions of the Companies Act, and the rules made under the Act, and must also comply with the following conditions:

(a).

The company’s articles of association must permit the issue of shares or securities on a preferential basis.

(b).

The preferential issue must be approved by the shareholders through a special resolution.

(c).

All securities allotted through the preferential offer must be fully paid up at the time of allotment.

(d).

The company must include the following disclosures in the explanatory statement attached to the notice of the general meeting (under section 102) when making a preferential offer:

(i). The objects or purpose of the issue.

(ii). The total number of shares or other securities proposed to be issued.

(iii). The price or price band at/within which the allotment is proposed, (Essentially is the range of the price)

(iv) The basis for determining the price, along with the valuation report of the registered valuer.

(v). The relevant date used for calculating the price.

(vi). The class or classes of persons to whom the allotment is proposed.

(vii). Whether the promoters, directors, or key managerial personnel intend to subscribe to the offer.

(viii). The expected time period within which the allotment will be completed.

(ix). The names of the proposed allottees and the percentage of post-preferential share capital they may hold/

(x). Any change in control of the company that may occur because of the preferential offer.

(xi). The number of persons who have already received allotment on a preferential basis during the year, including:

The number of securities allotted, and the price at which they were allotted.

(xii). The justification for issuing securities for non-cash consideration, along with the valuation report of the registered valuer.

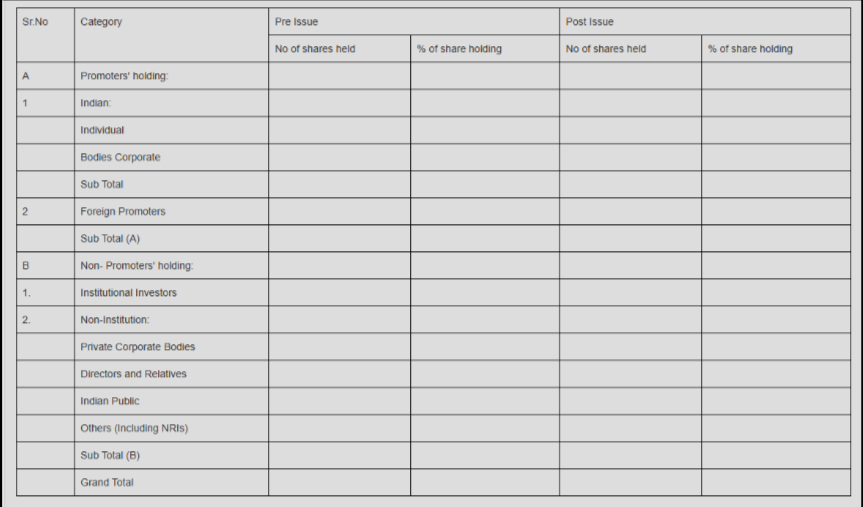

(xiii) The pre issue and post issue shareholding pattern of the company in the following format:

(e).

The allotment of securities issued on a preferential basis must be completed within 12 months from the date the special resolution was passed.

Please do note that this issue has to be approved through the special resolution under rule 13(2)(b))

(f)

If the company does not complete the allotment within 12 months, it must pass another special resolution before proceeding further.

(g)

When a company issues shares or other securities on a preferential basis, it must determine their price properly.

This rule applies regardless of whether the securities are issued for cash or for non-cash consideration.

The price must be based on a valuation report.

This valuation report must be prepared by a registered valuer.

(h)

When a company issues convertible securities on a preferential basis , the price of the resulting equity shares must be determined in one of the following ways:

(i)

The price may be fixed upfront at the time the convertible securities are offered.

The price will be based on the valuation report of a registered valuer prepared at that time.

(ii)

Alternatively, the price may be determined at a later time, which must be:

Not earlier than 30 days before the date the holder becomes entitled to apply for equity shares.

This will be based on a valuation report of a registered valuer that is not older than 60 days from that entitlement date.

The company must decide at the time of offering the convertible securities whether it is choosing option (i) or option (ii).

Their choice must be disclosed under sub-clause (v) of clause (d) of Rule 13(2).

(i)

If shares or other securities are being allotted for consideration other than cash then:

The valuation of such non-cash consideration must be carried out by a registered valuer, who shall give a valuation report with justification.

(j)

If the preferential offer involves non-cash consideration, it must be accounted for as follows:

(i).

If the non-cash consideration is a depreciable or amortizable asset then:

It must be recorded in the balance sheet of the company as per applicable accounting standards.

(ii).

If the non-cash consideration is not a depreciable or amortizable asset then j(i) does not apply instead:

The value of that non-cash consideration must be treated as an expense, and must be recorded according to the applicable accounting standards.

Explanation:

However, if a registered valuer has not yet been appointed as per the Act, companies still need a valid valuation.

In such cases, the valuation report must be prepared by one of the following:

An independent merchant banker registered with SEBI.

An independent Chartered Accountant in practice with at least 10 years of experience.

(3).

When a company issues shares or other securities on a preferential basis, the pricing must follow certain rules.

A registered valuer must determine the fair value of the securities and give a valuation report.

The company cannot issue the shares or securities at a price lower than the value determined in that valuation report.

Rule 14. Issue of Bonus Shares.

When the Board of Directors makes a decision to recommend a bonus issue, and this decision is publicly announced, it becomes binding.

After the announcement, the company cannot withdraw or cancel the proposed bonus issue.

Rule 15. Notice to Registrar for alteration of share capital.

When a company alters its share capital in any of the ways mentioned under Section 61(1), it must inform the Registrar.

If the Government passes an order increasing the company’s authorised share capital under Section 62(4) read with Section 62(6), the company must also file notice of this change.

When a company redeems any redeemable preference shares, it must similarly notify the Registrar.

If a company does not have share capital but increases its number of members, this change must also be reported.

In all these situations, the company must file a notice of alteration, increase, or redemption with the Registrar.

The notice must be filed in Form No. SH.7.

The required fee must be submitted along with the form.

To Access Form - SH-7: