Open Offer Process

Understanding Public Announcement

The public announcement is essentially an open offer announcement to the shareholders of the target company.

It informs the public that the acquirer has acquired or plans to acquire shares, voting rights, or control.

It must:

Disclose the identity of the acquirer and persons acting in concert.

Explain how the acquisition is happening (in this case, indirectly through another company).

State the extent of shares or voting rights being acquired or likely to be acquired.

Disclose the trigger for the open offer (i.e., crossing thresholds or gaining control).

Include details of the target company whose shares are affected.

Announce the open offer to public shareholders to buy their shares.

The offer price or how it will be determined.

Provide the number/percentage of shares the acquirer is offering to purchase.

Disclose future intentions regarding the target company (like control, management, etc.).

Details of the indirect acquisition transaction (e.g., acquiring a holding company).

Regulation 12. Manager to the Open Offer

12(1).

Before making a public announcement of an open offer, the acquirer is required to take certain preparatory steps.

The acquirer must appoint a merchant banker to handle the open offer process.

The merchant banker so appointed must be registered with SEBI.

The merchant banker must be independent and should not be an associate of the acquirer.

Once appointed, the merchant banker acts as the manager to the open offer and oversees its compliance and execution.

Explanation:

For the purpose of this regulation, the term “associate” needs to be understood clearly.

Instead of defining it separately here, the regulation adopts an existing definition.

The meaning of “associate” is the same as provided under the Securities and Exchange Board of India (Merchant Bankers) Regulations, 1992.

FIND THE DEF and ATTACH HERE.

12(2).

Once the merchant banker is appointed as the manager to the open offer, the process moves forward.

The public announcement of the open offer must be made as required under the regulations.

The acquirer does not make this announcement directly on their own.

Instead, the announcement is made through the manager to the open offer (i.e., the merchant banker).

Thus, the manager to the open offer acts as the intermediary for making the public announcement.

Regulation 13. Timing

13(1).

Where an obligation to make a public announcement arises under regulation 3 or regulation 4, the acquirer must:

Make an announcement and it must be made strictly in accordance with the procedure prescribed under regulation 14 and regulation 15.

The regulations fix a specific trigger point for timing of such announcement.

The public announcement must be made on the date on which the acquirer agrees to acquire shares, voting rights, or control over the target company.

13(2).

Such a Public Announcement:

(a).

In the case of market purchases, a specific timing requirement is prescribed.

The obligation to make a public announcement arises before executing the trade.

The relevant step is placing a purchase order with the stock broker.

Before placing such an order, the acquirer must first make the public announcement.

This requirement applies where the proposed acquisition would increase voting rights.

Specifically, where such increase would cross the stipulated thresholds.

Therefore, the announcement must come before any step that triggers the threshold breach.

Example :

Suppose an acquirer already holds 24% shares in a target company.

The threshold under the regulations is 25%.

The acquirer plans to buy shares from the market that will take his holding to 26%.

Before placing the purchase order with the broker, the acquirer must make the public announcement.

If he places the order first and then announces, it would be a violation.

(b).

Under circumstances where shares or voting rights are acquired through conversion mechanisms then:

In such cases, the conversion may be of convertible securities without a fixed date of conversion.

It may also involve conversion of depository receipts into underlying shares of the target company.

The acquisition effectively takes place when the option to convert is exercised.

At that point, the acquirer obtains shares, voting rights, or control.

The timing of the public announcement is tied to this act of conversion.

The announcement must be made on the same day as the exercise of the conversion option.

Thus, the obligation arises simultaneously with the decision to convert such securities into shares.

Example:

Suppose an acquirer holds convertible debentures of a target company.

These debentures do not have a fixed conversion date.

The acquirer decides to convert them into equity shares today.

Upon conversion, his shareholding increases from 20% to 28%, crossing the 25% threshold.

On the same day he exercises the option to convert, he must make the public announcement.

If he delays the announcement to a later date, it would be non-compliant.

(c).

