Acceptance of Deposit Rules - Part 2

Rule 4. Form and particulars of advertisements or circulars.

(1).

Companies accepting deposits from members under section 73(2) must issue a circular.

The circular must be sent to all members.

It must be sent by registered post with acknowledgment due, or by speed post, or by electronic mode.

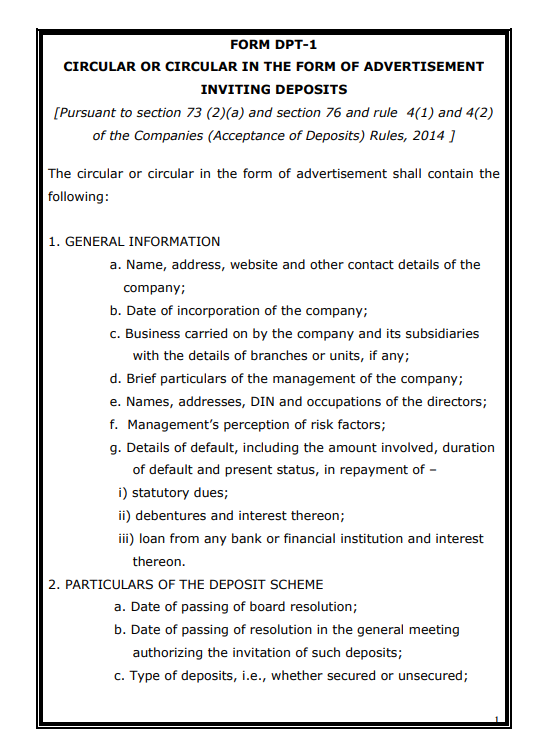

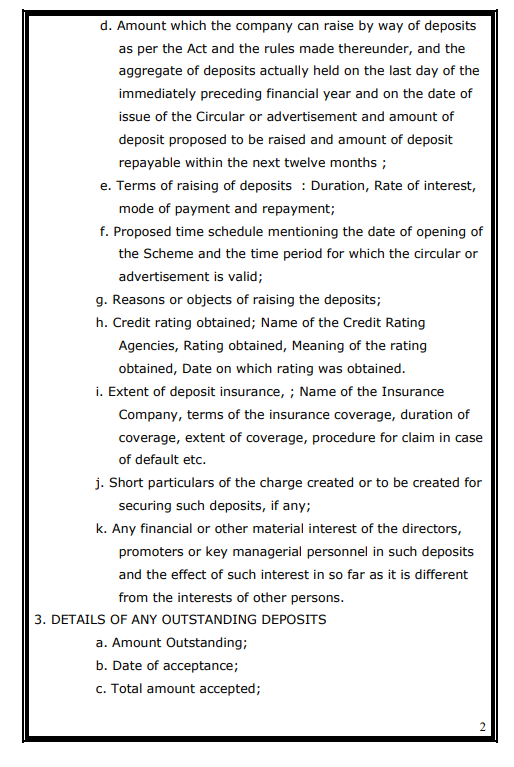

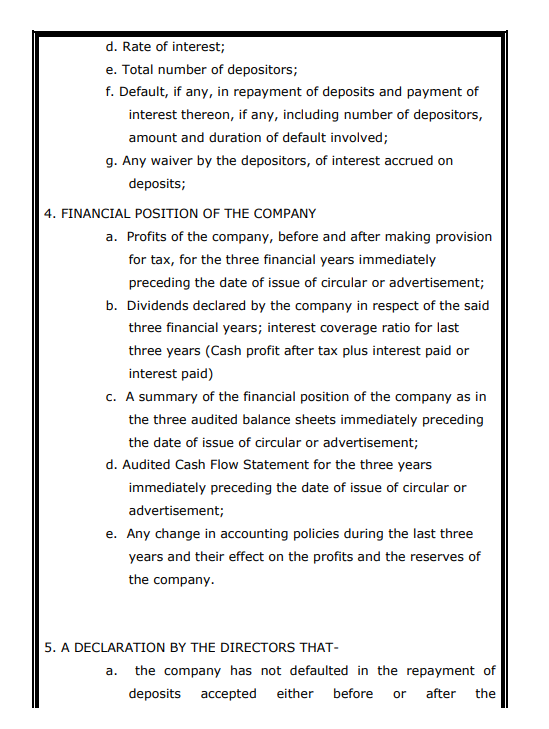

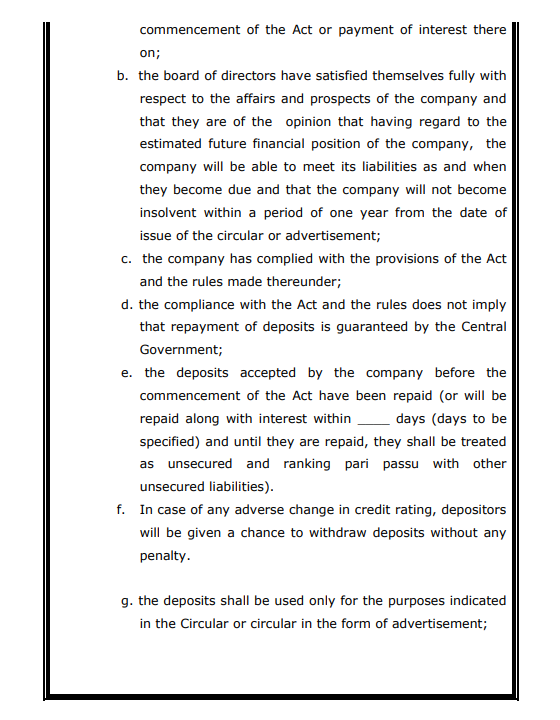

The circular must be in Form DPT-1.

Besides sending the circular to all members, the company may also publish the circular.

It may publish it in an English newspaper in the English language & publish in a vernacular newspaper in the regional language.

Both newspapers must have wide circulation in the state where the company’s registered office is located.

Form DPT-1 must include a certificate from the company’s statutory auditor.

The certificate must state that the company has not defaulted in repaying deposits or paying interest on them.

It does not matter , whether the deposits were taken before or after the Act began.

If the company had committed a default earlier, then a different declaration is required.

In that case, the statutory auditor must certify that the company has repaid the defaulted amount or paid the overdue interest.

The auditor must also confirm that five years have passed since the company corrected the default.

(2).

Eligible companies that want to invite public deposits must issue a circular in the form of an advertisement in Form DPT-1.

The advertisement must be published in an English newspaper in the English language with nationwide circulation.

It must also be published in a vernacular newspaper in the regional language.

The newspaper should have wide circulation in the state where the company’s registered office is located.

The company must also upload the circular on its website, if it has one.

