Open Offer Process - Part II

Understanding Escrow Account

An escrow account is a temporary account where money or assets are kept with a neutral third party.

It is created to ensure that both parties fulfil their obligations in a transaction.

In the context of an open offer:

The acquirer deposits money into the escrow account.

This acts as a security for payment to shareholders.

The account is usually managed by an independent entity (like a bank or the merchant banker).

The money in the escrow account cannot be freely used by the acquirer.

It can only be used for the specific purpose of the open offer.

If the acquirer completes the offer properly, the money is used to pay shareholders.

If the acquirer fails to comply, the escrow amount can be used to compensate or enforce obligations.

Regulation 17. Provision of Escrow

17(1).

Under circumstances where an open offer is to be made, a security requirement is prescribed.

The acquirer must create an escrow account.

This is to ensure performance of obligations under the regulations.

The timing for creating the escrow account is specifically fixed.

It must be created not later than two working days prior to the date of the detailed public statement (DPS).

The escrow account acts as a financial safeguard.

It ensures that funds are available to pay shareholders.

The acquirer must also deposit a specified amount into the escrow account.

The amount is determined based on a prescribed scale.

This deposit represents a security for completing the open offer.

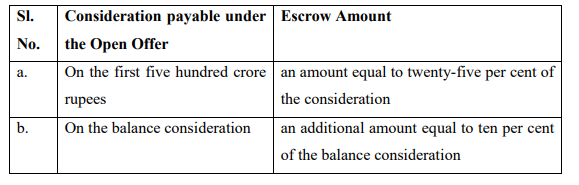

The deposit in the escrow amount will be the following aggregate amount in accordance to the scale below:

The amount to be deposited in the escrow account depends on the total consideration of the open offer.

(a). On the first ₹500 crore of consideration: The acquirer must deposit 25% of this amount in the escrow account.

(b). On the balance consideration (above ₹500 crore): The acquirer must deposit an additional 10% of the remaining amount.

Example:

Total offer size = ₹800 crore

On first ₹500 crore, the deposit will be 25% = ₹125 crore.

On remaining ₹300 crore , the deposit will be 10% = ₹30 crore

Therefore , the total escrow deposit will be = ₹155 crore

Under circumstances where the open offer is conditional upon a minimum level of acceptance, a stricter escrow requirement applies.

In such cases, the acquirer must deposit funds in cash in the escrow account.

The amount to be deposited is determined using two alternatives:

100% of the consideration payable for the minimum level of acceptance, or

50% of the total consideration payable under the open offer.

The acquirer must deposit whichever of the above two amounts is higher.

Example:

Suppose an acquirer makes an open offer of ₹200 crore in total.

The offer is conditional upon receiving at least 40% acceptance from shareholders.

Step 1: Calculate 100% of minimum acceptance amount

Minimum acceptance = 40% of ₹200 crore = ₹80 crore

So, first value = ₹80 crore

Step 2: Calculate 50% of total offer size

50% of ₹200 crore = ₹100 crore

Step 3: Compare both amounts

₹80 crore vs ₹100 crore

Higher amount = ₹100 crore

Final Requirement:

The acquirer must deposit ₹100 crore in cash in the escrow account.

Under circumstances where the open offer arises due to an indirect acquisition, a stricter escrow rule applies.

This applies where the public announcement is made under regulation 13(2)(e).

In such cases, the acquirer must deposit funds in the escrow account.

The requirement is more stringent than normal cases.

The acquirer must deposit 100% of the total consideration payable under the open offer.

This means the entire offer amount must be secured upfront.

There is no partial percentage or slab-based calculation here.

The full amount must be available in escrow.

Example:

Suppose an acquirer purchases a foreign holding company.

This holding company owns 60% shares in an Indian listed target company.

By acquiring the foreign company, the acquirer indirectly gains control over the Indian company.

This triggers an open offer to public shareholders of the Indian company.

Assume the open offer size is ₹300 crore.

