Types of Transactions in M&A - Part 1

M&A include a number of different transactions such as:

Mergers

Acquisitions

Amalgamation

Consolidations

Tender offers

Purchase of assets

Management buy-out

MERGERS

The terms merger and amalgamation are not expressly defined under the Act and are often used together as M&A.

However, there is a subtle difference between the two:

MERGER

Merger refers to the fusion of two or more companies into one.

In a merger, one or more companies lose their identity, while one company survives.

AMALGAMATION

Amalgamation refers to the blending of two or more undertakings into a single undertaking.

In an amalgamation, all existing companies lose their identity.

A new and separate legal entity is formed as a result of the amalgamation.

Amalgamation may take place by transferring two or more undertakings to a new company or to an existing company.

A transferor company is the company that merges or transfers its undertaking.

In the case of amalgamation, the transferor company is also called the amalgamating company.

A transferee company is the company that receives the undertaking.

After a merger or amalgamation, it is known as the amalgamated company.

THE WAYS IN WHICH LEGAL CONSOLIDATION CAN TAKE PLACE

A legal consolidation of two companies into a single entity can take place in the following ways:

By amalgamation, where two or more companies combine to form a new company.

By absorption, where one company is absorbed into another existing company.

By formation of a new company, where the merging companies cease to exist and a new entity is created.

The Boards of Directors of the companies involved first approve the proposal, after which shareholders approval is obtained as required by law.

Once the restructuring is completed:

The acquired company ceases to exist as a separate legal entity in the case of Merger and Amalgamation.

In an Acquisition , the acquired company will not cease to exist but it will be under the direct control of the transferee company.

Its assets, liabilities, rights, and obligations become part of the acquiring or resulting company.

Some notable examples of mergers and acquisitions include:

The acquisition of eBay India by Flipkart,

The merger of Vodafone India and Idea Cellular,

The Axis Bank’s acquisition of Free Charge.

The merger of State Bank of India with its subsidiary banks.

TYPES OF MERGERS

HORIZONTAL MERGER

A horizontal merger is a merger between companies that:

Sell similar or identical products,

Operate in the same market.

They are in direct competition with each other.

Such companies usually share the same product lines and customer base.

Key features and objectives of a horizontal merger are:

It reduces competition in the market.

It helps companies achieve economies of scale.

It allows firms to increase market share.

It may lead to market dominance or monopoly power.

It enables better control over pricing and distribution.

Example

Facebook’s acquisition of Instagram for a reported $1 billion is a classic example of a horizontal merger.

Both companies operated in the social media and photo-sharing space.

They were at similar stages of service delivery, offering overlapping features.

Through this acquisition, Facebook aimed to:

Increase its market share.

Expand its product offerings.

Reduce competition.

Access new user segments and markets.

The Walt Disney Company’s acquisition of Lucasfilm is another example of a horizontal merger.

Both companies were engaged in the production of films and television content.

The acquisition helped Disney strengthen its content portfolio, expand its franchise base, and enhance its dominance in the entertainment industry.

VERTICAL MERGER

A vertical merger is a merger between companies that operate in the same industry but at different stages of the production or supply process.

It occurs when one company buys from or sells to the other.

Such mergers usually involve a supplier and a manufacturer, or a manufacturer and a distributor.

The main purpose is to control the supply chain, reduce costs, and improve operational efficiency.

Example:

Suppose XYZ Ltd. manufactures shoes and ABC Ltd. produces leather.

ABC Ltd. has been a long-term supplier of leather to XYZ Ltd.

Since leather is a key input for making shoes, both companies operate at different stages of the same production process.

By merging, they can reduce costs, avoid middlemen, ensure steady supply, and increase profits.

This is called a vertical merger because the output of one company becomes the input of the other.

Microsoft’s Merger with Nokia.

Microsoft provided software and operating systems.

Nokia provided hardware and smartphones.

The merger helped Microsoft support its software with its own hardware, improving integration and control over the product ecosystem.

CONGLOMERATE MERGER

A conglomerate merger is a merger between two companies that do not have any common business activities.

The companies operate in completely unrelated industries.

The business of the target company is entirely different from that of the acquiring company.

Such mergers are not based on product or supply chain similarity.

The main objectives of a conglomerate merger are:

To increase the overall size of the business.

To diversify operations.

To spread business risk across different industries.

Example:

Berkshire Hathaway acquired The Lubrizol Corporation, which is a classic example of a conglomerate merger.