Under circumstances where acquisition happens through conversion of convertible securities with a fixed conversion date, then:

In such cases, the date of conversion is predetermined in advance.

The acquisition of shares, voting rights, or control will occur on that scheduled date.

Since the event is pre-fixed, the regulations require prior disclosure.

The public announcement cannot be made on or after conversion.

Instead, it must be made in advance of the conversion date.

Specifically, it must be made on the second working day preceding the scheduled date of conversion.

(d).

Under circumstances where acquisition arises pursuant to a disinvestment, a specific timing rule is prescribed.

In such cases, the acquisition is linked to a disinvestment transaction.

The trigger point is the execution of the agreement for such acquisition.

This agreement relates to acquiring shares, voting rights, or control over the target company.

The timing of the public announcement is directly tied to this event.

The announcement must be made on the same day as the execution of the agreement.

There is no scope for delay beyond that date.

Example:

A disinvestment transaction is where a government or existing promoter sells its stake in a company to another party.

For instance, the Government of India decides to sell its 30% stake in a PSU to a private acquirer.

The acquirer agrees to purchase this stake, which will give him control over the target company.

The parties sign a share purchase agreement on 1st September.

On the very same day (1st September), the acquirer must make the public announcement.

If the announcement is made later, it would not comply with the regulation.

(e).

In the case of indirect acquisition of shares, voting rights, or control over a target company, a specific timing flexibility is provided:

This rule applies where none of the parameters under regulation 5(2) are met.

In such situations, the public announcement is not required immediately on the same day.

Instead, a time window is allowed to the acquirer.

The announcement may be made within four working days.

The starting point for this timeline is determined by two possible events.

The first is the date on which the primary acquisition is contracted.

The second is the date on which the intention or decision to make the primary acquisition is publicly announced.

The earlier of these two dates will be taken as the reference point.

The four working day period is counted from that earlier date.

Thus, the obligation arises within a limited window, based on whichever event occurs first.

Example:

Suppose an acquirer plans to acquire a foreign holding company.

This holding company, in turn, owns shares in an Indian listed target company.

By acquiring the foreign company, the acquirer indirectly acquires control over the Indian target company.

The agreement to acquire the foreign company is signed on 1st June.

The deal is publicly announced in the media on 3rd June.

Here, the earlier date is 1st June (date of agreement).

The acquirer gets up to four working days from 1st June to make the public announcement.

So, the announcement must be made by, say, 5th or 6th June (depending on working days).

If the acquirer delays beyond this period, it would be non-compliant.

(f).

In the case of indirect acquisition of shares, voting rights, or control over the target company, a specific rule applies where regulation 5(2) parameters are met.

In such cases, stricter timing is prescribed for the public announcement.

The timing is linked to two key events relating to the primary acquisition.

The first is the date on which the primary acquisition is contracted.

The second is the date on which the intention or decision to make the primary acquisition is announced in the public domain.

The earlier of these two dates is taken as the trigger point.

The public announcement must be made on that earlier date itself.

Thus, the obligation arises immediately upon the first occurrence of either of these events.

Example:

Suppose an acquirer plans to acquire a global holding company.

This holding company has a significant stake in an Indian listed target company.

Because the value or control of the Indian company is substantial (Regulation 5(2) parameters are met), stricter rules apply.

The acquirer signs the agreement to acquire the global holding company on 10th August.

However, news of the deal is publicly announced earlier on 8th August.

Here, the earlier date is 8th August (public announcement of intention).

The acquirer must make the open offer public announcement on 8th August itself.

Even though the agreement is signed later, the earlier public disclosure triggers the obligation.

If the acquirer waits until 10th August, it would be a violation.

(g).

Under circumstances where acquisition happens through a preferential issue, a specific timing rule is prescribed.

In such cases, the acquirer obtains shares, voting rights, or control via preferential allotment.

The trigger point is not the allotment itself, but the approval stage.

The relevant event is when the board of directors of the target company authorises the preferential issue.