Escrow Requirement:

Normally, escrow would be calculated in slabs (25%, 10%, etc.).

But since this is an indirect acquisition under regulation 13(2)(e), the stricter rule applies.

The acquirer must deposit 100% of ₹300 crore in the escrow account.

So , the entire ₹300 crore is locked in escrow upfront.

17(2).

The consideration under the open offer must be calculated as per regulation 16(2).

This calculated consideration forms the basis for determining the escrow amount.

If there is an upward revision in the offer price, or the offer size, then:

The total consideration will increase accordingly.

The escrow amount must then be recomputed based on the revised consideration.

The acquirer must deposit the additional amount required into the escrow account.

This additional amount must be deposited before giving effect to the revision.

Example:

Suppose an acquirer makes an open offer for 1,00,000 shares at ₹100 per share.

Total consideration = ₹1 crore.

Based on this, the acquirer deposits the required escrow amount (as per % rules).

Later, the acquirer revises the offer price to ₹120 per share.

New consideration = 1,00,000 × 120 = ₹1.2 crore.

Since the consideration increased, the escrow amount must be recalculated on ₹1.2 crore.

Suppose earlier escrow required was ₹25 lakh, and now it becomes ₹30 lakh.

The acquirer must deposit the additional ₹5 lakh.

This additional ₹5 lakh must be deposited before announcing or implementing the revised price.

17(3).

The escrow account mentioned in 17(1) can be in any of the following forms:

(a).

Cash deposited with any scheduled commercial bank.

(b).

Bank guarantee issued in favour of the manager to the open offer by any scheduled commercial bank

(c).

The deposit can also be in the form of securities instead of cash.

These securities must be:

Frequently traded, and

Freely transferable.

This ensures that the securities are liquid and easily convertible into cash if required.

Examples may include listed equity shares or other marketable securities.

However, such deposits are not taken at full value.

An appropriate margin is applied.

This means the value of securities is discounted to account for market risk.

The margin ensures that even if prices fluctuate, there is sufficient security in the escrow.

So , securities can be used as escrow, but only if they are liquid, transferable, and adequately margin-adjusted.

If the acquirer deposits securities as escrow (instead of cash) then:

These securities provided should be frequently traded and freely transferable as mentioned in clause (c).

In such cases, not all securities are automatically acceptable.

The securities must meet certain prescribed conditions.

These conditions are laid down in regulation 9(2).

Therefore, the securities used for escrow must conform to those requirements.

In case of a public announcement is made for an indirect acquisition , in accordance with 13(2)(3) then:

Deposits of securities is not allowed in an escrow account for that indirect acquisition.

It probably has to be cash or bank guarantee.

Explanation:

An escrow account mentioned in (a) is created with a cash component

This cash can be kept in an interest-bearing account

So, the money can earn interest while it is held

However, there is a responsibility on the merchant banker

The merchant banker must ensure that the funds are readily available when payment is to be made to shareholders

So, earning interest should not delay or affect payment

17(4).

An acquirer is usually required to create an escrow account.

The escrow can be created using a bank guarantee, or deposit of securities.

However, this is not enough on its own.

The acquirer must also deposit a cash component.

Minimum requirement: At least 1% of the total consideration must be in cash.

This cash must be deposited with a scheduled commercial bank.

The cash component forms part of the same escrow account

So, Even if escrow is mainly non-cash, at least 1% must always be in cash for security and liquidity

17(5).

Part of the escrow account is kept as a cash deposit with a scheduled commercial bank

While opening this account, the acquirer must give authority

This authority is given to the manager to the open offer

The manager is empowered to instruct the bank to:

Issue a banker’s cheque, or

Issue a demand draft, or

Make direct payments from the escrow account

These payments must be made in accordance with the requirements of the regulations.

17(6).

A Part of the escrow account may be created in the form of a bank guarantee.

This bank guarantee must be issued in favour of the manager to the open offer.