(3).

Every company inviting deposits from the public shall upload a copy of the circular on its website, if any.

(4).

A company cannot issue a circular or an advertisement inviting deposits without proper authorisation.

No other person can issue or cause such a circular or advertisement to be issued on behalf of the company unless permitted.

The circular or advertisement must be issued only with the authority of the Board of Directors.

It must also be issued in the name of the Board of Directors.

(5).

A company cannot issue a circular or an advertisement inviting deposits unless certain steps are completed first.

At least 30 days before the circular or advertisement is issued, the company must send a copy to the Registrar for registration.

The copy sent to the Registrar must be signed by a majority of the directors who were on the Board when the circular was approved.

If the directors authorise someone else, their authorised agents may sign the copy instead.

The authorisation given to the agents must be in writing.

(6).

Once a company issues a circular or an advertisement inviting deposits, it is valid only for a limited period.

The circular remains valid up to the earlier of the following two dates:

Six months from the end of the financial year in which it was issued

The date on which the financial statements are laid before the company in the annual general meeting.

If the annual general meeting is not held, the circular remains valid only until the last date on which the AGM should have been held as per the Act.

After this validity period ends, the circular cannot be used.

The company must issue a fresh circular or advertisement every financial year if it wants to invite deposits during that year.

Explanation:

• For advertisements published in newspapers, the date of the newspaper issue is treated as the date of issue of the advertisement.