The timing of the public announcement is directly linked to this authorization.

The announcement must be made on the same date as the board approval.

There is no delay permitted beyond this point.

Thus, the obligation arises at the stage of board authorization of the preferential issue.

Example:

Suppose a target company plans to issue shares to an acquirer through a preferential allotment.

The acquirer currently holds 20% shares.

After the preferential issue, his holding will increase to 30%, crossing the 25% threshold.

The board of directors of the target company approves this preferential issue on 5th March.

Even though the actual allotment of shares may happen later, the trigger is the board approval.

On the same day (5th March), the acquirer must make the public announcement.

If the acquirer waits until the shares are actually allotted, it would be non-compliant.

(h).

Under circumstances where voting rights increase due to a buy-back, then this rule applies.

This applies where such buy-back does not qualify for exemption under regulation 10.

In such cases, the acquirer’s percentage holding increases without any direct acquisition.

The trigger is the consequential increase in voting rights.

The timing of the public announcement is not immediate.

Instead, a longer time window is provided.

The reference point is the closure of the buy-back offer by the target company.

The public announcement must be made within this timeline.

Specifically, it must be made not later than the ninetieth day from the date of such closure.

So , the obligation arises post buy-back, within the prescribed 90-day period.

Example:

Suppose an acquirer holds 24% shares in a target company.

The company undertakes a buy-back and reduces its total share capital.

The acquirer does not participate in the buy-back.

After the buy-back, his holding automatically increases to 27%.

This crosses the 25% threshold, even though he did not buy any shares.

The buy-back closes on 1st April.

The acquirer is not required to make an immediate announcement on that day.

Instead, he gets time up to 90 days from 1st April.

So, the public announcement must be made on or before 30th June.

If he fails to do so within this period, it would be non-compliant.

(i).

Under circumstances where acquisition of shares, voting rights, or control occurs on a date beyond the acquirer’s control, a specific rule applies.

In such cases, the acquirer does not know or control the exact date of acquisition.

The trigger is not the acquisition itself, but the intimation of such acquisition.

The acquirer becomes aware only upon receiving such intimation.

The timing of the public announcement is linked to this awareness.

The public announcement must be made within two working days.

The period is counted from the date of receipt of intimation of having acquired title.

So, the obligation arises upon intimation, within a short prescribed timeline.

Example:

Suppose an acquirer is entitled to receive shares through inheritance or operation of law.

The actual transfer of shares happens automatically on 10th May, without his active involvement.

However, the acquirer is not immediately informed about this transfer.

He receives official intimation of the transfer on 15th May.

The trigger for compliance is not 10th May, but 15th May (date of intimation).

From 15th May, the acquirer gets two working days to make the public announcement.

So, the announcement must be made by 17th May (assuming working days).

If he delays beyond this, it would be non-compliant.

13(2A).

Notwithstanding anything contained in 12(2), a special rule is prescribed for certain combined acquisitions.

This applies where the proposed acquisition is through a combination of multiple modes.

In such cases:

(i). The acquisition may involve an agreement along with one or more modes specified under regulation 13(2).

(ii). Alternatively, it may involve only one or more modes specified under regulation 13(2)(a) to (i).

Where such combination of acquisition modes exists, a unified timing rule applies.

The public announcement is not required separately for each mode.

Instead, it must be made on the date of the first such acquisition.

This first acquisition acts as the trigger point for the announcement.

However, an additional disclosure obligation is imposed.

The acquirer must disclose details of the proposed subsequent acquisitions in the public announcement.

Thus, a single announcement at the initial stage covers the entire composite acquisition plan.

Example:

Sometimes, an acquirer does not buy shares in just one way, but uses a mix of different methods.

For example, he may sign an agreement first and then also buy shares through market purchases or other permitted modes.

Instead of treating each step separately, the law treats the whole plan as one combined transaction.

In such cases, the acquirer does not need to make multiple public announcements.

He is required to make only one public announcement.

The timing of this announcement is fixed at the very first step of acquisition.

