Share Capital & Debenture Rules (Rule 16-19)

Rule 16. Provision of money by company for purchase of its own shares by employees or by trustees for the benefit of employees.

(1).

The company cannot give or set aside money to buy its own shares or its holding company’s shares.

This applies when the shares are being bought by trustees.

The trustees are buying the shares to hold them for employees or for the benefit of employees.

The company can provide such money only if it follows the following conditions.

(a).

Money can be provided for buying or subscribing to the shares only if the scheme is approved by the members.

The approval must be given through a special resolution.

This special resolution must be passed in a general meeting of the members.

(b).

If the company’s shares are listed, the shares must be purchased only through a recognized stock exchange.

The company cannot buy these shares through private offers or private arrangements.

(c).

If the company’s shares are not listed on a recognized stock exchange, the purchase price must be determined through a valuation.

This valuation must be done by a registered valuer.

(d).

The total value of the shares being purchased or subscribed is counted together with the money the company provides.

This combined amount must not go beyond 5% of the company’s paid-up capital and free reserves.

(2).

The explanatory statement attached to the notice of the general meeting (as required under section 102) must include extra details.

These extra details are in addition to the information already required under Rule 18(1).

The statement must specifically contain the additional particulars listed after this clause.

(a).

It must specify which class or category of employees will benefit from the scheme.

It must also state that money is being provided for buying or subscribing to shares for these employees.

(b).

It must include details of the trustee or the employees in whose name the shares will be registered.

(c).

It must provide details of the trust involved in the scheme.

It must include the name, address, occupation, and nationality of each trustee.

It must state whether any trustee has a relationship with the promoters, directors, or key managerial personnel, if such a relationship exists.

(d).

It must disclose whether any key managerial personnel, directors, or promoters have an interest in the scheme or the trust.

It must also explain the impact or effect of such interest.

(e).

It must provide detailed information on the benefits that employees will receive from the implementation of the scheme.

(f).

It must specify who will exercise the voting rights attached to the shares purchased or subscribed under the scheme.

It must also explain how those voting rights will be exercised.

(3).

A person shall not be appointed as a trustee to hold such shares, if he:

(a).

The person is a director, key managerial personnel, or promoter of the company, or of its holding, subsidiary, or associate company.

The person is a relative of such director, key managerial personnel, or promoter.

(b).

The person beneficially owns 10% or more of the company’s paid-up share capital.

(4).

If the employees do not directly exercise the voting rights for the shares under the scheme, the Board of Directors must report certain details.

These details must be included in the Board’s report for the relevant financial year.

The information to be disclosed are:

(a). The names of the employees who did not cast their votes themselves.

(b). The reasons why these employees did not vote directly.

(c). The name of the person who voted on their behalf.

(d). How many shares are held for these employees, and what percentage that represents of the company’s total paid-up share capital.

(e). The date of the general meeting where the voting took place.

(f). The resolutions on which the representative cast votes.

(g). The percentage of voting power used on each resolution compared to the company’s total voting power.

(h). Whether the votes were cast in support of or against each resolution.

Rule 17. Buy-back of shares or other securities.

Unless a different rule is specifically provided, private companies and unlisted public companies must follow these norms.

These norms apply to how such companies can buy back their securities.

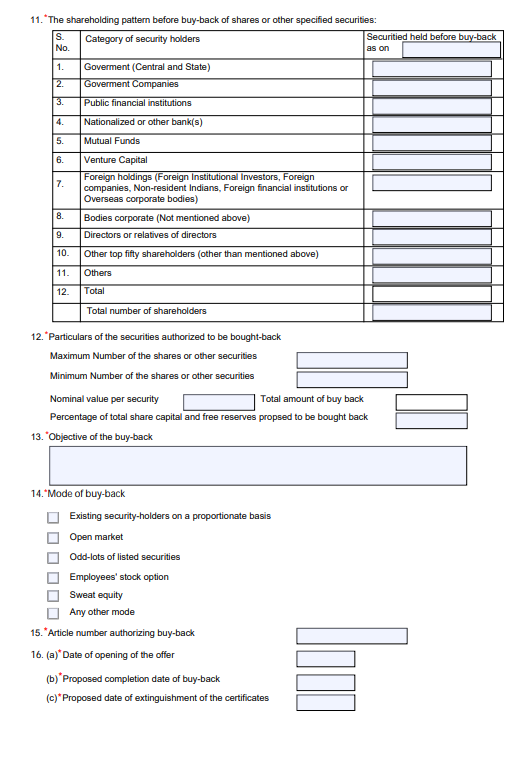

(1).

(a).

The date on which the Board of Directors approved the buy-back proposal.

(b).

The purpose or reason for carrying out the buy-back.

(c).

The category or type of shares or securities the company plans to buy back.

(d).

The total number of securities the company intends to buy back.

(e).

The method the company will use for the buy-back.

(f).

The price at which the buy-back will be carried out.

(g).

How the company determined or calculated the buy-back price.

(h).

The maximum amount the company will spend on the buy-back and the source of funds that will be used.

(i).

The deadline or time period within which the buy-back must be completed.

(j).

(i).