For circulars sent to members, the effective date of issue is the date on which the circular is dispatched.

These dates are used to determine validity periods and compliance timelines under the rule.

To Access Form DPT-1: https://ca2013.com/wp-content/uploads/2015/08/Form_DPT-1.pdf

Rule 5. Manner and Extent of Deposit Insurance - Omitted

Rule 6. Creation of Security

(1).

Companies accepting deposits from members under section 73(2), and eligible companies inviting secured deposits, must provide security for those deposits.

The security must be created by way of a charge on the company’s assets listed in Schedule III of the Act.

Intangible assets cannot be used for this purpose.

The value of the assets offered as security must be at least equal to the amount of the deposit that is not covered by deposit insurance.

If the deposits are secured by creating a charge on Schedule III assets (excluding intangible assets), the total of:

The amount of such secured deposits, and the interest payable on those deposits, cannot exceed the market value of the charged assets.

The market value must be determined by a registered valuer.

Example:

ABC Ltd wants to accept secured deposits.

It creates a charge on its land and building (Schedule III assets).

A registered valuer certifies that these assets are worth ₹5 crore.

The company wants to take ₹4 crore as secured deposits.

Deposit insurance covers ₹1 crore, so the uninsured portion is ₹3 crore.

Since the assets are worth ₹5 crore, they comfortably cover the uninsured amount.

Assume interest payable on the deposits will be ₹40 lakh.

Total liability = ₹4 crore + ₹0.40 crore = ₹4.40 crore, which is less than the asset value of ₹5 crore.

So the deposit is allowed.

If the company tries to take ₹5 crore, the total with interest would be ₹5.50 crore, which is more than the asset value of ₹5 crore.

This would not be permitted.

Explanation I:

The company needs to make sure that the total security available for the deposits is never less than the full amount of the deposits plus the interest payable on them.

This total security can come from:

Deposit insurance.

A charge on the company’s assets, or a combination of both.

If the combined value of the insurance and the asset charge is less than the deposit + interest amount, the company cannot accept the deposits.

Example:

ABC Ltd wants to accept deposits of ₹3 crore.

Interest payable over the period will be ₹30 lakh, so the total liability is ₹3.30 crore.

The rule says the company must ensure that the total security whether through deposit insurance, a charge on assets, or a combination of both is at least equal to ₹3.30 crore.

Suppose:

Deposit insurance covers ₹1 crore.

The company creates a charge on assets worth ₹2.5 crore.

Total security = ₹1 crore + ₹2.5 crore = ₹3.5 crore

Since ₹3.5 crore is more than ₹3.30 crore, the company complies with the rule.

If the total security had been less than ₹3.30 crore, the company could not accept the deposit.

Explanation. II

(1).

Since section 247(1) of the Act is not yet notified, and qualifications/experience requirements for valuers are not finalised, the valuation of stocks, shares, debentures, securities, etc. shall be done only by:

An independent merchant banker registered with SEBI.

An independent chartered accountant in practice with a minimum of ten years’ experience.

Update:

Section 247(1) of the Companies Act, 2013 is notified, but registered valuer rules are still being implemented.

Until the regime is fully operational, valuations of stocks, shares, debentures, and securities can be done by SEBI-registered independent merchant bankers.

It can also be done by independent chartered accountants with at least 10 years experience.

This interim arrangement remains valid for now.

(2).

The security required under Rule 6(1) cannot be in the form of a pledge.

This security must be created in favour of a trustee who represents the depositors.

The security must be created on identifiable assets of the company.

(a). It may be created on specific movable property of the company.

(b). It may be created on specific immovable property of the company, wherever it is situated.

It can be created on any interest the company has in such immovable property.