Berkshire Hathaway operates in diverse and unrelated businesses, such as insurance and reinsurance, utilities and energy and many more.

Its shares are listed on the New York Stock Exchange.

Lubrizol was a specialty chemical company engaged in producing and supplying technologies for transportation, industrial, and consumer markets.

It products included:

Lubricant additives for engine oils.

Additives for industrial lubricants and transportation fluids.

Fuel additives for gasoline and diesel.

Since Berkshire Hathaway and Lubrizol operate in completely unrelated industries:

Their combination does not involve product similarity or supply-chain linkage.

The acquisition was aimed at diversification, expansion of business size, and risk spreading, which are the core objectives of a conglomerate merger.

CONGENERIC MERGER

A congeneric merger is a merger between two or more businesses that are related to each other, but are not direct competitors.

The companies may be connected through:

Similar customer groups.

Related functions.

Complementary technology.

Such mergers allow companies to expand product lines, serve existing customers better, and leverage shared expertise or technology.

Example;

PVR–INOX Merger (2022)

PVR Cinemas and INOX Leisure, India’s two leading cinema chains, merged in 2022.

The merger created the largest multiplex chain in India, with over 1,500 screens.

Both companies operated in the same industry and catered to the same customer base, but had different operational strengths.

The merger resulted in synergies, such as:

Higher advertising revenues,

Reduced rental and operational costs.

Better optimisation of convenience fees.

The merged entity now operates under the name PVR-INOX.

HDFC Ltd – HDFC Bank Merger (2022)

HDFC Ltd merged with HDFC Bank in one of India’s largest financial deals, valued at around $40 billion.

Though both entities belonged to the financial services sector, their product offerings were different.

HDFC Limited was operation on housing finance while HDFC bank was operating in Banking Services.

The merger resulted in a single legal entity, while continuing to offer distinct services to customers.

This merger strengthened scale, balance sheet efficiency, and cross-selling opportunities.

Citicorp-Travelers Group Merger

A classic global example of a congeneric merger is the merger of Citicorp and Travelers Group.

The $70 billion deal led to the creation of Citigroup Inc.

Although both companies operated in financial services, they offered different product lines such as banking, insurance, and investment services.

The merger allowed the combined entity to provide diverse financial products under one umbrella.

REVERSE MERGER

A reverse merger is a type of merger in which a private company becomes a public company by acquiring an already listed public company.

It allows the private company to avoid the lengthy and costly process of an initial public offering (IPO).

Instead of going public on its own, the private company acquires a public company, often one with minimal operations.

After the merger, the private company’s business takes over, and it effectively converts into a public company.

This method saves time, cost, and regulatory compliance efforts associated with traditional public listing.

Example:

A well-known example of a reverse merger in India is the merger of ICICI with ICICI Bank in 2002.

At the time of the merger, ICICI (the parent company) had a balance sheet more than three times larger than that of its subsidiary, ICICI Bank.

Despite being the larger entity, ICICI merged into ICICI Bank, allowing the banking subsidiary to become the surviving public entity.

This restructuring enabled the group to simplify its structure, strengthen banking operations, and align better with regulatory and market requirements.

The transaction is regarded as a classic reverse merger, where the parent company was absorbed into its listed subsidiary.

ACQUISTION

An acquisition takes place when one company takes ownership of another company’s shares, equity interests, or assets.

It involves the purchase of a controlling interest in the share capital of an existing company.

Through acquisition, one company gains control over the management and operations of the other.

Even after the takeover, the acquired company continues to exist as a separate legal entity.

Although ownership and management may change, both companies retain their individual legal identities.

In an acquisition, the companies remain independent and separate legal entities.

There is only a change in ownership or control of the company.

When an acquisition is carried out without the consent of the target company’s management or is unwilling, it is known as a takeover.

Examples:

Flipkart and Myntra ($300 to 330 million).

