Prospectus & Allotment of Securities

Understanding Financial Instruments

Instrument

In law and finance, an instrument simply means a formal written document that creates or records a legal right or obligation.

A cheque , A bond certificate , A share certificate . A promissory not and A contract are all Instruments.

Basically, if a document gives someone a right (like the right to receive money, shares, interest, etc.) or creates an obligation (like the obligation to pay), it is called an instrument.

Financial Instrument

A financial instrument is a type of instrument (document or contract) that deals specifically with money, investment, or ownership.

A financial instrument is any contract that gives:

One party a financial asset (like money, shares, interest, returns), and

Another party a financial liability or equity.

A financial instrument is a legal document that shows you own something valuable (like shares) or you are owed something (like interest or repayment).

Examples:

Shares:

Shares represent a portion of ownership in a company.

When you hold shares, you become a part-owner and may receive dividends and voting rights depending on the type of shares.

Debentures/Bonds:

These are documents showing that the company has borrowed money from you.

In return, it promises to pay you interest at agreed intervals and repay the principal on maturity.

You are a creditor, not an owner.

Mutual fund units:

The fund units reflect your contribution to a pool of money collected from many investors.

A professional fund manager invests this pool in securities like shares, bonds, etc.

Your units represent your share in the total fund.

Bank deposits:

Bank Deposits means that the bank owes you the money you place with it.

The bank uses these funds for lending and investment, and pays you interest (depending on the type of deposit).

Understanding Securities

Securities are financial instruments that represent an ownership position in a company.

Securities can also represent a creditor relationship with a company or government.

Securities allow companies to raise funds for business expansion, projects, or other financial needs, while providing investors with an opportunity to earn returns.

Securities can also include hybrid instruments, like preference shares, that have characteristics of both debt and equity.

Securities are tradable and generally fall into four broad categories:

Equity Securities (Shares/Stocks):

Represent ownership in a company.

Shareholders are owners and can earn profits through dividends and capital appreciation.

Debt Securities (Debentures/Bonds):

Debt Securities represent a loan made by an investor to the company.

Investors earn interest and are repaid the principal at maturity.

Derivative Securities

Derivative is a financial instrument whose value depends on (or is derived from) the value of another asset, called the underlying asset.

The underlying asset could be Shares , Bonds , Gold , Currency , Interest rates ,Market indices (like NIFTY, SENSEX).

A derivative has no independent value of its own.

Its value changes when the value of the underlying asset changes.

Ex. If you have a derivative based on Tata Steel shares, your derivative becomes valuable only if Tata Steel’s share price moves.

Types of Derivatives:

Futures - A contract to buy or sell something in the future at a price decided today.

Options - A right (but not an obligation) to buy or sell an asset later.

Swaps - A contract where two parties exchange cash flows, like interest payments.

Forwards - A private agreement to buy or sell in the future, similar to futures but not traded on an exchange.

Why derivatives Exist?

Hedging: To protect against price changes (like insurance).

Speculation: To make profit from price movements.

Arbitrage: To earn small risk-free profits from price differences.

Hybrid Securities

A hybrid security acts partly like a share and partly like a loan.

A hybrid security is a financial instrument that mixes features of both:

Equity (ownership)

Debt (loan/interest)

It combines characteristics of shares and bonds.

Types of Hybrid Securities:

Preference Shares:

Preference shares (also called preferred shares) are a type of share that gives the shareholder special rights and priority compared to ordinary equity shareholders.

They are called “preference” because the shareholder gets preferential treatment in two major areas:

1. Preference in Dividend

Preference shareholders get their dividend first, before equity shareholders.

They usually receive a fixed rate of dividend (like interest on a loan).

If a company declares dividends, preference shareholders must be paid first.

2. Preference in Return of Capital

If the company is being wound up or liquidated, preference shareholders get their capital repaid before equity shareholders.

Preference shareholders generally cannot vote in company decisions.

They get voting rights only in special situations (e.g., when dividend isn’t paid).

Preference shares are a hybrid security because they have:

Debt-like features (Fixed Returns and the priority to be paid before)

Equity-like features (Form part of share capital)

They are owners, but with less control than equity shareholders.

Convertible Debentures:

Convertible debentures are long-term debt instruments issued by a company that pay a fixed rate of interest, but with an added option:

The investor can convert them into equity shares after a certain period or on meeting specific conditions.