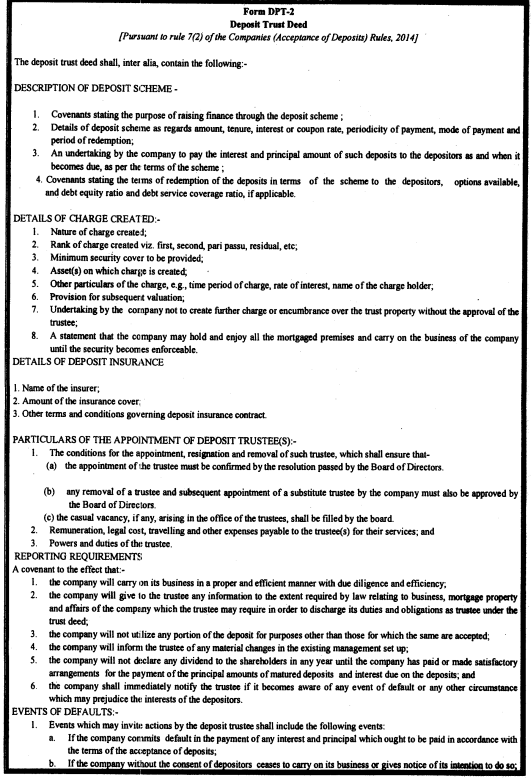

Rule 7. Appointment of trustee for depositors.

(1).

Companies accepting deposits from members under section 73(2) & Eligible companies accepting deposits under section 76:

Cannot issue any circular or advertisement inviting secured deposits unless they first appoint one or more trustees for the depositors.

These trustees are appointed to hold and manage the security that protects the depositors’ interests.

Before appointing a trustee for depositors, the company must obtain the trustee’s written consent.

The circular or advertisement inviting deposits must clearly state that the trustees for depositors have given their consent to act in that role.

This statement must be displayed with reasonable prominence so depositors are aware of it.

(2).

The company shall execute a deposit trust deed in Form DPT-2 at least seven days before issuing the circular or circular in the form of advertisement.

(3).

No person, including a company engaged in trusteeship services, may be appointed as a trustee for depositors if the proposed trustee:

(a). Is a director, key managerial personnel, officer or employee of the company, depositor or of its holding, subsidiary, or associate company.

(b). Is indebted to the company, its subsidiary, its holding company, its associate company, or any subsidiary of its holding company.

(c). Has any material pecuniary relationship with the company.

(d). Has entered into any guarantee arrangement relating to the principal amount of the deposits or the interest payable on them.

(e). Is related to any person covered under clause (a).

(4).

Once a circular or advertisement inviting deposits has been issued:

The trustee for depositors cannot be removed before the end of their term unless the Board approves it.

The removal must be approved by all directors who are present at the Board meeting.

If the company is required to have independent directors, then at least one independent director must be present at the meeting where the removal is approved.

To Access Form DPT -2: https://ca2013.com/returns/form-dpt-2/

Rule 8. Duties of trustees.

The trustee for depositors must:

(a). Make sure the company’s secured assets plus deposit insurance are enough to repay the principal and interest of secured deposits.

(b). Check that the circular or advertisement inviting deposits is accurate, matches the deposit scheme and trust deed, and follows the Act and rules.

(c). Ensure the company does not break any terms of the trust deed.

(d). Take reasonable steps to fix any breach of the trust deed or deposit terms.

(e). Arrange a meeting of depositors whenever such a meeting is required.

(f). Oversee whether the company has properly created security for deposits and complied with deposit insurance requirements.

(g). Act appropriately if the security for deposits needs to be enforced.

(h). Do whatever is necessary to protect depositors’ interests and resolve their complaints.

Rule 9. Meeting of depositors.

The trustee for depositors must call a meeting of all depositors when:

(a). The trustee receives a written request signed by depositors holding at least one-tenth of the total value of deposits outstanding at that time.

(b). Any event occurs that either causes a default, or in the trustee’s opinion, affects the interests of the depositors.

Rule 10. Form of application for deposits.

(1).

From the date these rules come into force, a company cannot accept or renew any deposit secured or unsecure without following a specific procedure.

The person who wants to make the deposit must first submit an application.

The application must be in the form specified by the company.

Only after receiving this application can the company accept or renew the deposit.

(2).

The application form mentioned in 10(1) must include a declaration from the person who wants to make the deposit.

In this declaration, the depositor must state that the deposit is not being made using money borrowed from someone else.

