Introduction to Corporate Restructuring

CORPORATE RESTRUCTURING

Corporate restructuring means making major changes to the way a company is set up or run so that it works better.

It involves reorganising , rearranging or changing:

Ownership: Who owns the company.

Business Activities: How the business operates.

Financial Structure: How money is managed.

Legal Framework: The company’s legal setup.

These changes are made to:

Reduce problems.

Handle risks.

Save costs.

Increase value.

Adapt to changes in the market or the law.

Corporate restructuring can take forms such as mergers, acquisitions, demergers, reduction of capital, buy-backs, or financial reorganisation.

ORGANIC AND INORGANIC GROWTH

A business organisation can grow mainly in two ways: Organic growth and Inorganic growth.

ORGANIC GROWTH:

Organic growth means growing a business from within, using its own efforts.

The company grows by improving its own operations, not by buying or merging with another company.

This growth can be achieved through capital restructuring or business restructuring.

It may involve better management, cost control, or financial adjustments inside the business.

The objective is to attract more customers in order to get higher sales and more income.

The company remains the same legal entity, with no change in its identity.

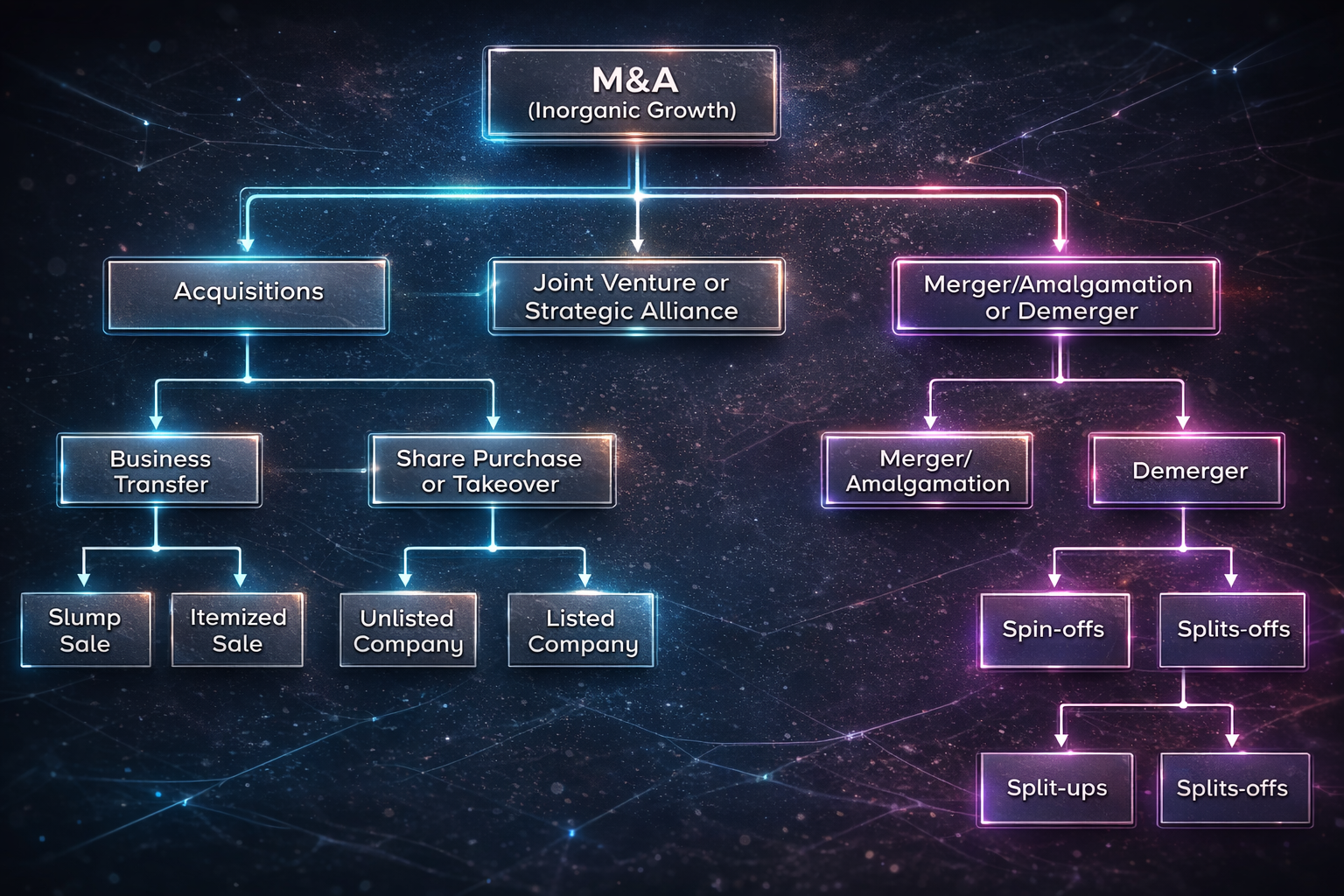

INORGANIC GROWTH:

Inorganic growth allows a company to grow faster by taking a shortcut instead of building everything step by step.

It helps the organisation achieve rapid growth by skipping several stages of normal expansion.

This type of growth is usually achieved through mergers, amalgamations, or acquisitions.

By combining with or taking over another business, the company can expand its size, market reach, and resources quickly.

This growth may result in a change in the corporate entity or legal structure of the company.

INORGANIC GROWTH THROUGH MERGERS AND ACQUISITIONS

Mergers and Acquisitions (M&A) provide an alternative to growing a business slowly on its own.

For buyers, M&A helps achieve strategic goals more quickly.

For sellers, it offers an opportunity to:

Exit the business.

Realise value : To convert the worth of an asset, business, investment into actual, measurable benefit, usually in the form of money or tangible gains.

Share future risks and rewards.

Both parties benefit by combining resources, strengths, and opportunities in a new or restructured business.

INTERNAL AND EXTERNAL EXPANSION

A company can grow in two ways: Internal expansion or External expansion.

Internal expansion means the company grows slowly over time through its regular business activities.

External expansion takes place when a company grows by acquiring or merging with other businesses.

Many companies choose this route to expand beyond their existing operations instead of growing only from retained profits.