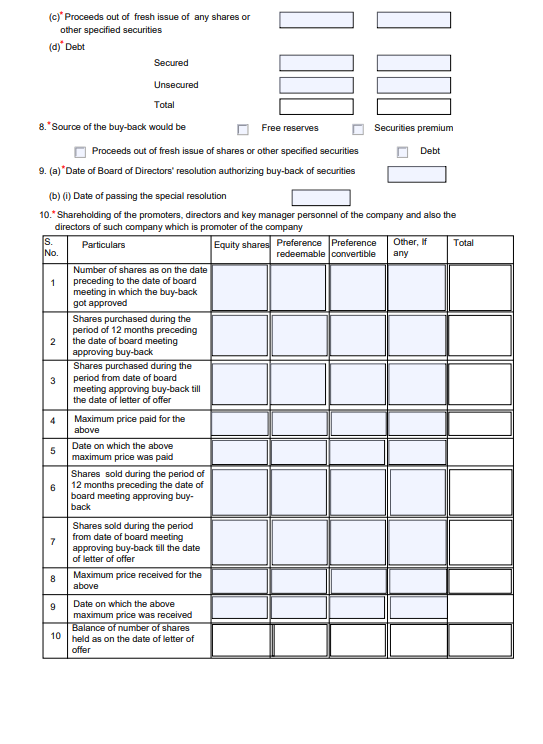

The total shareholding of the promoters must be disclosed.

If the promoter is a company, the shareholding of its directors must also be included.

The shareholding of the company’s own directors and key managerial personnel must also be disclosed.

All these details must be stated as on the date of the notice calling the general meeting.

(ii).

The total number of equity shares bought or sold by the persons mentioned in sub-clause (i) must be disclosed.

This includes transactions made in the 12 months before the board meeting where the buy-back was approved.

It also includes transactions made from the date of that board meeting up to the date of the notice calling the general meeting.

(iii).

The maximum and minimum price at which purchases and sales referred to in sub-clause (ii) were made along with the relevant date;

(k).

If the persons listed in sub-clause (i) of clause (j) plan to offer their shares in the buy-back:

(i).

They must disclose how many shares they intend to tender.

(ii).

They must provide details of all their share transactions and holdings for the last 12 months before the board meeting where the buy-back was approved, including:

The number of shares acquired.

The price at which they were acquired.

The date of each acquisition.

(l).

A confirmation must be given that the company has no outstanding defaults.

This includes no default in repaying deposits or paying interest on them.

No default in redeeming debentures or paying interest on debentures.

No default in redeeming preference shares or paying any dividend that is due.

No default in repaying term loans or paying interest to any financial institution or bank.

(m).

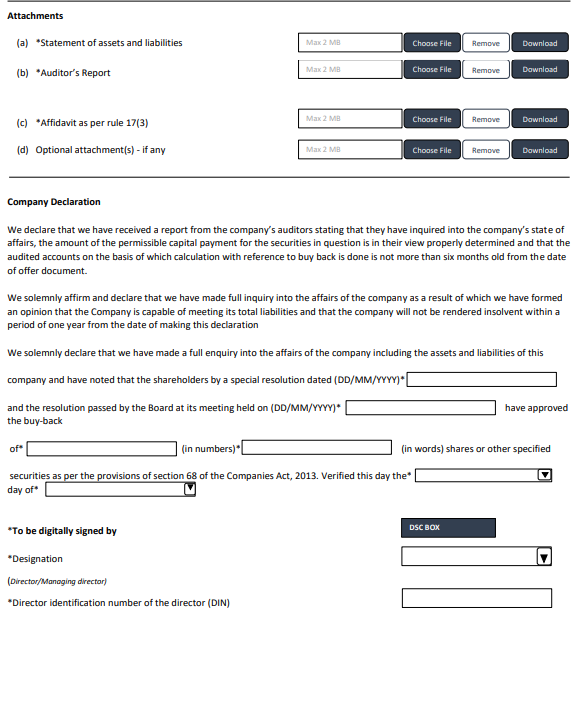

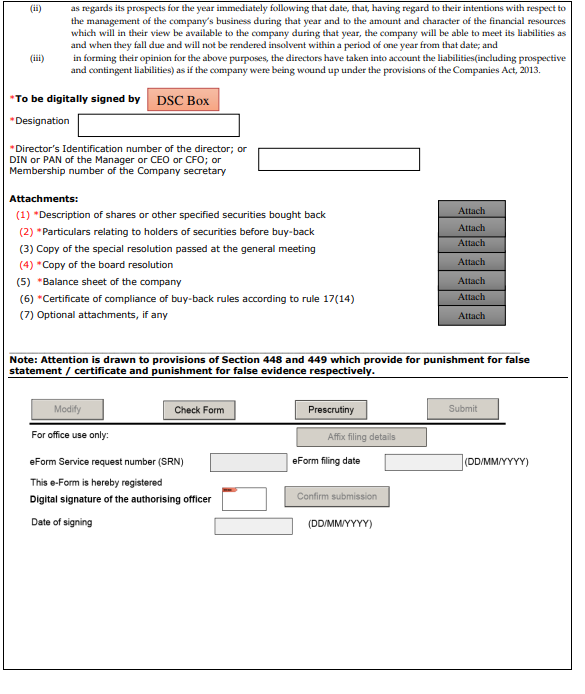

A confirmation must be given that the Board of Directors has thoroughly examined the company’s affairs and future prospects.

The Board must also confirm that, after this enquiry, that they have formed the required opinion:

(i).

The Board must confirm that the company’s financial position has been assessed.