The guarantee must remain valid for the entire offer period.

In addition, it must continue to remain valid for 30 days after completion of payment to shareholders.

So, the bank guarantee must stay active during the offer and for 30 extra days after payments, ensuring full security for shareholders.

17(7).

A Part of the escrow account may be in the form of securities

The acquirer must authorize the manager to the open offer

This authorization allows the manager to:

Sell the securities, or otherwise realise their value.

This ensures that funds can be generated when required.

If there is any shortfall in the escrow amount: the manager to the open offer becomes responsible to make good the shortfall.

So , securities in escrow can be liquidated, and the manager must ensure the full required amount is always maintained.

17(8).

After shareholders tender their shares, the payment of consideration is completed.

Even after this, the escrow account is not immediately released.

The manager to the open offer must wait for 30 days.

During this period the escrow account remains intact as a safeguard.

There is only one exception: Funds can be transferred to a special escrow account as required under regulation 21.

Apart from this exception , no release of escrow funds is allowed before 30 days.

So , escrow stays locked for 30 days after payment, ensuring additional protection, except for permitted transfers to a special escrow account.

17(9).

The acquirer has obligations under the regulations.

If the acquirer fails to fulfill these obligations:

The Securities and Exchange Board of India can step in.

SEBI can direct the manager to the open offer to take action.

The manager may be instructed to:

Forfeit the escrow account, or

Forfeit amounts in the special escrow account.

This forfeiture can befull, or partial.

So , if the acquirer defaults, SEBI can order forfeiture of escrow funds as a penalty and safeguard mechanism.

17(10).

The escrow account deposited with the bank in cash will be released only in a particular manner:

The manner is as follows:

(a).

The entire amount is returned to the acquirer if the open offer is withdrawn under regulation 23

This must be certified by the manager to the open offer

Special condition

If withdrawal is under Regulation 23(1)(c) then the manager cannot release funds immediately.

The manager must first receive confirmation from the Securities and Exchange Board of India.

So , escrow money goes back to the acquirer on valid withdrawal, but in certain cases, SEBI approval is required before release.

(b).

The escrow account (cash) can be released in a specific way.

Up to 90% of the escrow amount can be transferred.

This transfer is made to the special escrow account.

It must be done in accordance with regulation 21.

The full amount is not transferred—only up to 90%.

So , majority of escrow funds (max 90%) can be moved to a special escrow account as per the regulations.

(c).

After the open offer process, payments are made to shareholders

A part of the escrow is already transferred to the special escrow account

The remaining balance still lies in the escrow account

This remaining balance is returned to the acquirer

But such return will be only after 30 days have passed from completion of payment to shareholders

This must be certified by the manager to the open offer.

So , leftover escrow funds go back to the acquirer, but only after a 30-day safety period and certification.

(d).

Under circumstances , an open offer is not in cash but in exchange of shares or other secured instruments then:

After shareholders tender their shares consideration is given (in shares/instruments).

A 30-day period must pass after completion of such payment.

(e)

After these 30 days, the entire escrow amount is released to the acquirer.

This requires certification by the manager to the open offer.

So , in share-exchange offers, the full escrow is returned after 30 days and certification, since no cash payout risk remains.

(e).

If under any circumstance the acquirer fails to fulfill obligations under the regulations then:

As a result, the escrow account is forfeited.

Post this , the entire escrow amount is transferred to the manager to the open offer

Before distribution expenses of registered market intermediaries (if any) are deducted

The remaining amount is then distributed as follows:

(i).

1/3rd to the target company.

(ii).

1/3rd to the Investor Protection and Education Fund.

Investor Protection and Education Fund is established under the SEBI (Investor Protection and Education Fund) Regulations, 2009.

(iii)

1/3rd distributed among shareholder on a pro-rata basis (based on their participation in the open offer).

So , on default, escrow is forfeited and split equally between the company, investor fund, and participating shareholders (after expenses).