Indian companies have frequently performed well in corporate restructuring, both within India and internationally.

Inorganic growth strategies such as mergers, acquisitions, takeovers, and spin-offs are considered powerful tools for rapid business growth.

They help companies enter new markets quickly.

They allow firms to expand their customer base.

They help in reducing competition and consolidating market position.

Companies can grow in size at a much faster pace.

They enable the adoption of new technologies, improved products, better talent, and efficient processes.

Because of these advantages, inorganic growth strategies are seen as fast-track corporate restructuring methods for growth.

CONSOLIDATING THE MARKET POSITION

Consolidating market position means to strengthen and secure a company’s existing place in the market.

This is done in order to become more stable, competitive, and difficult for rivals to challenge.

It makes your position in the market stronger and safer.

It increases control over customers, supply chains, or pricing.

It reduces competition or competitive threats.

HOW COMPANIES CONSOLIDATE THEIR POSITION IN THE MARKET

Acquiring or merging with competitors.

Expanding market share in existing markets.

Improving brand loyalty and customer retention.

Gaining economies of scale to lower costs.

UNDERSTANDING CORPORATE RESTRUCTURING

Corporate restructuring refers to the process through which a business enterprise makes significant changes to its structure.

It involves redesigning one or more aspects of a company, such as its business, financial, or legal setup.

The process is wide-ranging and comprehensive, not limited to a single change.

Through restructuring, a company can streamline and consolidate its operations.

The objective is to strengthen the company’s position so it can achieve both its short-term and long-term business goals.

A business can grow gradually over time as people begin to recognise and use its products and services, but this is usually a slow and steady process.

Alternatively, a business may grow through an inorganic process, which leads to rapid expansion.

This type of growth is marked by:

A sudden increase in the workforce.

A larger customer base.

Expanded infrastructure and resources.

An overall rise in revenue and profits of the business.

DEFINITION OF RESTRUCTURING

According to the Oxford Dictionary:

Restructuring means reorganising a company in order to work more efficiently, increase profits, or adjust to changes in the market.

Peter F. Drucker states that one of the most important changes in modern business is:

How companies operate and relate to each other.

Business relationships are no longer based only on ownership, but increasingly on strategic partnerships and collaboration.

Corporate restructuring plays an important role in helping companies become stronger and more efficient.

It helps enterprises achieve economies of scale and improve global competitiveness.