Based on this assessment, the Board believes that immediately after the date the general meeting is convened:

The company will have no grounds to be considered unable to pay its debts.

They will considered capable of meeting the debt requirements.

(ii).

The Board must assess the company’s prospects for the year following that date.

They must consider how they plan to manage the company’s business during that year.

They must also consider what financial resources will be available to the company.

Based on this, they must confirm that the company will be able to pay its liabilities as they become due.

They must also confirm that the company will not become insolvent within one year from that date.

(iii).

The directors have considered all the company’s liabilities.

This includes current liabilities, future (prospective) liabilities, and contingent liabilities.

They have evaluated these liabilities as if the company were being wound up under the Companies Act, 2013.

(n).

A report addressed to the Board of directors by the company’s auditors stating that:

(i).

They have inquired into the company’s state of affairs.

(ii).

The amount of the permissible capital payment for the securities in question is in their view properly determined.

(iii).

The audited financial statements used to calculate the buy-back must be no older than six months from the date of the offer document.

If the audited accounts are older than six months:

The buy-back calculations must be based on unaudited accounts that are not older than six months from the date of the offer document.

These unaudited accounts must undergo a limited review by the company’s auditors.

(iv).

The Board of Directors confirms that the opinion mentioned in clause (m) has been formed on reasonable grounds.

They believe, based on the company’s current financial position, that the company will not become insolvent within one year from that date.

(2).

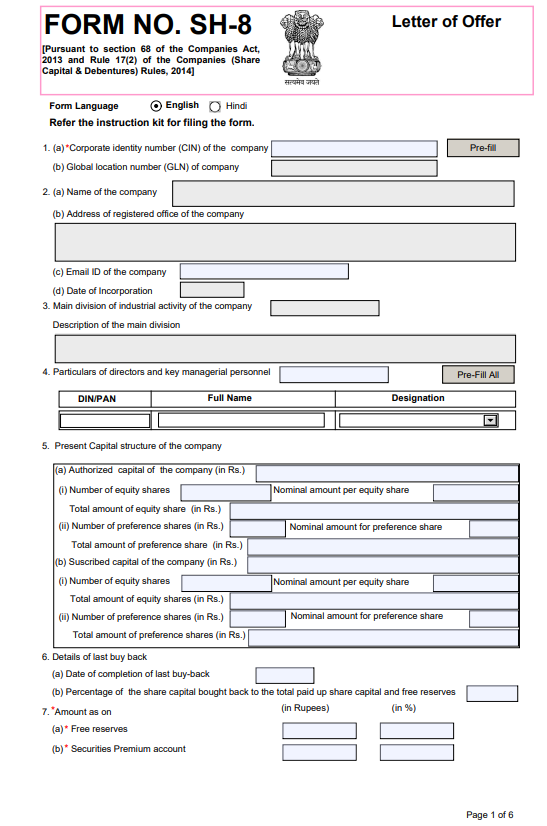

A company approved through a special resolution must file a letter of offer with the Registrar of Companies before proceeding with the buy-back.

The letter of offer must be submitted in Form SH.8, along with the required fee.

The letter of offer must be dated and signed by at least two directors.

One of the signatories must be the managing director, if the company has one.

(3).

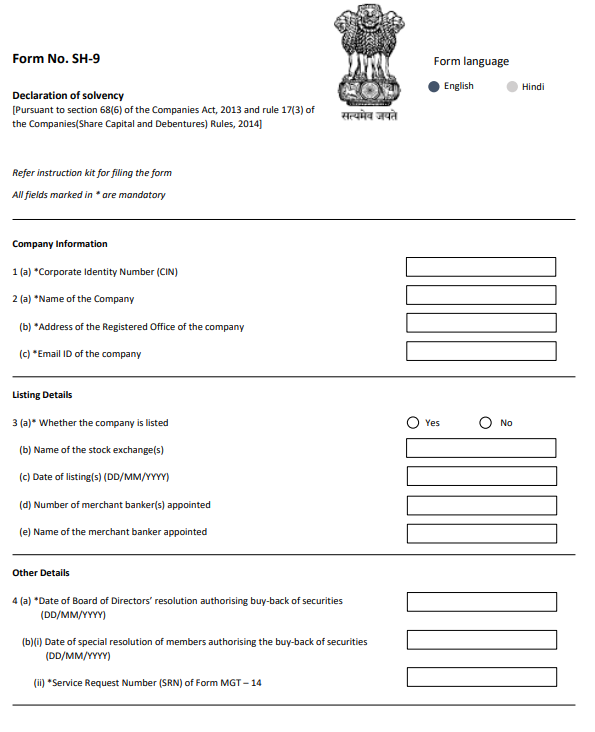

The company must file a declaration of solvency together with the letter of offer.

A listed company must file this declaration with both the Registrar of Companies and SEBI; an unlisted company files only with the Registrar.

The declaration must be in Form SH.9 and submitted with the required fee.

It must be signed by at least two directors.

One of the signatories must be the managing director, if the company has one.

The declaration must also be verified through an affidavit, as required in the form.

(4).

The company must send the letter of offer to all shareholders or security holders right after it is filed with the Registrar of Companies.

The dispatch must happen within 20 days from the date of filing the letter of offer with the Registrar.

(5).

The buy-back offer must stay open for at least 15 days and not more than 30 days from the date the letter of offer is sent.

However, if all members of the company agree, the offer can be kept open for less than 15 days.

(6).