So, the moment the first acquisition happens, the announcement must be made.

Even if more acquisitions are planned later, they are covered by this first announcement.

However, there is an important condition.

The acquirer must clearly disclose all the future planned acquisitions in that first announcement.

13(3).

Under circumstances where the acquirer chooses to make a voluntary open offer under regulation 6, then the following rule applies:

In such cases, the open offer is not triggered by thresholds, but by the acquirer’s own decision.

The key event is the decision taken by the acquirer to make the open offer.

The timing of the public announcement is directly linked to this decision.

The announcement must be made on the same day as the decision.

There is no gap permitted between decision and announcement.

Thus, the obligation arises immediately upon deciding to voluntarily make an open offer.

Example:

Under circumstances where the acquirer voluntarily decides to make an open offer, the trigger is the decision itself.

Suppose an acquirer already holds 28% shares in a target company.

He is not required by law to make an open offer at this stage.

However, he decides to voluntarily acquire more shares to increase his stake.

He takes this decision on 10th January.

On the same day (10th January), he must make the public announcement of the open offer.

Even if the actual purchase of shares happens later, the trigger is the decision date.

If he delays the announcement to a later date, it would be non-compliant.

13(4).

After making the public announcement under 13(1) or 13(3), the following steps are required to be followed:

The acquirer is required to issue a more detailed disclosure.

This is called the detailed public statement (DPS).

The DPS is not issued directly by the acquirer.

It is published through the manager to the open offer.

The DPS must comply with the procedure under regulation 14 and regulation 15.

The timing for this is specifically prescribed.

It must be published within five working days of the public announcement.

Under circumstances where the public announcement is made under clause 13(2)(e) , then a special rule applies for the detailed public statement (DPS).

This typically relates to indirect acquisitions.

In such cases, the DPS is not linked to the date of the public announcement.

Instead, the timing is linked to the completion of the primary acquisition.

The primary acquisition refers to acquiring shares, voting rights, or control in another company or entity.

That entity, in turn, holds shares or control over the target company.

The DPS must be made after this primary acquisition is completed.

The timeline is specifically prescribed.

It must be published within five working days of such completion.

Explanation:

Under circumstances where an acquirer attempts an acquisition but does not ultimately gain control or voting rights, then:

In such cases, the acquisition may not materialise as intended.

The acquirer may fail to obtain the ability to exercise voting rights.

Or may fail to obtain control over the target company.

Since control or voting rights are not actually acquired, the trigger for the open offer does not fully materialise.

Consequently, the next compliance step is relaxed.

The acquirer is not required to make a detailed public statement (DPS).

This means the open offer process does not proceed further.

Example:

(a). Detailed Public Statement within 5 days of Public Announcement

Suppose an acquirer signs an agreement on 1st June to acquire 30% shares of a target company.

This triggers an open offer, so he makes a public announcement (PA) on 1st June.

Now, the law requires a more detailed disclosure (DPS).

The acquirer must publish the DPS within 5 working days from 1st June (say by 6th or 7th June).

Here, DPS timing is directly linked to the PA date.

(b). Indirect Acquisition - Detailed Public Statement after completion of primary acqusition.

Suppose an acquirer plans to acquire a foreign holding company that owns shares in an Indian listed target company.

He makes a public announcement (PA) on 1st July when the deal is announced.

However, the actual acquisition of the foreign company (primary acquisition) completes on 20th July.

In this case, DPS is not required within 5 days of 1st July.

Instead, the DPS must be made within 5 working days from 20th July (i.e., after completion of primary acquisition).

So, DPS may be made by around 25th July.

(c). Failure of Acquisition - No Detailed Public Statement Required

Suppose the same acquirer announces on 1st July that he will acquire the foreign holding company.

However, due to regulatory issues, the deal fails and is never completed.

As a result, the acquirer never gains control or voting rights in the target company.

Since the acquisition did not materialise, the open offer effectively collapses.