They start off as a loan so you are a creditor earning interest and can later be turned into ownership, making you a shareholder.

Because they blend the features of both debt and equity, they are considered a hybrid financial instrument.

Companies often issue convertible debentures to raise money at a lower interest rate, since investors are willing to accept reduced interest in return for the potential benefit of becoming shareholders in the future.

Warrants:

Warrants are financial instruments issued by a company that give the holder a right (but not an obligation) to buy the company’s shares at a fixed price, within a specified time in the future.

They do not represent ownership when issued but instead, they act as a future option to become a shareholder.

Warrants are often issued along with debentures or preference shares as an additional incentive for investors.

Warrants provide the potential to buy shares later at a favourable price if the company performs well.

The main advantage for investors is that warrants allow participation in future share price increases without immediately investing large amounts.

For the company, warrants help raise capital and attract investors by offering this future benefit.

Perpetual Bonds:

Perpetual bonds are a special type of debt instrument that have no maturity date.

This means the company is not required to repay the principal amount at any fixed time.

Instead, the bondholder receives regular interest payments (called coupons) indefinitely, as long as the bond is held.

Because there is no repayment of principal, perpetual bonds behave partly like equity, even though they are issued as debt.

Banks and financial institutions issue perpetual bonds to strengthen long-term capital without creating pressure of repayment.

The interest rate on these bonds is usually higher than normal bonds, because investors accept the risk of not getting principal back.

Understanding Allotment

Allotment refers to the formal process by which a company assigns or distributes securities to applicants after an issue.

Allotment happens after the company receives applications for shares or debentures.

It determines who gets how many securities, ensuring it is done fairly according to rules.

Companies issue allotment letters to successful applicants as proof of their investment.

Proper allotment ensures legal ownership and compliance with regulatory requirements under the Companies Act.

Rule 2: Definitions

(1).

(a).

Act means the Companies Act, 2013.

Whenever the word “Act” is used in these rules, it refers to that Act.

(b).

Annexure means attachment or document added at the end of a main document to provide additional information, evidence, or clarification.

Annexure attached to these rules.

It can be any schedules, forms, or details listed there are part of these rules.

(c).

Fees means the fees prescribed under the Companies (Registration Offices and Fees) Rules, 2014.

Whenever fees are mentioned, they must be paid as per those rules.

(d).

Form or e-Form refers to the specific forms provided in the Annexure to these rules.

These are the forms that companies must use for different filings or purposes under these rules.

(e).

Regional Director means a person appointed by the Central Government in the Ministry of Corporate Affairs to act as a Regional Director.

(f).

Section means a section of the Companies Act, 2013.

So whenever a section number is mentioned, it refers to a section of the Act.

(2).

If any term or expression appears in these Rules but is not defined within these Rules themselves, then its meaning must be taken from:

The Companies Act, 2013.

The Companies (Specification of Definitions Details) Rules, 2014, whichever of these laws contains the definition.

Rule 3. Information to be stated in the Prospectus - Omitted.

Rule 4: Reports to be set up in a Prospectus - Omitted.

Rule 5: Other Matters and Reports to be stated in the Prospectus - Omitted.

Rule 6: Period for which information to be provided in certain cases - Omitted.

Rule 7: Variation in terms of contracts referred to in the prospectus or objects for which prospectus was issued.

(1).

If a company has raised money from the public through a prospectus & still has some of that money unutilized, then the company cannot change:

The terms of the contracts mentioned in the prospectus.

The objects (purposes) for which the prospectus was issued.

To make such a change, the company must:

Pass a special resolution through a postal ballot.

The notice for this special resolution must include certain mandatory particulars, namely:

(a). What the company originally intended to use the raised money for.

(b). The full amount collected from the public through the prospectus.

(c). How much of the raised money has been used for the purposes stated in the prospectus.

(d). How far the company has progressed in fulfilling the original project/objects.

(e). The balance amount still lying unused from the funds raised

(f). Details of the exact changes the company wants to make to:

The terms of contracts mentioned in the prospectus.

The objects for which the money was originally raised.

(g). Why the change is necessary and how it benefits the company or shareholders.

(h). By when the company expects to complete the new/altered objectives.

(i). Omitted

(j). Possible risks or uncertainties associated with the modified project/objective.