If shareholders offer more shares than the company has decided to buy back, the company cannot accept all of them.

In such a case, each shareholder’s offer will be accepted proportionately.

So each shareholder will have only a proportion of their offered shares bought back, based on the total shares offered.

(7).

The company must verify all the buy-back offers within 15 days from the date the offer period closes.

Any shares or securities submitted for buy-back will be considered accepted by default.

They will only be treated as rejected if the company specifically communicates a rejection within 21 days from the date the offer closes.

(8).

Right after the buy-back offer period closes, the company must open a separate bank account.

The company must deposit into this account the full amount that will be payable to shareholders for the shares they have tendered.

The amount deposited should cover the entire consideration required for the buy-back as per the rules.

(9).

The company shall within seven days of the time specified in Rule 17(7):

(a). The company must pay cash to those shareholders or security holders whose shares or securities have been accepted in the buy-back.

(b). The company must return the share certificates to those whose securities were not accepted, either entirely or return the remaining certificates in cases where only part of their securities were accepted.

(10).

The company shall ensure that:

(a).

The letter of offer must include information that is true, factual, and relevant.

It must not contain any false or misleading statements.

The letter must clearly state that the company’s directors take responsibility for all the information provided in the document.

(b).

From the date the special resolution authorizing the buy-back is passed until the buy-back offer closes, the company cannot issue any new shares.

This includes bonus shares or any other type of new share issuance.

The only exception is shares that arise from already existing convertible instruments.

(c).

The company must confirm in the offer document that it has opened a separate bank account specifically for the buy-back.

This account must be adequately funded to cover the entire buy-back amount.

The company must also state that all payments for the buy-back will be made only in cash.

(d).

The company shall not withdraw the offer once it has announced the offer to the shareholders.

(e).

The company shall not utilize any money borrowed from banks or financial institutions for the purpose of buying back its shares.

(f).

The company shall not utilize the proceeds of an earlier issue of the same kind of shares or same kind of other specified securities for the buy-back.

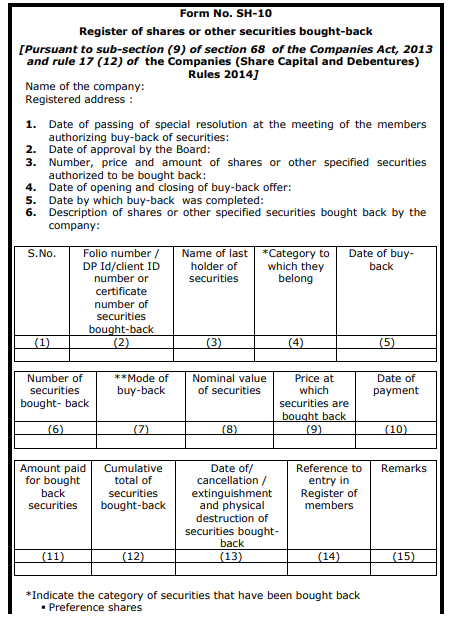

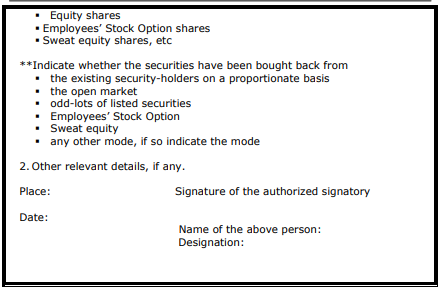

(12).

(a).

The company, shall maintain a register of shares or other securities which have been bought-back in Form No. SH.10.

(b).

The company must maintain a register of all shares or securities that have been bought back.

This register must be kept at the company’s registered office.

It must be in the custody of the company secretary or any other person whom the Board authorizes for this purpose.

(c).

The entries in the register shall be authenticated by the secretary of the company or by any other person authorized by the Board for the purpose.

(13).