In this case, the acquirer is not required to issue a DPS at all.

Regulation 14. Publication

14(1).

Under circumstances where a public announcement is made, a dissemination requirement follows.

A Dissemination requirement is a duty to ensure information reaches the public, shareholders, and regulators properly and transparently

The acquirer must send the public announcement to all stock exchanges where the target company is listed.

The objective is to make sure that all relevant trading platforms are informed.

The responsibility then shifts to the stock exchanges.

Upon receiving the announcement, the stock exchanges must act promptly.

They are required to disseminate the information to the public.

This dissemination must be done forthwith, i.e., without delay.

14(2).

Under circumstances where a public announcement is made, a follow-up communication requirement arises.

The acquirer must send a copy of the public announcement to the Securities and Exchange Board of India.

The acquirer must also send a copy to the target company.

This must be sent to the registered office of the target company.

The timing for this step is specifically prescribed.

It must be completed within one working day from the date of the public announcement.

14(3).

Under circumstances where a detailed public statement (DPS) is to be published, a specific publication requirement is prescribed.

In such cases, the DPS must be widely disseminated through newspapers.

The publication must be made in multiple languages and regions.

It must be published in one English national daily with wide circulation.

It must also be published in one Hindi national daily with wide circulation.

Additionally, it must be published in one regional language daily where the registered office of the target company is situated.

Further, it must be published in one regional language daily at the place of the stock exchange.

This stock exchange should be the one where the maximum trading volume in the target company’s shares is recorded.

The relevant trading volume is calculated over the 60 trading days preceding the public announcement.

14(4).

Under circumstances where the detailed public statement (DPS) is published in newspapers, certain simultaneous obligations arise.

At the same time as publication, copies of the DPS must be sent to specified entities.

(i). To the Securities and Exchange Board of India through the manager to the open offer

The DPS must be sent to SEBI.

This is not done directly by the acquirer.

It is routed through the manager to the open offer (merchant banker).

SEBI reviews the DPS to ensure all disclosures and requirements are met.

(ii) To all stock exchanges where the target company is listed

The DPS must be sent to every stock exchange where the company’s shares are traded.

Once received, the stock exchanges have an immediate duty.

They must forthwith disseminate the information to the public.

(iii) To the target company at its registered office

A copy of the DPS must also be sent to the target company.

It must be delivered to the company’s registered office.

Upon receiving it, the target company has its own obligation.

The company must forthwith circulate the DPS to all members of its board of directors.

Regulation 15. Contents

15(1).

The public announcement should essentially containing all such information as may be specified.

It must also include the following:

(a).

Name and identity of the acquirer and persons acting in concert with him

(b).

Name and Identity of the Sellers

(c).

Under circumstances where a public announcement or detailed disclosure is made, the nature of the acquisition must be clearly stated.

The acquirer must explain how the acquisition is proposed to take place.

This includes whether the acquisition is through purchase of existing shares.

It may also be through allotment of new shares (such as preferential issue).

The acquisition may happen through any other permitted mode.

It could involve acquiring voting rights or control over the target company.

The disclosure must clearly specify the exact method being used.

(d).

Under circumstances where an open offer is triggered, details of consideration must be disclosed.

The acquirer must state the consideration for the proposed acquisition.

This refers to what the acquirer is paying (cash, shares, or other form of payment).

The disclosure must relate to the transaction that triggered the open offer obligation.

It must clearly explain the value being paid for such acquisition.

Additionally, the price per share must be disclosed, if applicable.

This helps shareholders understand the valuation of the transaction.

It also enables comparison with the open offer price.

(e).

The Offer Price and the mode of payment of consideration.

(f).

Under circumstances where details of the open offer are disclosed, certain key elements must be specified.

The acquirer must disclose the offer size.

This refers to the number or percentage of shares proposed to be acquired from public shareholders.

The acquirer must also disclose any conditions attached to the offer.

This includes conditions like a minimum level of acceptances, if applicable.

It means the offer may be conditional upon receiving a minimum number of shares.