(k). Any additional details shareholders need to make an informed decision on the special resolution.

(2).

If a company wants to change the terms of a contract mentioned in the prospectus or alter the objects for which the prospectus was issued, then:

It must publish an advertisement of the notice.

The advertisement must be in Form PAS-1.

This is the prescribed format under the Prospectus and Allotment Rules.

The advertisement must be published at the same time as the Postal Ballot notice is sent to shareholders.

So ,as soon as the company dispatches/postally sends the notice of special resolution to members.

On that very day, it must also publish the PAS-1 advertisement in newspapers.

(3).

The notice shall also be placed on the web-site of the company, if any.

To Access Form PAS-1: https://ca2013.com/returns/pas-1/

Rule 8. Offer of Sale by Members.

(1)

All provisions of Part I of Chapter III (“Prospectus and Allotment of Securities”) of the CA , 2013 and its rules apply to an offer for sale under Section 28.

However, the following provisions do not apply to such an offer:

(a).

The requirement to receive a minimum amount before allotment does not apply.

Because the company is not issuing new shares and only existing shareholders are selling.

(b).

The rule that prescribes the minimum value of each application does not apply.

(c).

The Board normally must state how the company will use the money raised from the issue.

In an offer for sale, the money goes to the selling shareholder(s), not the company.

So, this requirement does not apply.

(d).

If certain information or requirements cannot be compiled, or cannot be provided by the selling shareholder (offeror), then such provisions can be exempted, but only if:

The offeror gives detailed justification explaining why compliance is not possible.

These exemptions exist because an offer for sale does not raise money for the company, and is made by an existing shareholder (not the company).

So, many obligations applicable to a fresh issue do not logically fit.

(2).

The prospectus issued under section 28 shall disclose the name of the person or persons or entity bearing the cost of making the offer of sale along with reasons.

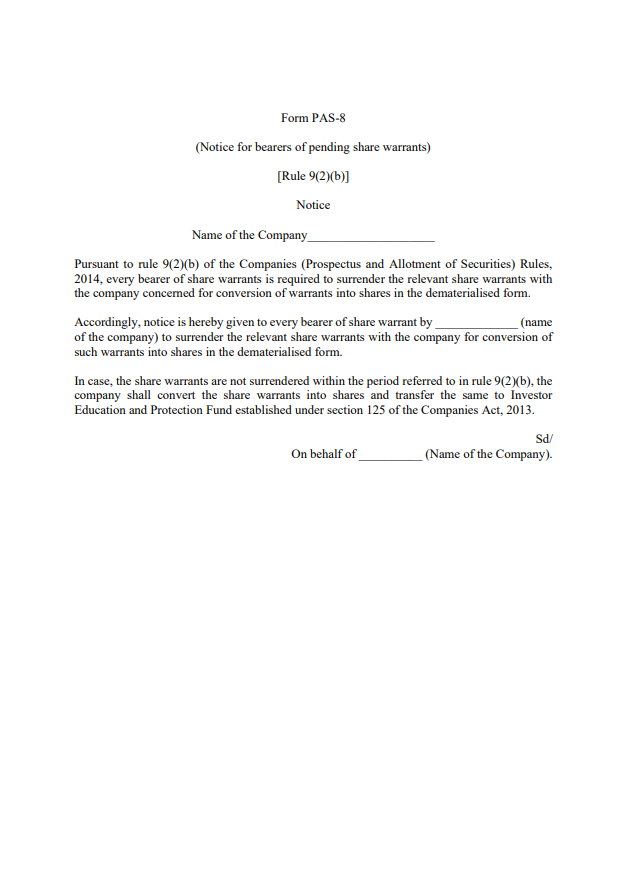

Rule 9. Dematerialisation of securities.

(1).

When a public company makes a public offer of convertible securities, its promoters are required to hold those securities only in dematerialised (demat) form.

Provided that:

If the promoters were holding any convertible securities in physical form up to the date of the initial public offer (IPO),

They must convert all such physical holdings into demat form before the IPO is made.

After the IPO, the promoters must continue to hold their entire convertible-security shareholding only in demat form.

(2).