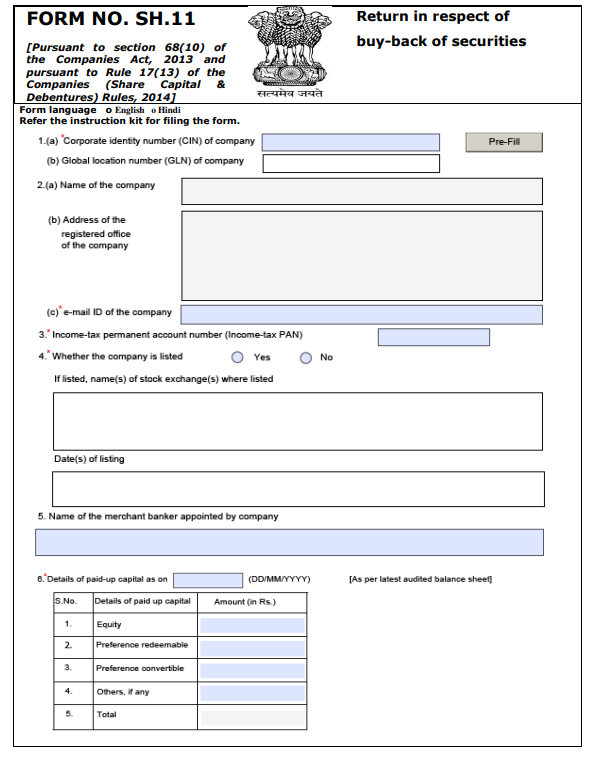

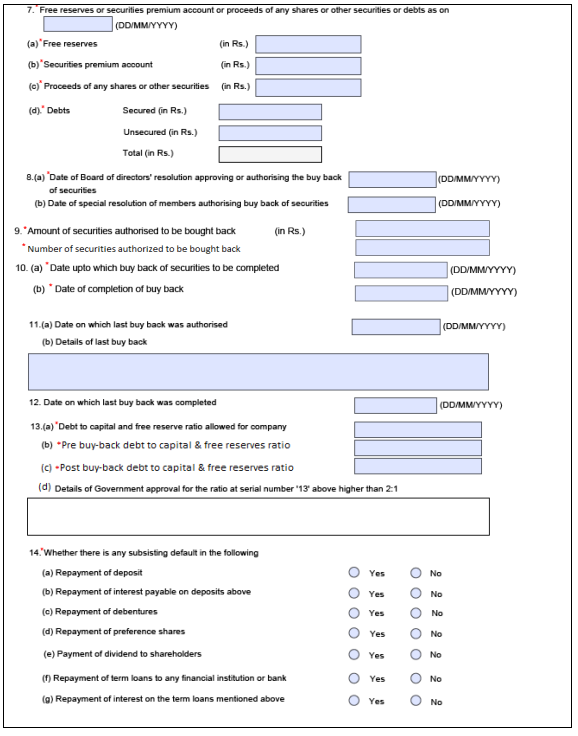

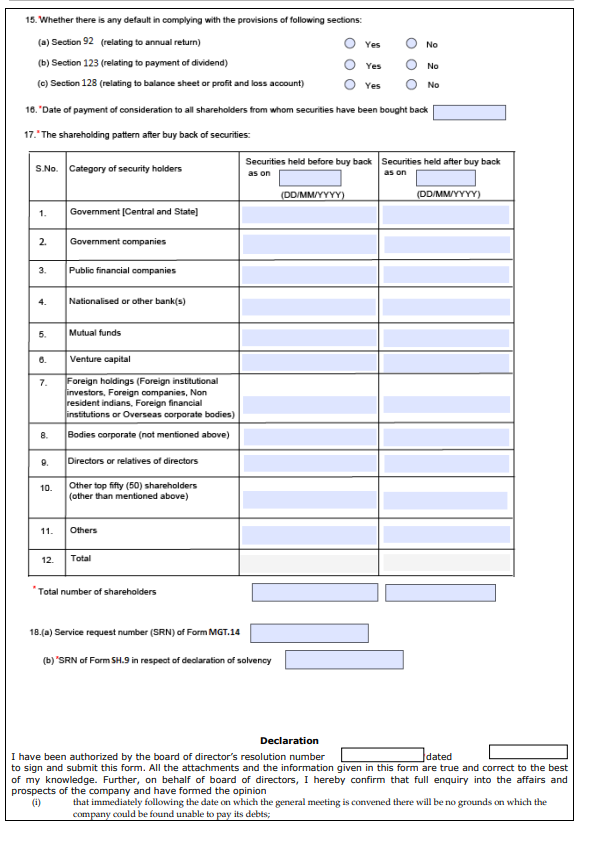

After completing the buy-back, the company must file a return in Form SH.11.

An unlisted company must file this return with the Registrar of Companies.

A listed company must file it with both the Registrar and SEBI.

The return must be submitted along with the required fee.

(14).

The company must file a return of buy-back with the Registrar in Form SH.11.

This return must include a declaration confirming that the buy-back has been carried out according to the Act and the applicable rules.

The declaration must be signed by two directors, and one of them must be the managing director, if the company has one.

To Access Form SH -8: https://ca2013.com/wp-content/uploads/2015/08/Form_SH-8.pdf

Please note that this form has to be filed online with the MCA Portal.

To Access Form SH -9: https://ca2013.com/wp-content/uploads/2023/01/Form-SH-9.pdf

Please note that this form has to be field online with the MCA Portal.

To Access Form SH -10: https://ca2013.com/returns/sh-10/

Please note that this form has to be field online with the MCA Portal.

To Access Form SH -11: https://ca2013.com/wp-content/uploads/2015/07/sh-11.pdf

Please note that this form has to be field online with the MCA Portal.

Rule 18. Debentures.

(1).

The company shall not issue secured debentures, unless it complies with the following conditions:

(a).

A company may issue secured debentures, but the redemption period cannot be more than 10 years from the date they are issued.

Provided that the following types of companies are allowed to issue secured debentures for a longer period up to 30 years instead of 10 years:

(i). Companies involved in developing or setting up infrastructure projects.

(ii). Infrastructure Finance Companies (IFCs) as defined under RBI’s Non-Banking Financial Companies Prudential Norms, 2007.

(iii). Infrastructure Debt Fund – NBFCs, as defined under the RBI’s Infrastructure Debt Fund NBFC Directions, 2011.

(iv). Any company that has been specifically permitted by:

A Ministry or Department of the Central Government.

The Reserve Bank of India.

The National Housing Bank.

Any other statutory authority, to issue debentures for a period longer than 10 years (but not exceeding 30 years).

(b).

The company must create a security charge over its properties or assets, or those of its subsidiaries, holding company, or associate companies.

The value of these assets must be adequate to cover the full repayment of the debenture amount along with the interest

(c).

The company must appoint a debenture trustee before issuing the prospectus or letter of offer for inviting people to subscribe to its debentures.