Rule 11. Power to nominate.

Every depositor has the right to nominate a person who will receive the deposit if the depositor dies.

This nomination can be made at any time.

When a nomination is made under this rule, the provisions of section 72 of the Companies Act will apply to it as far as possible.

Rule 12. Furnishing of deposit receipts to depositors.

(1).

Whenever a company accepts a new deposit or renews an existing one, it must issue a receipt to the depositor or to the depositor’s authorised agent.

The receipt must state the amount of money received by the company.

This receipt must be given within 21 days from:

The date the company receives the money,

The date the cheque is realised.

The date the deposit is renewed.

(2).

The deposit receipt mentioned in 12(1) must be signed by an officer of the company who has been authorised by the Board for this purpose.

• The receipt must clearly state the date on which the deposit was made.

• It must include the name and address of the depositor.

• It must mention the amount of the deposit received by the company.

• It must specify the rate of interest that the company will pay on that deposit.

• It must also state the date on which the deposit will be repaid.

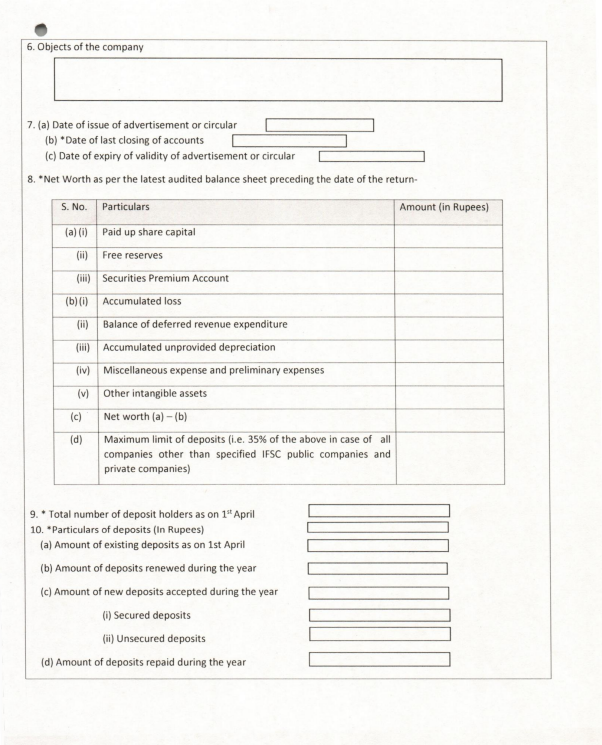

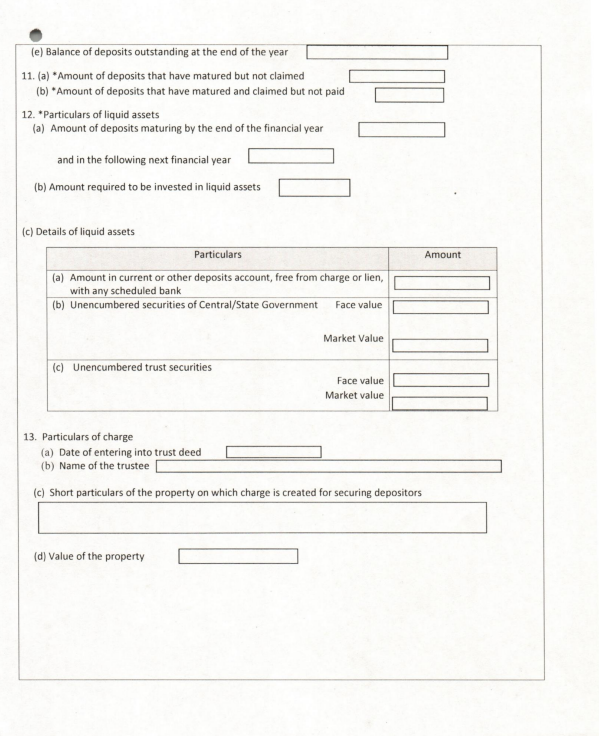

Rule 13. Maintenance of liquid assets and creation of deposit repayment reserve account.