It allows companies to reach the right size by cutting unnecessary layers.

It leads to reduction in operational and administrative costs.

Corporate restructuring involves reorganising the business or financial structure of a company to improve efficiency and profitability.

It is used as a strategic tool by corporate houses to increase value for both the organisation and its investors.

NEED TO REORGANISE THE COMPANY

The need to reorganise a company can arise for many reasons, such as:

To become more competitive in the market.

To deal with difficult economic conditions.

To shift the business in a new strategic direction.

CORPORATE RESTRUCTURING AND ITS OBJECTIVES

Corporate restructuring mainly involves major changes to the company’s assets and liabilities.

It also involves making major changes to a business model, management, or financial structure.

It is done so that business operations can be carried out in a more efficient, effective, and competitive manner & deal with challenges and improve shareholder value.

It is considered an inorganic growth strategy because it helps the company grow and strengthen its position through significant structural changes.

The core objective of this process is to improve future cash flows, which in turn helps in:

Increasing market share.

Strengthening brand value.

Creating better synergies within the organisation.

AMALGAMATION

Amalgamation means the merger of one or more companies into another company.

It can also mean the merger of two or more companies to form a single new company.

In the case of Religare Finvest Limited v. State of NCT of Delhi & in the case of General Radio & Appliances Co. Ltd. v. M.A. Khader:

The Court held that:

Once two companies are amalgamated, the transferor company completely ceases to exist.

The amalgamated company acquires a new legal status.

After amalgamation, the companies cannot be treated as partners or as jointly liable for assets and liabilities.

All rights, liabilities, and obligations stand absorbed into the amalgamated company alone.

DEFINITIONS OF AMALGAMATION

(a).

According to Stroud’s Judicial Dictionary of Words and Phrases:

Amalgamation means the welding or blending of two or more business concerns into one.

So, if companies continue as separate legal entities, it cannot be called an amalgamation.

(b).

According to Black’s Law Dictionary:

Amalgamation as the act of combining or uniting businesses, often resulting in the formation of a new corporation from two or more existing ones.

(c).

The Companies Act, 2013 does not give a direct definition of amalgamation.

Instead, it lays down the procedure and legal consequences of amalgamation.

One important legal effect is that the corporate identity of the transferor company comes to an end, as it is absorbed into the transferee company.

Judicial interpretation has also clarified that the term amalgamation has no fixed legal meaning, but generally refers to a situation where:

Two companies combine to form a third entity.

One company is absorbed into another and loses its separate identity.

In essence, amalgamation results in one surviving separate company, while the other company or companies cease to exist in law.

In the case of Principal Commissioner of Income Tax v. Mahagun Realtors (P) Ltd, the Hon’ble Supreme Court clarified the true nature of amalgamation.

The Court held that:

Amalgamation is different from winding up of a company.

While the corporate identity of the transferor company comes to an end, this does not mean that the business itself disappears.

The business activities, operations, and commercial venture continue, but they now exist within the transferee company.

So, the legal shell of the old company is destroyed. The company’s activities get a new corporate home, not a complete burial.

While dealing with matters such as assessment or legal proceedings :

The underlying business continuing through the transferee company should be taken into consideration.

It is important not to treat the disappearance of a corporate entity as an automatic end to all legal or assessment proceedings.

In many areas of civil law and procedural law, even after amalgamation, a cause of action or complaint does not automatically come to an end.

This depends on the structure, purpose, and intent of the relevant law.

Courts generally try to identify:

Whether a successor or representative entity exists after amalgamation.

Whether the assets have been transferred to such entity.

Who should bear the liability if it is finally decided against the business.

THE NEED AND SCOPE FOR CORPORATE RESTRUCTURING

Corporate restructuring focuses on reorganising a company’s overall business activities to achieve specific goals at the corporate level.

These objectives are strategic in nature and aim to strengthen both the company’s performance and its long-term position.

The key advantages are:

Enhancement of Shareholder Value

Restructuring helps improve profitability, efficiency, and growth prospects.

This increases earnings, dividends, and share prices.

As a result, shareholders gain higher returns on their investment.

Better Use of Surplus Cash

Profits generated by one business unit can be reinvested in another unit with higher growth potential.

This avoids idle cash and makes sure funds are used where they can generate maximum returns.