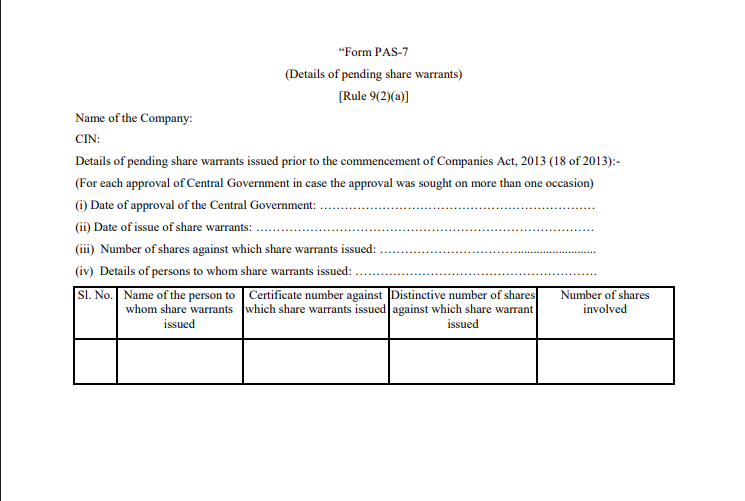

Every public company which issued share warrants prior to commencement of the Companies Act, 2013 (18 of 2013) and not converted into shares shall:

(a).

The company must inform the Registrar about all such unconverted share warrants.

This must be done within three months from the date on which the Companies (Prospectus and Allotment of Securities) Second Amendment Rules, 2023 come into effect.

The information must be submitted in Form PAS-7.

(b).

Within six months from the commencement of the Companies (Prospectus and Allotment of Securities) Second Amendment Rules, 2023, the company must take the next step.

The company must require the bearers of the share warrants to:

Surrender their share warrants to the company & get the corresponding shares dematerialised into their demat accounts.

To inform the warrant holders, the company must issue a public notice in Form PAS-8.

This notice must be:

Posted on the company’s website (if it has one) and published in:

A vernacular-language newspaper circulating in the district.

An English newspaper widely circulated in the State where the company’s registered office is located.

(3).

If a bearer of a share warrant does not surrender the warrant within the six-month period mentioned in (2) then:

The company must step in and convert those share warrants into dematerialised form on its own.

After conversion, the company must transfer the dematerialised shares to the Investor Education and Protection Fund (IEPF) established under Section 125 of the Companies Act.

To Access Form PAS-7: https://ca2013.com/wp-content/uploads/2023/10/Form-PAS-7.pdf

To Access Form PAS-8: https://ca2013.com/wp-content/uploads/2023/10/Form-PAS-8.pdf

Rule 9A. Issue of securities in dematerialised form by unlisted public companies.

(1).

Every unlisted public company must follow these requirements:

(a). It must issue all new securities only in dematerialised (demat) form and no physical certificates can be issued.

(b). It must also facilitate the dematerialisation of all its existing securities.

These obligations must be carried out in accordance with the Depositories Act, 1996 and the regulations made under that Act.

(2).

When an unlisted public company plans to:

Issue any securities.

Conduct a buyback.

Issue bonus shares.

Make a rights offer then:

It must ensure before making such an offer that the entire holding of securities belonging to its:

Promoters , Directors & Key managerial personnel (KMPs) is fully dematerialised as per the Depositories Act, 1996 and the regulations made under it.

(3).

Every holder of securities of an unlisted public company must follow these rules:

(a).

If the security holder wants to transfer any of their securities on or after 2nd October 2018, they must first dematerialise those securities before the transfer can take place.

(b).

If the security holder wants to subscribe to new securities of an unlisted public company on or after 2nd October 2018, they must ensure that all their existing securities are already in dematerialised form before subscribing.

(4).

Every unlisted public company must enable its shareholders to dematerialise all existing securities.

To do this, the company must make the required application to a depository (as defined under Section 2(1)(e) of the Depositories Act, 1996).

The company must obtain a separate ISIN (International Securities Identification Number) for each type of security it has issued.

After securing the ISIN, the company must inform all existing security holders that dematerialisation facilities are available.

(5)

Every unlisted public company must ensure the following:

(a).

It must pay all fees on time , both admission fees and annual fees to:

The depository, and the registrar to an issue and share transfer agent, as per the agreements executed with them.

(b).

It must always maintain a security deposit with the depository and registrar/share transfer agent.

This deposit must be at least equal to two years’ fees, and must be kept in whatever form the parties agree upon.

(c).