Further, the acquirer must clearly state their intention regarding listing status.

This includes whether they plan to delist the target company or continue its listing.

If the acquirer intends to delist under regulation 5A, additional disclosures are required.

The proposed open offer price must be disclosed.

An indicative price must also be provided.

The acquirer must explain the rationale and basis for arriving at the indicative price.

Understanding Indicative Price:

An indicative price is a provisional or initial price disclosed by the acquirer.

It is shared at an early stage, especially in cases like proposed delisting.

It gives shareholders an idea of the likely price at which shares may be acquired.

It is not always the final price.

The final price may change based on regulatory requirements or price discovery mechanisms.

15(2).

Under circumstances where a detailed public statement (DPS) is issued, its content has a specific purpose.

The DPS must include all material and relevant information.

The information to be included is as specified under the applicable regulations.

The focus is on providing complete and accurate disclosures.

This includes details about the acquirer, the offer, pricing, and future plans.

The aim is not just compliance, but meaningful disclosure.

The DPS should give shareholders a clear understanding of the open offer.

It should help them evaluate the impact on their investment.

Based on this information, shareholders can decide whether to tender their shares or not.

15(3).

Under circumstances where any communication is made in relation to an open offer, a strict disclosure standard applies.

This covers the public announcement, detailed public statement, and all related materials.

It also includes advertisements, circulars, brochures, publicity material, and the letter of offer.

All such communications must be complete and accurate.

They must not omit any material or relevant information.

They must not contain any misleading statements or representations.

The obligation applies to all forms of communication issued in the acquisition process.

Regulation 16. Filing of Offer with the Board

16(1).

Under circumstances where the detailed public statement (DPS) has been made, the next compliance step follows.

The acquirer is required to prepare a draft letter of offer (DLOF).

This draft must contain all prescribed and relevant information.

The filing must be done through the manager to the open offer.

It is not filed directly by the acquirer.

The draft letter of offer must be filed with the Securities and Exchange Board of India.

The timing for this filing is specifically prescribed.

It must be done within five working days from the date of the DPS.

Along with the draft, a non-refundable fee must be paid.

The amount of the fee depends on the prescribed scale.

The mode of payment is also specified.

It can be made through direct credit via NEFT / RTGS / IMPS.

It can also be made through the SEBI online payment gateway.

Any other mode specified by SEBI from time to time is also permitted.

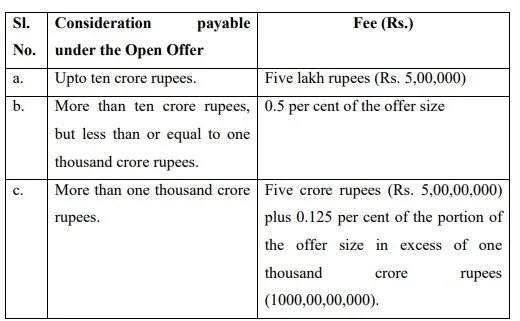

The non-refundable fee payable to SEBI depends on the offer size (consideration under the open offer).

(a) Where consideration is up to ₹10 crore:

A fixed fee is payable.

The amount is ₹5 lakh.

(b). Where consideration is more than ₹10 crore but ≤ ₹1,000 crore:

The fee is 0.5% of the offer size.

It is calculated on the entire consideration amount.

(c) Where consideration exceeds ₹1,000 crore:

A base fee of ₹5 crore is payable.

In addition, 0.125% is charged on the portion exceeding ₹1,000 crore.

So, fee = ₹5 crore + (0.125% of amount above ₹1,000 crore).

16(2).

Under circumstances where consideration under the open offer is to be calculated, a specific method is prescribed.

The calculation must be based on the offer price.

It must assume full acceptance of the open offer.

This means calculation is done as if all shareholders tender their shares.

The total consideration is therefore computed on the maximum possible payout.

In cases where differential pricing applies, an additional rule is given.

The calculation must be done using the highest offer price.