Exploiting Interdependence Between Businesses

Companies with related businesses can share resources, technology, distribution networks, and expertise.

Restructuring allows firms to benefit from such connections, leading to operational and cost efficiencies.

Reduction of Business Risk

By restructuring operations or diversifying business activities, companies can spread risk across multiple products or markets.

This would reduce dependence on a single source of income.

Development of Core Competencies

Restructuring enables companies to focus on what they do best.

By divesting non-core activities and strengthening key areas, firms can build strong capabilities that give them a competitive edge.

Tax Advantages

Merging a loss-making company with a profitable one allows the set-off of accumulated losses and unabsorbed depreciation.

This would lead to reduced tax liability and improved cash flow.

Adapting to Technological Changes

Rapid developments in information technology force companies to upgrade systems, processes, and business models.

Restructuring helps organisations adopt new technologies to improve productivity and performance.

Global Competitiveness

Corporate restructuring helps companies scale up operations, adopt international best practices.

It also helps strengthen financial and managerial capacity, making them capable of competing in global markets.

Increase in Market Share

Through M&A or expansion strategies, companies can enter new markets, eliminate competition, & increase customer base.

Global Expansion Due to Rupee Convertibility

Convertibility of the rupee has made it easier for Indian companies, including medium-sized firms, to access global markets.

This would allow them to invest abroad, and raise international capital.

So , Restructuring supports such international expansion.

Improved Efficiency and Cost Reduction

Intense competition requires firms to streamline operations, reduce unnecessary costs, achieve synergy, and use managerial skills effectively.

Restructuring helps optimise operations and maximise efficiency.

Risk Minimisation Through Diversification

By diversifying into different products or industries, companies can balance losses in one area with gains in another.

This makes sure there is a minimum acceptable rate of return.

Revival of Sick Units and Strategic Tax Planning

When a financially weak or sick unit is merged with a successful one, the stronger company can:

Absorb losses.

Adjust unabsorbed depreciation.

Write off accumulated losses.

This leads to strategic tax planning while also reviving unproductive assets and strengthening the combined entity.

PURPOSE OF CORPORATE RESTRUCTURING

To strengthen the competitive position of an individual business.

To ensure the business contributes effectively to the overall goals of the corporate group.

To reorganise operations for greater efficiency and smoother functioning.

To restructure management systems for quicker and better decision-making.

To realign financial structures to improve stability and profitability.

To enable faster response to changing market conditions.

To align business performance with broader objectives such as growth, profitability, and market leadership.

To fully utilise the strategic assets already built by the business.

These assets may include monopoly positions, brand goodwill, exclusive rights, licences, patents, or long-term contracts.

Through restructuring, companies can reposition these assets, integrate them with other business units, or deploy them in more profitable markets.

TYPES OF RESTRUCTURING

There are essentially 4 types of Corporate Restructuring:

(a). Financial Restructuring.

(b). Market Restructuring.

(c). Organisational Restructuring.

(d). Technological Restructuring.

FINANCIAL RESTRUCTURING

Financial restructuring focuses on changing a company’s capital structure and arranging funds for new projects.

It involves reorganising equity, debt, and other financial resources of the company.

It helps in raising fresh finance for expansion or new ventures.

Financial restructuring enables a firm to recover from financial distress.

It allows the company to continue operations and revive its business without going into liquidation.

Financial restructuring may be undertaken for the following business reasons:

Poor financial performance

When a company faces continuous losses, cash flow problems, or high debt, financial restructuring helps reorganise finances.

This helps restore stability and profitability.

External competition

Increased competition may reduce margins and revenues.

Restructuring helps the company cut costs, optimise capital, and remain competitive.

Erosion or loss of market share

Declining market presence signals the need for restructuring to improve pricing, product offerings, or investment strategies.

Emerging market opportunities

New markets or business opportunities may require additional funds or a better capital structure, which financial restructuring helps achieve.

Financial restructuring involves changes in both equity and debt components of a company’s capital structure.

It includes:

Equity restructuring, such as:

Buy-back of shares.

Alteration or reduction of share capital.

Debt restructuring, such as:

Restructuring of secured long-term borrowings.

Restructuring of unsecured long-term borrowings.

Restructuring of short-term borrowings.

MARKET AND TECHNOLOGICAL RESTRUCTURING

Market restructuring involves decisions related to the product and market segments in which a company chooses to operate.