After the debentures are allotted, the company must execute a debenture trust deed within 60 days.

(d).

The security for the debentures must be created in favour of the debenture trustee.

This security can be created through a charge or mortgage on the following:

(i).

Any specific movable property of the company, its holding company, its subsidiaries, or its associate companies, or any other movable asset.

(ii).

Any specific immovable property, wherever it is located, or any interest in such immovable property.

In the case of a non-banking financial company (NBFC), the charge or mortgage mentioned in sub-clause (i) can be created on any movable property, without restriction.

If a Government company issues debentures that are fully secured by a guarantee from the Central Government, one or more State Governments, or both, then no charge needs to be created on assets under this rule.

If a subsidiary company takes a loan from a bank or financial institution, the required charge or mortgage may be created on the assets or properties of its holding company as well.

(2).

The company must appoint debenture trustees under section 71(5).

Before doing so, the company must make sure that certain conditions are fulfilled.

The conditions that must be complied with are listed below:

(a).

The names of the debenture trustees must be clearly mentioned in the letter of offer inviting people to subscribe to the debentures.

Their names must also be included in all later notices or communications sent to debenture holders.

(b).

Before appointing a debenture trustee, the company must obtain written consent from the person(s) proposed to be appointed as debenture trustee(s).

The letter of offer inviting subscription to the debentures must clearly state that such written consent has been obtained.

(c).

A person shall not be appointed as a debenture trustee, if he:

(i). One who beneficially holds shares in the company.

(ii). A promoter, director, KMP, officer, or employee of the company or its group entities.

(iii). One who is entitled to receive any money from the company other than trustee remuneration.

(iv). One who is indebted to the company or its group entities.

(v). One who has given a guarantee for the principal or interest of the debentures.

(vi).

The person has a pecuniary (financial) relationship with the company.

The value of that relationship is 2% or more of the company’s gross turnover or total income.

The value is ₹50 lakh or more (or any higher amount prescribed).

The relationship existed during either of the two immediately preceding financial years or during the current financial year.

(vii). Is relative of any promoter or any person who is in the employment of the company as a director or key managerial personnel

(d).

The Board may fill any casual vacancy in the office of the debenture trustee.

Until the vacancy is filled, the remaining trustee or trustees can continue to act.

If the vacancy occurred because the debenture trustee resigned, the Board can fill the vacancy only with the written consent of the majority of the debenture holders.

(e).

A debenture trustee can be removed before their term ends.

Removal requires approval from the debenture holders.

The approval must come from holders representing not less than 75% (three-fourths in value) of the outstanding debentures.

This approval must be given at a meeting of the debenture holders.

(3).

It shall be the duty of every debenture trustee to:

(a).

Ensure that the letter of offer does not include anything that conflicts with the terms of the debenture issue or with the trust deed.

(b).

Ensure that the covenants in the trust deed do not harm or negatively affect the interests of the debenture holders.

(c).

Request regular status or performance reports from the company.

(d).

Inform the debenture holders promptly about any defaults in interest payment or debenture redemption, and update them on the actions taken by the trustee in response.

(e).

Appoint a nominee director to the company's Board in any of the specified default situations.

(i).

When the company fails to pay interest to debenture holders on two consecutive occasions.

When the company fails to redeem the debentures when due.

(ii.

A situation where the company fails to create the required security for the debentures.

(iii).

A situation where the company fails to redeem the debentures when they become due.

(f).

Ensure that the company does not violate any terms of the debenture issue or any covenant in the trust deed.

Take reasonable and necessary steps to correct or remedy any breach if it occurs.

(g).

Immediately inform the debenture holders if any term of the debenture issue or any covenant of the trust deed has been breached.

(h).

Ensure that all conditions related to creating the security for the debentures (if security is required) are properly implemented.

Ensure that the company complies with the requirements for creating and maintaining the Debenture Redemption Reserve (DRR).

(i).

Ensure that the company’s assets and the guarantors’ assets, if any are always sufficient to cover the interest and principal payable on the debentures.

Ensure that these assets remain free from any encumbrances, except those that the debenture holders have specifically agreed to.

(j).

Take all required actions when the security for the debentures becomes enforceable.

(k).

Call for reports on the utilization of funds raised by the issue of debentures.

(l).

Take necessary steps to call and hold a meeting of the debenture holders whenever such a meeting is required.

(m).

Ensure that the debentures are converted or redeemed exactly as per the terms and conditions under which they were issued.

(n).

Take all actions necessary to protect the interests of the debenture holders.

Perform any additional steps required to address and resolve the grievances of debenture holders.

(4).

The debenture trustee must call a meeting of all debenture holders in the following situations:

(a).

A meeting must be called if debenture holders, holding at least 10% of the total value of outstanding debentures, make a written request asking for it.

(b).

A meeting must be called if an event happens that amounts to a breach or default.

A meeting must also be called if the debenture trustee believes that any event has occurred which affects the interests of the debenture holders.

(5).

The company issuing the debentures must execute a trust deed in Form SH.12 (or in a format very similar to it).

This trust deed must be executed in favour of the debenture trustees.

It must be completed within 60 days from the allotment of debentures.

In any case, it must be executed within three months from the closure of the issue or offer, whichever applies.

(6).

The requirements mentioned in sub-rules (2) to (5) of rule 18 do not apply when debentures are issued through a public offer.