This applies even if different shareholders are offered different prices.

The mode of payment is irrelevant for this calculation.

Whether consideration is paid in cash, shares, or any other form does not matter.

Under circumstances where the consideration under the open offer is increased, a corresponding adjustment is required.

This increase may happen due to a revision in offer price.

It may also happen due to a revision in offer size.

In such cases, the total consideration payable under the open offer increases.

As a result, the fees payable to SEBI must also be revised.

The revised fee must be recalculated based on the updated consideration.

The timing for payment of the revised fee is specifically prescribed.

It must be paid within five working days from the date of such revision.

Example:

Under circumstances where consideration is calculated and later revised:

Initial Calculation

Suppose an acquirer makes an open offer to buy 1,00,000 shares.

The offer price is ₹100 per share.

Even if not all shareholders may sell, the law assumes full acceptance.

So, total consideration = 1,00,000 × 100 = ₹1 crore.

This ₹1 crore is used to calculate the SEBI fee.

Differential Pricing case

Suppose some shareholders are offered ₹100 per share and others ₹120 per share.

Even if only a few get ₹120, the law uses the highest price (₹120).

So, total consideration = 1,00,000 × 120 = ₹1.2 crore.

Fee is calculated on ₹1.2 crore (not ₹100).

Revision in Offer Price

Later, the acquirer revises the offer price from ₹100 to ₹130.

New total consideration = 1,00,000 × 130 = ₹1.3 crore.

Since consideration increased, SEBI fee must also be revised upward.

The additional fee must be paid within 5 working days from the revision date.

Revision in Offer Size

Suppose instead of 1,00,000 shares, the acquirer increases the offer to 1,50,000 shares.

At ₹100 per share ,for the new size of 1,50,000 a new consideration would be applicable at = ₹1.5 crore.

Again, fees must be recalculated on ₹1.5 crore.

The revised fee must be paid within 5 working days.

Under circumstances where the open offer value increases, a follow-up obligation arises.

The increase may be due to a revision in offer price.

It may also be due to a revision in offer size.

As a result, the total consideration payable under the open offer increases.

Consequently, the fees payable to SEBI must also be revised.

The revised fee must be recalculated based on the updated (higher) consideration.

The timing for payment is specifically prescribed.

The revised fee must be paid within five working days.

The timeline starts from the date of such revision.

Example:

Revision in Offer Price

Suppose an acquirer makes an open offer for 1,00,000 shares at ₹100 per share.

Total consideration would be ₹1 crore.

SEBI fee is calculated on this amount.

Later, the acquirer revises the offer price to ₹120 per share.

New consideration = 1,00,000 × 120 = ₹1.2 crore.

Since the consideration has increased, the SEBI fee must be recalculated on ₹1.2 crore.

The additional fee (difference) must be paid.

This payment must be made within 5 working days from the date of revision.

Revision in Offer Size

Suppose initially the offer is for 1,00,000 shares at ₹100 then SE ₹1 crore.

Later, the acquirer increases the offer size to 1,50,000 shares.

New consideration = 1,50,000 × 100 = ₹1.5 crore.

The SEBI fee must now be recalculated on ₹1.5 crore.

The extra fee must be paid within 5 working days from the date the size was increased.

16(3).

Under circumstances where key documents of the open offer are prepared, a digital submission requirement applies.

The responsibility lies with the manager to the open offer (merchant banker).

The manager must provide soft copies of specified documents.

These documents include:

The public announcement (PA).

The detailed public statement (DPS).

The draft letter of offer (DLOF).

The soft copies must be submitted in the format and specifications prescribed by the Securities and Exchange Board of India.

Once submitted, SEBI has a further obligation.

SEBI will upload these documents on its official website.

16(4).

Under circumstances where the draft letter of offer (DLOF) is filed, a review process by SEBI will follow:

SEBI is required to examine the draft letter of offer.

It must provide its comments as quickly as possible.

However, an outer time limit is prescribed.