It focuses on aligning business activities with the company’s core competencies.

This is done so that the resources are concentrated on markets where the firm has a competitive advantage.

Technological restructuring occurs when new or advanced technologies change the way an industry functions.

To adapt, companies reorganise their processes, systems, and skills to remain efficient and relevant.

This form of restructuring:

Often impacts employees.

Requires new training and skill development.

May lead to layoffs as operations become more efficient.

It also involves forming alliances or partnerships with third parties that possess specialised technical expertise or resources.

Example 1:

Indian technology major Tata Consultancy Services Limited has undertaken a process of corporate restructuring with a clear focus on three core areas.

1. Cloud.

2. Agile.

3. Automation.

The company’s restructuring plan covers multiple dimensions, including:

Strengthening manufacturing and delivery capacity.

Upgrading product, technical, and technological capabilities.

Improving financial efficiency.

Reorganising employment and workforce structures.

Streamlining organisational and management systems.

Optimising purchasing and operational processes.

Example 2:

The Walt Disney Company has undertaken a reorganisation of its global technology group and parks-and-resorts division as part of its restructuring efforts.

This reorganisation has led to elimination of certain job roles, resulting in some employees losing their jobs.

At the same time, Disney is creating new roles that better support its long-term technology and business goals.

The objective is to realign its workforce and operations with future-focused technologies and strategies.

Further, Joint Ventures, Strategic Alliances, and Franchising are common examples of market and technological restructuring, as they allow companies to:

Enter new markets.

Access new technologies and expertise.

Adapt to changing business and technological environments without operating entirely on their own.

ORGANISATIONAL RESTRUCTURING

Organisational restructuring involves redesigning the internal structure, systems, & procedures of a company to improve the ability of its people to respond to change.

It focuses on enhancing the capability and efficiency of employees at all levels.

Successful organisational restructuring requires the cooperation and involvement of employees across the organisation.

Some companies restructure to expand operations by creating new departments to serve growing markets.

Other companies reorganise to downsize or eliminate departments in order to reduce overhead costs and improve efficiency.

MERGERS AND ACQUSITIONS

M&A are transactions through which the ownership of companies, business organisations, or operating units is transferred or combined.

They involve the consolidation of two companies into a single business structure.

As a part of strategic management, M&A enable enterprises to grow, shrink, or reshape their business operations.

They also help companies change the nature of their business or strengthen their competitive position in the market.

The main reasoning behind mergers and acquisitions is that two companies together can create more value than they can individually.

By combining resources, capabilities, and markets, companies can achieve synergy.

With the objective of wealth maximisation, firms continuously evaluate opportunities for mergers or acquisitions.

M&A is therefore used as a strategic route to increase overall value and competitiveness.

IMPORTANCE OF MERGERS AND ACQUISITIONS

Mergers and Acquisitions (M&A) are an important growth strategy in the modern economy.

M&A are transactions through which the ownership of companies, business organisations, or operating units is transferred or combined.

These transaction essentially result in the consolidation of two companies.

As a tool of strategic management, M&A enable enterprises to expand, downsize, or reshape their business and competitive position.

Mergers and Acquisitions (M&A) help companies grow faster and strengthen their market position in several ways:

They enable companies to expand geographically and enter new markets.

M&A help businesses scale up operations and move towards becoming market leaders.

They increase the company’s ability to distribute goods and services on a wider scale, reaching more consumers.

Wider reach leads to better brand recognition and higher sales.

Consumers benefit by getting more competitive products and improved technology due to combined expertise and resources.

REASONS FOR MERGERS AND ACQUSITIONS

Regardless of their type or structure, all mergers and acquisitions share one common objective: To create synergy.

Synergy is the combined value of the two companies is greater than the value of each company operating separately.

The idea is that the whole becomes more valuable than the sum of its parts.

The success of a merger or acquisition depends on whether this synergy is actually realised.

Synergy generally arises in two main forms:

Revenue enhancement, through increased market reach, cross-selling, better products, or stronger brand presence.

Cost savings, through economies of scale, elimination of duplicate functions, and improved operational efficiency.

ADVANTAGES OF A MERGER

Becoming Bigger:

Companies use Mergers and Acquisitions (M&A) as a fast way to expand their business.