(7).

The company must comply with the rules for creating and maintaining the Debenture Redemption Reserve (DRR).

The company must also follow the rules for investing or depositing the required amount for debentures that will mature in the next financial year.

The next financial year would be up to 31st March.

All of this must be done according to the following specific conditions

(a).

DRR must be created out of the company’s profits that are available for paying dividends.

(b).

Rules for how much DRR is required and when money must be invested or deposited are as follows:

(i).

No DRR is required for debentures issued by:

All India Financial Institutions regulated by RBI, and Banking companies

This applies to both public issues and privately placed debentures.

(ii). For other Financial Institutions (as defined in section 2(72) of the Companies Act, 2013), DRR requirements will be the same as those for NBFCs registered with RBI.

(iii).

For listed companies (except those mentioned in sub-clause (i)), no DRR is required in the following situations:

(A). Public issue of debentures:

A. When issued by NBFCs registered under section 45-IA of RBI Act, 1934 and Housing Finance Companies registered with National Housing Bank.

B. When issued by any other listed company.

(B). Privately placed debentures

No DRR is required for the same companies listed under A and B above.

(iv).

For unlisted companies (other than the institutions in sub-clause (i)):

(A). NBFCs registered with RBI and Housing Finance Companies do not need DRR when issuing privately placed debentures.

(B). All other unlisted companies must maintain a DRR equal to 10% of the value of outstanding debentures.

(v).

Companies covered under: (A) of sub-clause (iii)(b) or (B) of sub-clause (iv)(b) must on or before 30th April each year:

Invest or deposit at least 15% of the amount of debentures maturing during the next financial year (ending 31st March)

The investment or deposit must be made in one or more of the approved methods listed in sub-clause (vi).

It is provided that The invested/deposited amount must never fall below 15% of the amount of debentures maturing that year.

(vi). Approved investment/deposit options for sub-clause (v):

(A). Deposits with any scheduled bank, free from any charge or lien.

(B). Unencumbered Central or State Government securities.

(C). Unencumbered securities listed in section 20(a) to (d) and (ee) of the Indian Trusts Act, 1882.

(D). Unencumbered bonds issued by companies notified under section 20(f) of the Indian Trusts Act, 1882.

The amount invested or deposited under this clause can be used only for redeeming debentures that mature during that financial year.

(c)

For partly convertible debentures, DRR must be created only for the non-convertible portion.

(d)

Money credited to the DRR can be used only for redeeming debentures and cannot be used for any other purpose.

(8).

(a).

The trust deed created to secure any debenture issue must be available for inspection by any member or debenture holder of the company.

It must be open for inspection in the same way and to the same extent as the company’s register of members.

The person inspecting it must pay the same fee that applies to inspecting the register of members.

(b).

If any member or debenture holder requests a copy of the trust deed, the company must send it to them.

The copy must be provided within seven days of receiving the request.

The requester must pay the applicable fee for receiving the copy.

(9).

This rule does not apply to any money a company receives from issuing commercial paper.

It also does not apply to money received from issuing any other similar instrument.

These instruments must have been issued according to the guidelines, regulations, or notifications of the Reserve Bank of India (RBI).

(10).

This rule does not apply to foreign currency convertible bonds (FCCBs) or foreign currency bonds issued under the 1993 FCCB & Depository Receipt Scheme.

It also does not apply to such bonds issued under any regulations or directions of the Reserve Bank of India (RBI).

The only exception is when the Scheme, regulations, or RBI directions specifically state that this rule will apply.

(11).

This rule does not apply to rupee-denominated bonds issued only to overseas investors.

These bonds must be issued in accordance with RBI’s A.P. (DIR Series) Circular No. 17 dated 29 September 2015.