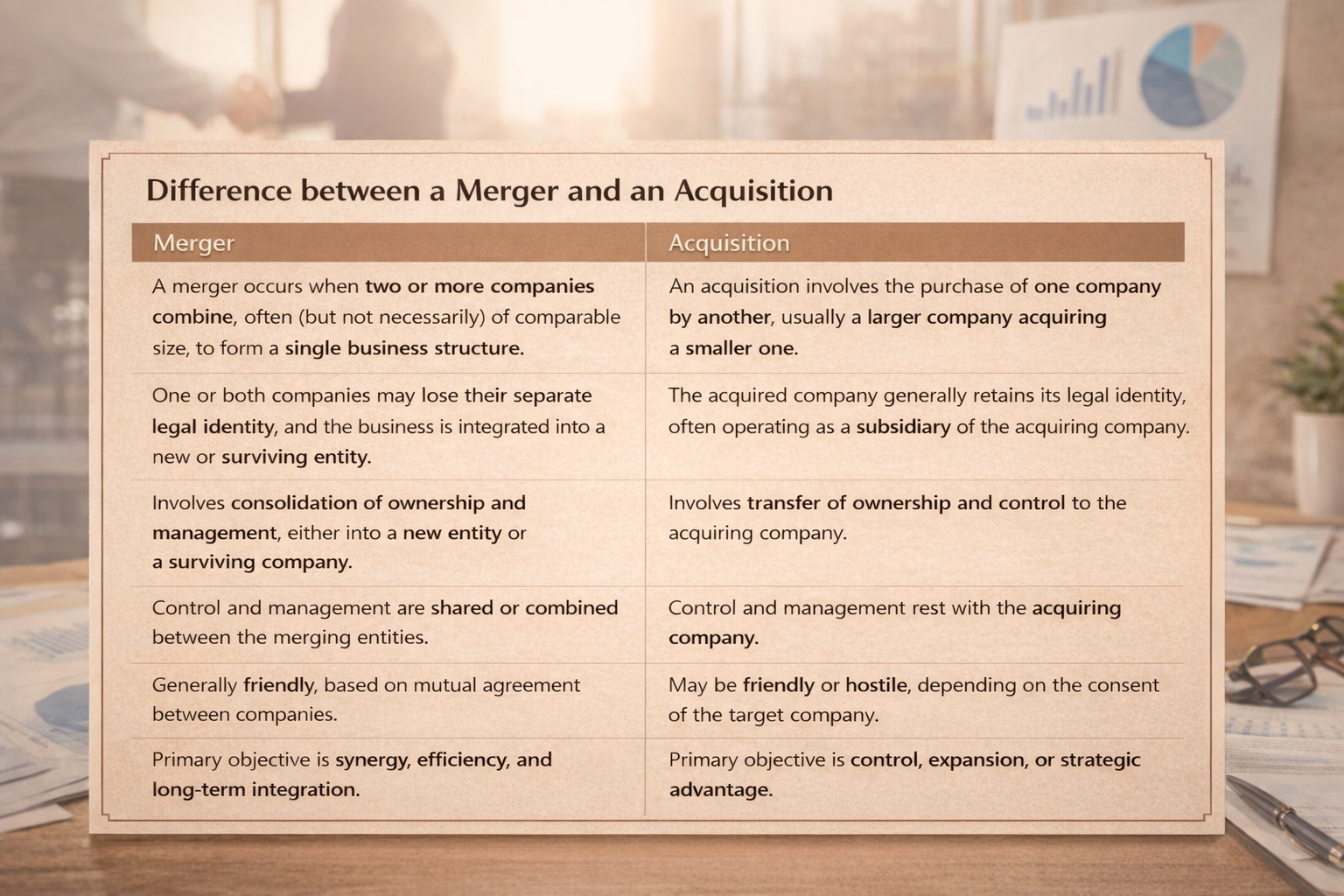

DIFFERENCE BETWEEN A MERGER AND AN ACQUISITION

COMMERICAL AND ECONOMIC PERSPECTIVE OF A M&A.

From a commercial and economic perspective, mergers and acquisitions often lead to the same practical outcome, even though they are legally different.

In both cases, there is usually a consolidation of assets and liabilities under one controlling entity.

Because of this, the distinction between a Merger and an Acquisition becomes blurred in practice.

A transaction structured legally as an acquisition may still result in one company’s business coming under the indirect ownership of the other company’s shareholders.

On the other hand, a transaction structured legally as a merger may give shareholders of both companies shared ownership and control in the combined enterprise.

In essence, while the legal form may differ, the economic effect often remains similar, with businesses combining their operations, ownership, and control.

STOCK SWAP

A stock swap occurs when the shareholders of the target company exchange their shares for shares of the acquiring company as part of a merger or acquisition.

Instead of receiving cash, shareholders are paid in shares of the acquiring company.

To ensure fairness, the shares of both companies must be properly valued.