M&A helps firms increase size and scale quickly.

It allows companies to overtake or leapfrog competitors in the market.

Organic growth (internal expansion) usually takes many years or even decades.

Through mergers or acquisitions, similar growth can be achieved in a much shorter time.

M&A therefore serves as a speedy alternative to slow, gradual business growth.

Pre-Empted Competition:

Pre-empting competition means acquiring or merging with a competitor before others do.

It prevents rivals from gaining strategic advantages through the same acquisition.

Companies use M&A to secure key markets, technologies, or resources ahead of competitors.

This factor strongly drives merger and acquisition activity.

Domination:

Domination is a motive where companies use M&A to gain control over a sector.

By merging with or acquiring major competitors, firms can strengthen market power.

Such combinations may reduce competition significantly.

Mergers between very large companies can lead to a potential monopoly.

Therefore, these transactions are subject to strict scrutiny by regulatory authorities.

Economies of Scale:

Mergers help companies achieve economies of scale.

Economies of scale means a reduction in cost per unit of a product or service.

This happens because the total output increases after the merger.

Fixed costs such as administration, infrastructure, R&D, and marketing are spread over a larger volume of production.

Bulk purchasing of raw materials leads to lower input costs.

Better utilisation of plants, machinery, and workforce reduces wastage and inefficiency.

As a result, the merged entity becomes more cost-efficient and competitive in the market.

Acquiring New Technology:

Companies must keep up with technological developments to remain competitive.

They need to apply new technologies effectively in their business operations.

Acquiring smaller companies with unique or advanced technologies helps achieve this.

Such acquisitions allow large companies to maintain or strengthen their competitive edge.

Improve Market Reach & Industrial Visibility:

Companies acquire other firms to enter new markets.

M&A helps in increasing revenues and earnings.

A merger can expand marketing and distribution networks.

Expanded networks create new sales opportunities.

Larger merged firms often have better credibility with investors.

Bigger companies usually find it easier to raise capital than smaller ones.

Tax-Benefits:

Companies sometimes use mergers and acquisitions to reduce their overall tax burden.

These tax advantages may arise due to set-off of losses, depreciation benefits, tax credits, or favourable tax treatment available to the merged entity.

While tax savings can be a significant outcome of M&A, they are not always openly stated as the main reason for the transaction.

TAX BENEFITS OF MERGERS AND ACQUISITIONS: IMPLICIT AND EXPLICIT MOTIVES

Set-off of accumulated losses

A profitable company may merge with a loss-making company and use its carried-forward losses to reduce taxable profits.(subject to tax laws).

Use of unabsorbed depreciation

Unused depreciation of one entity can sometimes be carried forward in the merged company.

Lower effective tax rate

Restructuring operations through M&A may shift profits to entities or locations with more favourable tax treatment.

Tax-efficient asset restructuring

Acquiring assets through mergers rather than direct purchase may attract tax exemptions or defer capital gains.

Utilisation of tax incentives

Merging with a company enjoying tax holidays or sector-specific incentives can extend benefits to the combined business.

IMPLICIT TAX BENEFITS

Tax benefits are considered implicit when:

The primary stated purpose of the M&A is business-related, such as expansion, synergy, or market access.

Tax advantages arise as a by-product of the transaction rather than its main justification.

Management does not publicly disclose tax savings as a driving reason.

The deal would still make commercial sense even without tax benefits.

Example:

A profitable company acquires a struggling competitor mainly to gain market share, but incidentally benefits from setting off accumulated losses.

EXPLICIT TAX BENEFITS

Tax benefits are considered explicit when:

The main objective of the M&A is tax optimisation.

The transaction is structured specifically to obtain tax advantages.

Tax savings are clearly identified, quantified, and planned in advance.

Without the tax benefit, the deal would not be economically attractive.

Example: A profitable company merges with a loss-making entity primarily to absorb its carried-forward losses and reduce tax liability.

How Mergers & Acquisitions take place

(a). By Purchase of Assets.

In a purchase of assets, the acquiring company buys specific assets of another company rather than acquiring ownership of the company itself.

The assets purchased may include land, buildings, machinery, inventory, intellectual property, contracts, or goodwill.

The buyer can choose which assets to acquire and which liabilities to assume, giving greater flexibility.

The selling company continues to exist as a separate legal entity unless it is later wound up.