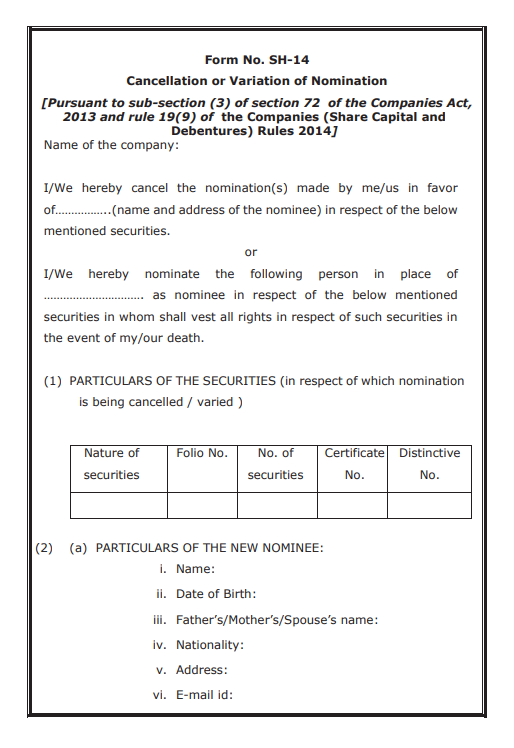

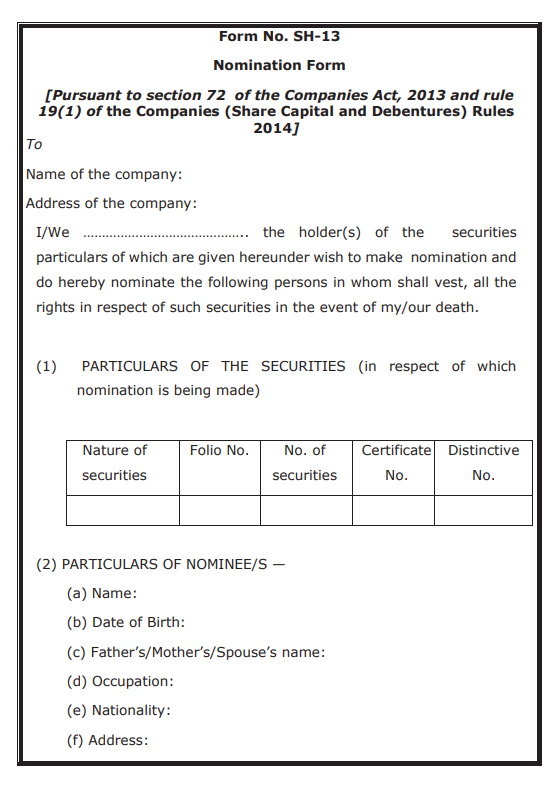

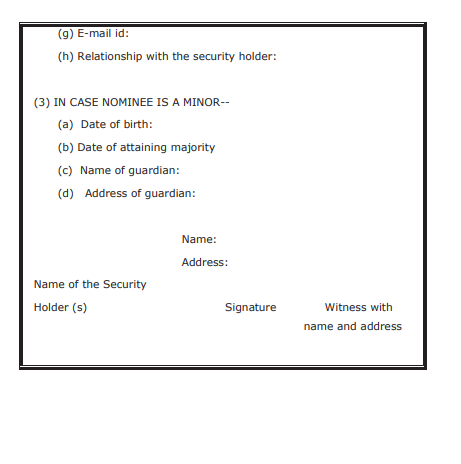

Rule 19. Nomination by securities holder.

(1).

Any person who holds securities of a company can nominate someone using Form SH.13.

The nominated person will receive or vest with those securities if the security holder dies.

(2).

Once the company receives the nomination form, it must immediately record the nomination.

This entry must be added in the relevant register of security holders maintained under section 88.

(3).

If securities are held jointly by more than one person, all the joint holders must together make the nomination.

They must nominate one person using Form SH.13.

(4).

The company must record the nomination request within two months from the date it receives the properly completed and signed nomination form.

(5).

If the security holder dies, or if securities are jointly held and all joint holders die, the nominated person can take action.

The nominee must provide whatever proof the Board asks for.

After providing the required evidence, the nominee can choose either of the options:

(a). To register himself as holder of the securities.

(b). To transfer the securities, as the deceased holder could have done.

(6).

If the nominee chooses to have the securities transferred and registered in his own name, he must inform the company in writing.

This written notice must be signed by the nominee.

The notice must also be submitted along with the death certificate of the deceased security holder(s).

(7).

All rules and restrictions under the Act that apply to transferring and registering the transfer of securities will also apply here.

These rules apply as if the original holder were still alive.

The notice or transfer made by the nominee will be treated as though it were a normal transfer signed by the deceased shareholder or debenture holder.

(8).

When the original holder dies, the nominee becomes entitled to the securities.

The nominee can receive all dividends, interest, and other financial or non-financial benefits attached to those securities.

These benefits are the same as those a registered holder would receive.

However, the nominee is not allowed to exercise membership rights (such as voting or participating in company meetings) until he is formally registered as the holder.

Only after registration can the nominee use rights that come with membership.

The Board can, at any time, issue a notice to the nominee asking him to choose either to get the securities registered in his own name or to transfer them to someone else.

The nominee must act on this notice within 90 days.

If the nominee does not comply within 90 days, the Board can stop all payments related to the securities.

This includes stopping dividends, interest, bonuses, or any other amounts payable on those securities.

These payments will remain withheld until the nominee complies with the Board’s notice.

(9).

The security holder who made the nomination can cancel it at any time.

The security holder can also change the nomination and appoint a new nominee.

To do this, the holder must give the company a notice of cancellation or change using Form SH.14.

(10).

The cancellation or change of nomination becomes effective on the date the company receives the notice.

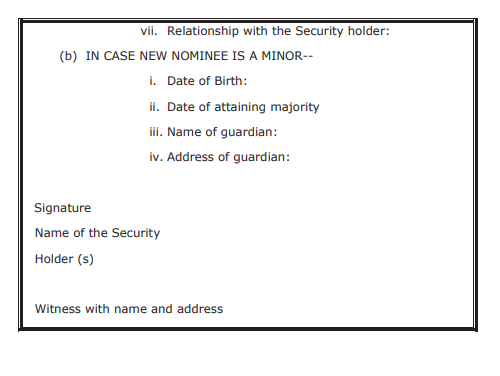

(11).

If the nominee is a minor, the security holder can appoint another person to take over if the minor nominee dies.

This appointment must be made in Form SH.13.

The appointed person will become entitled to the securities if the minor nominee passes away before reaching majority.

To Access Form SH-13: https://www.sebi.gov.in/sebi_data/commondocs/nov-2021/Form%20No.%20SH-13_p.pdf

Please note that the form should be filed online with the MCA portal.

To Access Form SH-14: https://www.sebi.gov.in/sebi_data/commondocs/nov-2021/Form%20No.%20SH-14_p.pdf

Please note that the form should be filed online with the MCA portal.