Every company covered under section 73(2), and every eligible company, must make a mandatory deposit each year.

This deposit must be made on or before 30th April every year.

The amount to be deposited is the amount specified in section 73(2)(c) should be at least 20% of the deposits maturing during the financial year.

The money must be deposited with a scheduled bank.

The amount deposited cannot be used for any purpose other than repayment of deposits.

The deposit balance maintained with the bank must never fall below 20% of the total deposits maturing in that financial year, at any point in time.

Rule 14. Registers of deposits.

(1).

Every company accepting deposits shall maintain at its registered office one or more separate registers for deposits accepted or renewed.

These registers shall be entered separately in the case of each depositor the following particulars:

(a). Name, Address and PAN of the depositor/s.

(b). Particulars of guardian, in case of a minor.

(c). Particulars of the nominee.

(d). Deposit receipt number.

(e). Date and the amount of each deposit.

(f). Duration of the deposit and the date on which each deposit is repayable.

(g). Rate of interest or such deposits to be payable to the depositor.

(h). Due date for payment of interest.

(i). Mandate and instructions for payment of interest and for non-deduction of tax at source, if any.

(j). Date or dates on which the payment of interest shall be made.

(k). Omitted.

(l). Particulars of security or charge created for repayment of deposits.

(m). Any other relevant particulars;

(2).

Every company that accepts deposits from members under section 73(2), as well as every eligible company that accepts deposits from the public:

Needs to set aside a certain amount each year as a mandatory reserve for deposit repayment.

This amount must be deposited on or before the 30th day of April every year, without exception.

The amount that must be deposited is the amount referred to in section 73(2)(c).

With respect to Section 73(2)(c) , the company must deposit at least 20% of all the deposits that are going to mature during that financial year.

The deposit must be made with a scheduled bank, ensuring that the funds are kept in a safe and regulated banking institution.

The money placed in this bank deposit is strictly earmarked for repayment of deposits.

The company is not permitted to use this money for any other business activity, investment, or expenditure.

At all times during the financial year, the balance kept in this bank account must not fall below 20% of the total deposits that are due to mature during that year.

(3).

The register in 14(1) must be kept safely and in good condition.

It must be preserved for at least eight years.

This eight-year period is counted from the financial year in which the most recent entry was made in the register.

Rule 15. General provisions regarding premature repayment of deposits.

• A depositor may request the company to repay the deposit early, but only after the deposit has completed at least six months from the date it was made.

This early repayment happens before the original maturity period for which the deposit was accepted.

In such a case, the company must reduce the interest rate by 1% from the rate that would normally apply for the actual period the deposit.

The company is not allowed to pay interest at any rate higher than this reduced rate.

The rule about reducing interest for early repayment does not apply if the company repays the deposit early only for the following purposes:

(a). To comply with the requirements of rule 3.

(b). To provide war risk or other related benefits to personnel of the Navy, Army, or Air Force, or to their families, based on an application made by an association or society formed by such personnel, during a period of emergency declared under article 352 of the Constitution.

Eligible company under Section 73(2) may allow a depositor to renew a deposit before it matures so that the depositor can get a higher rate of interest.

If the company permits this early renewal, then the company must pay the depositor the higher interest rate.

This higher rate is allowed only if the renewed deposit follows all other rules and requirements of the deposit regulations.

Additionally, the new (renewed) deposit period must be longer than the time that was left on the old deposit before renewal.

Explanation:

When a company repays a deposit before maturity, it must calculate how long the deposit actually remained with the company.

To calculate this period, each full year is counted normally.

If there is an extra part of a year, the treatment depends on its length:

If the extra period is less than 6 months, it is ignored.

If the extra period is 6 months or more, it is counted as one full year.

This calculation method determines which interest rate the company should apply when making an early repayment.