It must comply with all regulations, guidelines, directions, or circulars issued by:

The Securities and Exchange Board of India (SEBI), and the Depository, relating to dematerialisation of shares of unlisted public companies and related matters.

(6).

If an unlisted public company fails to comply with (5) then:

The company is prohibited from carrying out the following actions:

Making any offer of securities.

Buying back its securities.

Issuing bonus shares.

Making a rights issue.

This restriction continues until all overdue payments to the depositories or the registrar/share transfer agent are fully made.

(7).

Except where (5) provides otherwise, the general rules governing depositories and dematerialisation will apply.

This includes the provisions of:

The Depositories Act, 1996.

The SEBI (Depositories and Participants) Regulations, 2018.

The SEBI (Registrars to an Issue and Share Transfer Agents) Regulations, 1993.

These laws and regulations will apply mutatis mutandis, meaning they apply with necessary changes or adaptations to fit the context of unlisted public companies.

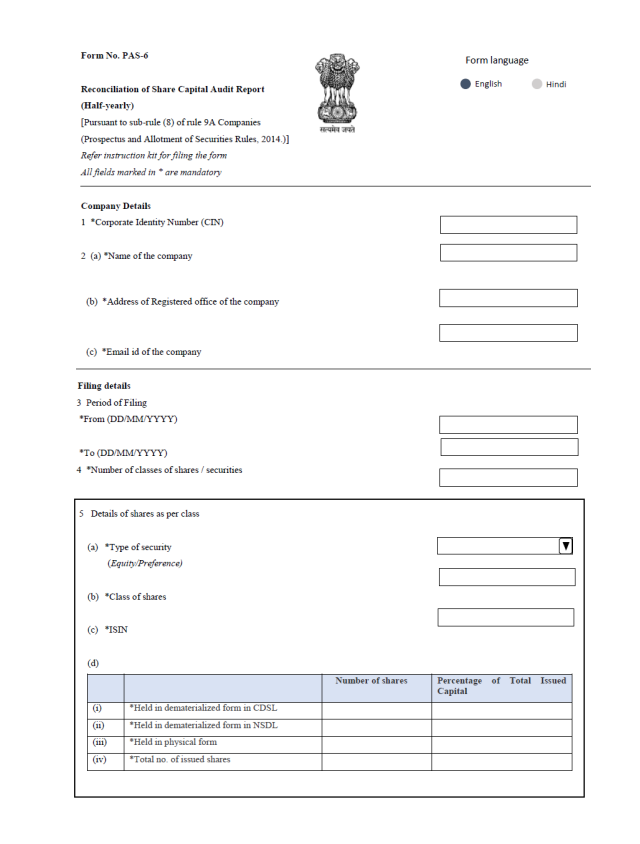

(8).

Every unlisted public company covered by this rule must file Form PAS-6.

This form must be submitted to the Registrar of Companies (ROC).

The filing must be done within 60 days from the end of each half-year (April–September and October–March periods).

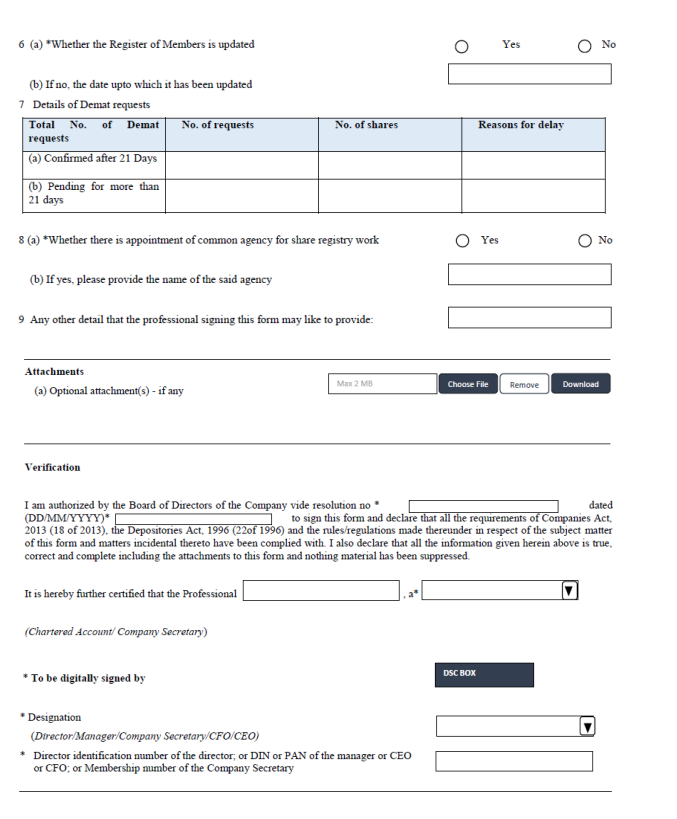

The form must be duly certified by either:

A Company Secretary in practice, or A Chartered Accountant in practice.