How it works

The transaction is usually carried out through an Asset Purchase Agreement (APA).

Consideration may be paid in cash, shares, or a combination of both.

Ownership of each asset is transferred through separate legal formalities (Conveyance deeds, assignment of IP, novation of contracts).

Why companies prefer asset purchases

It limits exposure to unknown or contingent liabilities.

It allows acquisition of only profitable or strategic assets.

IT often used when the target company is in financial distress or insolvency.

It enables tax-efficient structuring in some cases.

Limitations

Transfer can be time-consuming and compliance-heavy.

Contracts and licenses may require third-party or regulatory consent.

Employees do not automatically transfer unless agreed.

(b). By Purchasing of Common Shares.

In a purchase of common shares, the acquiring company buys equity shares of the target company.

By acquiring a majority or controlling stake, the buyer gains ownership and control over the target company.

The target company continues to exist as the same legal entity, but with a change in shareholding.

How it works

The transaction is executed through a Share Purchase Agreement (SPA).

Shares may be purchased from existing shareholders or through a fresh issue by the company.

Consideration may be paid in cash, shares, or a combination.

Once the required shareholding is acquired, the acquirer can appoint directors and control management.

Why companies prefer share purchases

Share purchases have a simpler transfer process compared to asset purchases.

All assets, contracts, licences, and employees automatically remain with the company.

Suitable when continuity of business is important.

It is often used for strategic acquisitions and takeovers.

Limitations

The buyer also takes on all existing and contingent liabilities of the company.

Requires thorough due diligence to identify risks.

Regulatory approvals (SEBI, RBI, Competition Commission, etc.) may be required.

(c). By Exchanging of Shares for Assets.

In this method, the acquiring company acquires the assets of another company by issuing its own shares instead of paying cash.

The consideration for the asset transfer is shares of the acquiring company.

The seller receives equity ownership in the acquiring company in return for its assets.

How it works

The acquiring company issues new shares to the selling company or its shareholders.

In exchange, specified assets and, in some cases, liabilities are transferred to the acquirer.

The transaction is documented through an Asset Transfer Agreement / Scheme of Arrangement.

The selling company may continue to exist or may be wound up after the transfer.

Why companies use this method

It is useful when the acquirer wants to preserve cash.

It allows sellers to participate in future growth of the acquiring company.

It is often used in restructuring, demergers, and slump sales through court or tribunal-approved schemes.

It can be tax-efficient, depending on the structure and applicable laws.

Limitations

Share dilution occurs in the acquiring company.

Valuation of assets and shares can be complex and contentious.

Requires shareholder and regulatory approvals.

(d). By Exchanging Shares for Shares.

In this method, the acquiring company acquires a controlling stake in another company by issuing its own shares to the shareholders of the target company.

Instead of paying cash, the acquirer exchanges its shares for the shares of the target.

As a result, the shareholders of the target become shareholders of the acquiring company.

How it works

A share swap ratio is determined based on valuation of both companies.

The acquiring company issues new shares to the target company’s shareholders.

In return, the acquiring company receives equity shares of the target, often resulting in control.

The transaction is carried out through a Share Swap Agreement or a Scheme of Amalgamation.

Why companies use this method

It helps conserve cash and debt capacity.

It facilitates large-scale mergers and takeovers.

It aligns interests of both companies’ shareholders.

It is common in mergers, amalgamations, and group restructurings.

Limitations

It causes dilution of existing shareholders of the acquiring company.

The Share valuation and swap ratios may be disputed.

It requires shareholder, regulatory, and sometimes tribunal approvals.

SHARE SWAP RATIO

In many mergers and acquisitions, the deal is not completed using cash.

Instead, it is carried out through a share-for-share exchange, known as a share swap.

A share swap ratio is the proportion in which the acquiring company offers its own shares to the shareholders of the target company during a M&A.

It determines how many shares of the acquiring company a shareholder of the target company will receive in exchange for their existing shares.

The swap ratio functions like a conversion rate between the shares of the two companies, reflecting their relative value.

If the swap ratio is 2:1, it means a shareholder will receive 2 shares of the acquiring company for every 1 share held in the target company.

Key factors affecting the swap ratio

Earnings and profitability of both companies

Debt levels and financial liabilities

Market value of shares

Asset base and future growth potential