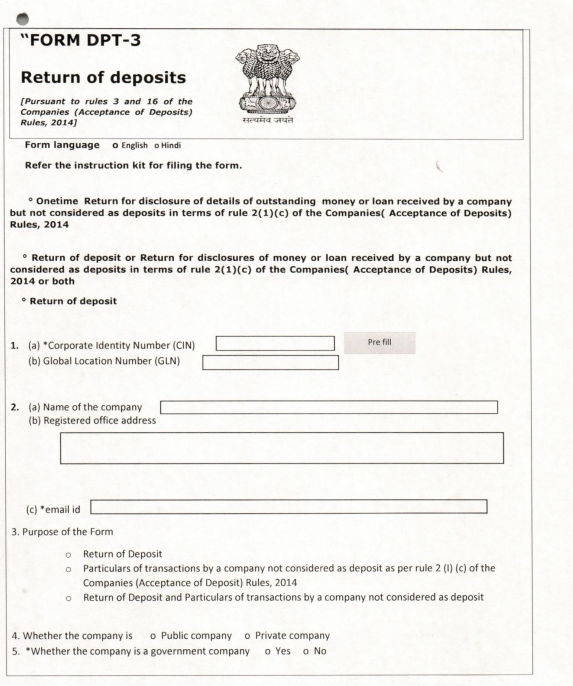

Rule 16. Return of deposits to be filed with the Registrar.

Every company to which the deposit rules apply must file an annual return.

This return must be filed on or before 30th June every year.

The return must be filed with the Registrar in Form DPT-3.

The required filing fee must be paid as per the Companies (Registration Offices and Fees) Rules, 2014.

The information in Form DPT-3 must reflect the company’s position as on 31st March of that year.

The information submitted must be audited by the company’s auditor.

A declaration from the auditor confirming the audit must also be included in Form DPT-3.

Explanation:

Every company except a Government company must use Form DPT-3 for annual filing.

Form DPT-3 must be used to file the return of deposits.

It must also be used to file details of transactions that are not treated as deposits under the rules.

If a company has both deposits and non-deposit transactions, it must report both in the same Form DPT-3.

To Access Form DPT-3: https://ca2013.com/wp-content/uploads/2019/01/form-dpt-3.pdf

16A. Disclosures in the financial statement

(1).

This rule applies to all companies except private companies.

Such companies must give a disclosure in their financial statements.

The disclosure must be made in the notes to the financial statements.

The note must clearly state the details of any money received from a director.

(2).

This rule applies to private companies.

A private company must include a disclosure in its financial statements.

The disclosure must be made in the notes to the financial statements.

The note must state details of money received from directors.

It must also state details of money received from relatives of directors.

(3).

This rule applies to all companies except Government companies.

Such companies must file a one-time return in Form DPT-3.