SEBI must give its comments within 15 working days from the date of receipt of the draft.

If SEBI provides comments within this period, the acquirer must consider and incorporate them.

If SEBI does not provide any comments within 15 working days, a legal presumption applies.

It is deemed that SEBI has no comments to offer.

Example:

SEBI gives comments within 15 days

Suppose the acquirer files the DLOF with the Securities and Exchange Board of India on 1st June.

SEBI reviews the document and sends comments on 10th June.

These comments may relate to disclosures, pricing, or corrections.

The acquirer and manager must incorporate these changes.

Only after making these changes can the final letter of offer be sent to shareholders.

No comments within 15 days

Suppose the DLOF is filed on 1st June.

SEBI does not send any comments till 21st June (15 working days).

In this case, it is deemed that SEBI has no comments.

The acquirer can proceed without waiting further.

The letter of offer can be finalized and sent to shareholders.

Under circumstances where the Securities and Exchange Board of India seeks further information, a modified timeline applies.

SEBI may ask for clarifications or additional information from the manager to the open offer.

In such cases, the original 15 working day timeline does not strictly continue.

The timeline gets extended based on the response.

The extension depends on when a satisfactory reply is received.

Once the manager submits the required clarification or information, and it is satisfactory, a new clock starts.

SEBI must then issue its comments within 5 working days from the date of receipt of such satisfactory reply.

Example:

Suppose the acquirer files the DLOF with the Securities and Exchange Board of India on 1st June.

Normally, SEBI would have to give comments within 15 working days.

On 8th June, SEBI asks for clarification on pricing and disclosures.

The manager to the open offer submits a reply on 12th June.

However, SEBI finds the reply incomplete and asks again.

A satisfactory reply is finally submitted on 15th June.

Now, the original 15-day clock is no longer relevant.

A fresh timeline starts from 15th June.

SEBI must now give its comments within 5 working days from 15th June (say by 20th June).

Under circumstances where the Securities and Exchange Board of India gives its comments on the draft letter of offer, further compliance is required.

SEBI may specify certain changes or modifications to the draft.

These changes are mandatory and not optional.

The responsibility lies with both:

The manager to the open offer, and

The acquirer.

They must incorporate all such changes in the letter of offer.

This must be done before the letter of offer is sent to shareholders.

Example:

Suppose the acquirer files a draft letter of offer (DLOF) with the Securities and Exchange Board of India on 1st July.

SEBI reviews the draft and on 10th July gives comments:

The offer price calculation is not properly explained.

Certain financial disclosures are incomplete.

The future plans of the acquirer are not clearly stated.

These are not suggestions and they are mandatory changes.

The manager to the open offer and the acquirer must:

Revise the pricing explanation.

Add complete financial disclosures.

Clearly state future plans.

They update the draft accordingly and prepare the final letter of offer.

Only after incorporating all these changes can they send the letter of offer to shareholders.

If they ignore or partially follow SEBI’s comments, it would be non-compliant.

16(5).

Under circumstances where there are competing offers for the same target company, then:

Multiple acquirers may make open offers for the same company.

In such cases, each acquirer files a draft letter of offer (DLOF).

The Securities and Exchange Board of India must review all such drafts.

SEBI is required to ensure fair and equal treatment among competing offers.

Therefore, SEBI must provide its comments on all DLOFs on the same day.

It cannot give comments on one offer earlier and delay others.

This ensures a level playing field for all acquirers.

It also allows shareholders to compare competing offers simultaneously.

16(6).

Under circumstances where the disclosures in the draft letter of offer are found to be inadequate, a corrective step is triggered.

The Securities and Exchange Board of India may require improvements in the document.

SEBI can call for a revised letter of offer.

This means the original draft is not sufficient for regulatory purposes.

The acquirer and manager must prepare and submit a revised draft with proper and complete disclosures.

Once the revised letter of offer is submitted, it is not treated casually.

SEBI will review it again.

The review will follow the same process as earlier.

It will be dealt with in accordance with 16(4).