Based on this valuation, a swap ratio is determined, which decides how many shares of the acquiring company are given for each share of the target company.

AMALGAMATION

Amalgamation is used when companies decide that a fresh start under a new corporate identity is strategically better than continuing under any existing structure.

It is common where businesses are of comparable size or strength, and neither wishes to remain dominant.

Amalgamation is defined as the combination of one or more companies into a single entity.

It includes the following types:

(i). Formation of a new company

Two or more existing companies join together.

A new company is formed.

All the combining companies lose their separate legal identities.

(ii). Absorption or blending of one company by another

One company is absorbed into an existing company.

The absorbed company ceases to exist independently.

The surviving company takes over the assets and liabilities of the absorbed company.

In either case , a new company is formed, which takes over: All assets, all liabilities, and All business operations of the amalgamating companies.

Shareholders of the old companies become shareholders of the new entity.

ABSORPTION (MERGER INTO AN EXISTING COMPANY)

Absorption is preferred when one company is financially stronger, larger, or more established.

This company would then intend to expand by taking over another company without disturbing its own identity.

So the transferor company is wound up and the transferee company continues to exist.

The company or companies that are absorbed lose their separate legal existence after amalgamation.

The shareholders of the amalgamating company become shareholders of the new or amalgamated company.

All property, assets, rights, and liabilities of the amalgamating company are:

Taken over by, or transferred to the new company or the existing amalgamated company.

Amalgamation involves the transfer of the entire undertaking of one or more companies.

The purpose is to unite the businesses and operations of two or more companies under one control.

The resulting company may be: A newly incorporated company formed for this purpose.

The core essence of amalgamation is creating an arrangement that brings multiple undertakings under a single corporate entity.

After amalgamation, only the amalgamated company continues to exist, while the amalgamating companies cease to exist independently.

DEFINTION OF THE TERM AMALGAMATION

The term amalgamation is not defined under the Companies Act, 2013 but it is defined under the Income Tax Act , 1961.

In accordance Section 2(1B) of the Income Tax Act, 1961 provides a statutory definition of amalgamation.

Amalgamation refers to the merger of companies.

It may involve one or more companies merging with an existing company, or

Two or more companies merging to form a new company.

The company or companies that merge are known as the amalgamating companies.

The company with which they merge, or the new company formed as a result, is known as the amalgamated company.

Such merger takes place in a manner that :

Automatic Transfer of Property upon Amalgamation

Immediately before the amalgamation, the amalgamating company or companies own certain property.

Upon amalgamation, this entire property stands transferred to the amalgamated company.

The transfer happens automatically as a direct result of the amalgamation.

No separate deed, assignment, or conveyance is required for such transfer.

Automatic Transfer of Liabilities upon Amalgamation

Immediately before the amalgamation, the amalgamating company or companies have certain liabilities and obligations.

Upon amalgamation, all such liabilities and obligations become those of the amalgamated company.

This transfer of liabilities takes effect automatically as a consequence of the amalgamation.

No separate agreement, novation, or consent is required for the liabilities to pass to the amalgamated company.

Continuity of Shareholding upon Amalgamation

Shareholders who hold at least three-fourths (75%) of the value of shares in the amalgamating company or companies are taken into account.

While calculating 75%, any shares that are held by the amalgamated company, its subsidiary, or their nominees before the amalgamation are ignored.

These qualifying shareholders automatically become shareholders of the amalgamated company once the amalgamation takes effect.

Their status as shareholders of the amalgamated company arises because of the amalgamation, and not because they separately bought shares in it.

This conversion of shareholding is not treated as a purchase of assets of one company by another.

It is also not treated as a distribution of assets after winding up of the amalgamating company.

REASONS FOR AMALGAMATION

To Acquire Cash Resources

Enables the acquiring company to gain immediate access to liquid funds.

Helps meet working capital needs without raising external finance.

Useful for funding expansion, debt repayment, or new projects

To Eliminate Competition

Reduces or removes direct competitors from the market.

Helps strengthen market position and pricing power.

Leads to increased market share and customer base.

Tax Savings / Advantages

Allows set-off of accumulated losses and unabsorbed depreciation.

Helps in optimizing tax liability through better tax planning.

Encourages restructuring of financially weak companies

Economies of Large-Scale Operations

Reduces cost per unit due to higher production volume.

Enables bulk purchasing, shared infrastructure, and better utilization of resources.

Improves operational efficiency and profitability

To Increase Shareholders’ Value

Enhances earnings per share through synergy benefits.