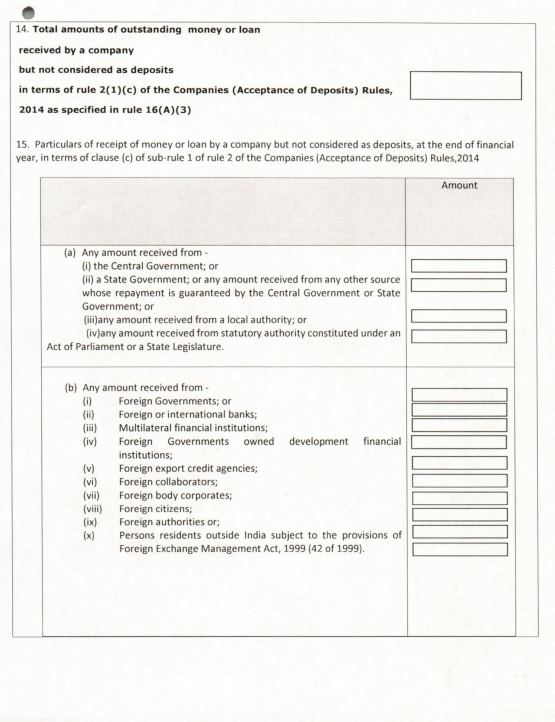

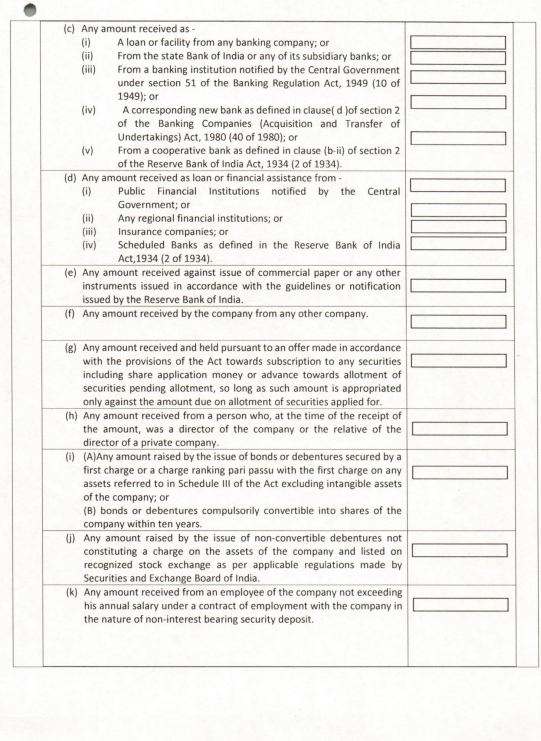

The return must report all outstanding receipts of money or loans that:

Were received between 1st April 2014 and 31st March 2019, and are not treated as deposits under rule 2(1)(c).

This one-time return must be filed within ninety days from:

31st March 2019, or ninety days from the date of publication of the notification in the Official Gazette, whichever wording applies as per the final notification.

The filing must be done along with the prescribed fee under the Companies (Registration Offices and Fees) Rules, 2014.

Rule 17. Penal rate of interest.

This rule applies to all companies.

If a deposit (secured or unsecured) has matured and the depositor has claimed the amount, the company must repay it.

If the company does not repay the claimed deposit after maturity, the amount becomes overdue.

For the entire overdue period, the company must pay a penal interest rate of 18% per annum.

This penalty applies until the company actually pays the overdue deposit amount.

Rule 18. Power of Central Government to decide certain questions.

Sometimes it may not be clear whether these deposit rules apply to a particular company.

If such a question or doubt arises, it must be referred to the Central Government.

The Central Government will make the decision on whether the rules apply.

While making this decision, the Central Government will consult the Reserve Bank of India (RBI).

Rule 19. Applicability of sections 73 and 74 to eligible companies.

Section 76(2) deals with eligible companies that are allowed to accept deposits from the public.

For such companies, the rules and requirements contained in sections 73 and 74 of the Companies Act will also apply mutatis mutandis.

Explanation:

This clarification applies to companies that had accepted or invited public deposits under the Companies Act, 1956 and its rules.

Such deposits are referred to as Earlier Deposits.

If the company has been regularly repaying these Earlier Deposits and the interest due on them in accordance with the old (1956 Act) provisions, then:

The requirement under section 74(1)(b) of the Companies Act, 2013 will be considered fulfilled.

Section 74(1)(b) requires companies to repay old deposits within a specified time

This deemed compliance applies as long as the company:

Follows the provisions of the Companies Act, 2013 and these rules.

Continues to repay the Earlier Deposits and interest on their original due dates.

The repayment must be done in accordance to the original terms, conditions, and duration of those Earlier Deposits.

Any new deposits that an eligible company accepts must fully comply with:

Chapter V of the Companies Act, 2013, and these Deposit Rules.

Rule 20. Statement regarding deposits existing as on the date of commencement of the Act.

For the purposes of clause (a) of 74(1) , the statement shall be in Form DPT-4.

Rule 21. Punishment for contravention

This rule applies to:

Companies covered under Section 73(2). (Companies that can accept deposits from members.)

Eligible companies inviting deposits from the public.

Any other person involved in violating these rules.

If any of these parties contravene any provision of the deposit rules for which the Companies Act does not provide a specific punishment, then:

This penalty clause applies.

The company and every officer in default will be liable for punishment.

The punishment is:

A fine up to ₹5,000.

If the violation continues after the first day, an additional fine up to ₹500 per day for each day the contravention continues.