Leads to higher dividends and capital appreciation.

Creates long-term value through improved performance

To Reduce Degree of Risk by Diversification

Spreads business risk across different products or markets.

Reduces dependence on a single line of business.

Stabilizes income and cash flows

Managerial Effectiveness

Combines skilled management and technical expertise.

Improves decision-making and corporate governance.

Eliminates inefficient or duplicate managerial functions.

To Achieve Growth and Financial Gain

Enables rapid expansion compared to organic growth.

Improves financial strength and borrowing capacity.

Helps achieve strategic and long-term business goals

Revival of Weak, Sick, or Insolvent Company

Helps financially distressed companies survive.

Utilizes idle assets and workforce efficiently.

Protects employment and business continuity.

Survival

Helps companies withstand market pressure and economic downturns.

Provides stability in highly competitive or declining industries.

Prevents liquidation or closure

Sustaining Growth

Ensures continuity of business expansion.

Helps adapt to changing market conditions.

Supports long-term competitiveness and stability

CONSOLIDATION

Consolidation results in the formation of a completely new company, distinct from the existing companies involved.

Both companies proposing to consolidate must obtain approval from their respective stockholders/shareholders.

The approval is generally given through special resolutions passed in shareholders’ meetings.

Once the consolidation is approved, the existing companies cease to exist as separate legal entities.

All assets, liabilities, rights, and obligations of the consolidating companies are transferred to the newly formed company.

The stockholders of both companies receive common equity shares in the new company.

The shareholding in the new firm is usually based on a pre-determined exchange ratio.

Example:

Citicorp and Travelers Insurance Group becomes Citigroup (1998)

In 1998, Citicorp and Travelers Insurance Group announced a consolidation.

This consolidation led to the creation of an entirely new company called Citigroup.

Both Citicorp and Travelers ceased to exist as independent legal entities after the consolidation.

Shareholders of both companies approved the transaction and received equity shares in Citigroup.

The objective was to create a financial services giant offering banking, insurance, and investment services under one umbrella.

This deal is a classic example of consolidation, where two companies merge to form a new corporate entity.

TENDER OFFER

In this method, one company (the acquiring company) makes an offer to buy the outstanding shares of another company (the target company).

The offer is made at a specific price per share, which is usually higher than the current market price to encourage shareholders to sell.

The acquiring company communicates the offer directly to the shareholders of the target company, not to its management.

Such an offer is commonly known as a tender offer.

Shareholders are given a fixed time period to decide whether to accept or reject the offer.

If a sufficient number of shareholders accept the offer, the acquiring company gains controlling interest in the target company.

Once control is acquired, the target company may: Continue as a subsidiary or be merged with the acquiring company.

This method allows the acquirer to bypass resistant management of the target company.

It is often used in hostile takeovers, where the board of the target company does not support the acquisition.

The transaction results in a change in ownership, while the legal identity of the target company may continue unless further restructuring occurs.

Example:

ABC Ltd is a publicly listed company whose shares are currently trading at $15 per share in the market.

Michael, a venture capitalist, intends to take over control of ABC Ltd.

He makes an offer to purchase shares at $18 per share, which is higher than the prevailing market price.

The higher price represents a control premium, meant to motivate shareholders to sell their shares.

The offer is conditional upon Michael’s firm acquiring at least 51% of the total shareholding of ABC Ltd.

Acquiring 51% or more shares would give Michael’s firm majority ownership and management control.

The offer would typically be made directly to the shareholders of ABC Ltd, often through a tender offer.

Shareholders may choose to accept or reject the offer based on the price advantage and future prospects.

If the 51% threshold is met, the takeover is successful; if not, the offer fails and lapses.

ACQUSITION OF ASSETS

In a purchase of assets, one company (the acquiring company) buys specific assets of another company (the selling company).

The acquiring company may purchase:

Tangible assets such as land, buildings, machinery, and inventory.

Intangible assets such as trademarks, patents, goodwill, and licenses.

The selling company must obtain approval from its shareholders before transferring substantial assets.

Unlike share acquisition, the acquiring company does not automatically take over all liabilities of the selling company, unless expressly agreed.

This method allows the acquirer to choose only desirable assets and avoid unwanted risks or debts.

Purchase of assets is common in bankruptcy or insolvency proceedings, where the distressed company cannot continue operations.

During bankruptcy, multiple companies may bid for different assets of the bankrupt company

The bidding process helps maximize the value of assets for creditors

After the final transfer of assets, the bankrupt company is usually liquidated or dissolved.

Example:

XYZ Motors Ltd, an automobile parts manufacturer, enters bankruptcy due to heavy losses and mounting debt.

During the bankruptcy process, its assets are put up for sale to repay creditors.

Alpha Auto Components Pvt. Ltd. bids to acquire:

XYZ Motors’ manufacturing plant, machinery and equipment, and certain design patents.

The shareholders of XYZ Motors approve the sale of these assets as required by law.

Alpha Auto Components purchases only the selected assets and does not assume XYZ Motors’ existing debts or liabilities.

After the transfer is completed, XYZ Motors is liquidated, and the sale proceeds are distributed among creditors.

MANAGEMENT BUY-OUT

A MBO is a transaction in which a company’s existing management team purchases the assets and operations of the business they manage.

In an MBO, control shifts from the current owners to the internal management, rather than to an external buyer.

MBOs are attractive to professional managers because they gain the dual role of managers and owners.

Ownership offers greater financial rewards, including profit participation and capital appreciation, compared to being salaried employees.

Managers are often well placed to execute an MBO because they have deep knowledge of the business, operations, and risks.

From the owner’s perspective, an MBO provides a smooth exit option, as the business continues under familiar leadership.

WHY A MANAGEMENT BUY-OUT IS PREFERRED

A sale to management may be preferred over a trade sale because the number of potential external buyers may be limited.

Vendors may feel uncomfortable approaching competitors, as this could require disclosure of confidential or sensitive business information.

There may be a concern that competitors could misuse such information if the sale does not go through.

Owners may have a strong desire that the company continues independently, rather than being absorbed into another business.

Vendors often believe that the existing management represents safe hands, ensuring continuity of values, culture, and employee welfare.

HOW MANAGEMENT BUY0OUT WORKS

A management buyout (MBO) involves the management team pooling their own resources to acquire all or part of the company they manage.

The acquisition may be financed through a mix of personal funds, borrowings, or external funding.

In most cases, the management team acquires full ownership and control of the business.

After the MBO, managers transition from employees to owner-managers, combining operational control with ownership rights.

Using their existing expertise and familiarity with the business, the management team aims to grow the company and drive it forward independently.

FACTORS THAT MAKE A SUCCESSFUL MBO

Company with a strong track record of profitability

Demonstrates stable operations and consistent earnings.

Increases confidence of lenders and investors.

Reduces uncertainty in valuing the business.

Good future prospects with low risk factors.

Indicates potential for sustainable growth after the buyout.

Ensures the business can withstand market and economic changes.

Makes long-term ownership more viable for management.

Strong and committed management team with mixed skills

Combines operational, financial, strategic, and leadership expertise.

Shows unity and long-term commitment to the business.

Improves execution of post-buyout growth plans.

Vendor willing to sell to management at a realistic price

Reflects trust in the management team.

Facilitates smoother negotiations and deal closure.

Prevents overvaluation that could strain future performance.

Fundable deal structure supported by future cash flows.

Ensures the purchase price and financing can be serviced from business earnings.

Reduces reliance on excessive debt or external support.

Supports financial stability and long-term success of the MBO.

PURCHASE OF COMPANY AS RESOLUTION APPLICANT UNDER IBC LAW

The primary objective of the Insolvency and Bankruptcy Code, 2016 (IBC) is to revive financially distressed companies instead of liquidating unnecessarily.

The Code focuses on the approval of an effective resolution plan that can restore the company’s operations and viability.

Another key aim is the maximization of the value of assets of the corporate debtor, so that losses to creditors, employees, and other stakeholders are minimized.

Under the IBC framework, when a company enters insolvency, it is placed under a formal resolution process.

During this process, resolution applicants (companies, groups, or individuals) are invited to participate in a competitive bidding process.

Interested applicants submit resolution plans, proposing how they will:

Acquire or take over the insolvent company.

Restructure its debts.

Revive its business operations.

The resolution plan that is found to be the most viable and beneficial is selected.

Viability is assessed in terms of the company’s revival prospects and maximum value for stakeholders.

The selected plan must receive approval from the creditors.

The plan also requires confirmation by the adjudicating authority.

Through this process, the insolvent company can be taken over by a new owner.

This allows the business to be revived and continued as a going concern, instead of being liquidated or shut down.