The filing must be accompanied by the prescribed fee as per the Companies (Registration Offices and Fees) Rules, 2014.

(8A).

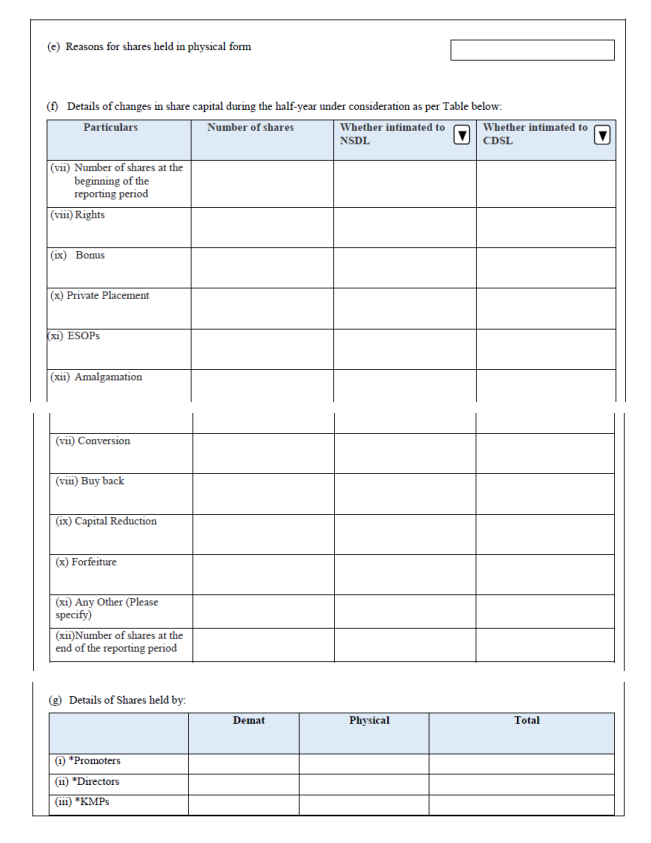

The company shall immediately bring to the notice of the depositories any difference observed in its issued capital and the capital held in dematerialised form.

(9).

If any security holder of an unlisted public company has a grievance regarding matters covered by this rule,

The grievance must be submitted to the Investor Education and Protection Fund (IEPF) Authority.

(10).

If the IEPF Authority needs to take action against:

A depository.

A depository participant

A registrar to an issue and share transfer agent.

It can only do so after first consulting the Securities and Exchange Board of India (SEBI).

(11).

This rule shall not apply to an unlisted public company which is

(a). A Nidhi company.

(b). A Government company.

(c). A wholly owned subsidiary.

To Access Form PAS-6: https://ca2013.com/wp-content/uploads/2023/01/PAS-6.pdf

Please note that this form should be filed electronically on the MCA website.

Rule 9B. Issue of securities in dematerialised form by private companies

(1).

Every private company, except a small company, must comply with the following within the period specified in (2):

(a). It must issue all securities only in dematerialised (demat) form and no physical certificates can be issued.

(b). It must facilitate the dematerialisation of all its existing securities.

These requirements must be followed in accordance with the Depositories Act, 1996 and the regulations made under it.

(2).

A private company that is not a small company as on the last day of a financial year ending on or after 31st March 2023, based on its audited financial statements, must comply with this rule within 18 months from the end of that financial year.

A Producer Company falling under this sub-rule gets five years from the end of that financial year to comply.

A private company (not being a Producer Company) which is not a small company as on 31st March 2023, may comply with this rule on or before 30th June 2025.

This essentially states that:

Normal private companies (not small companies): 18 months to comply.

Producer companies: 5 years to comply.

Private companies (other than Producer Companies) not small as on 31-03-2023 then the time extended to 30-06-2025.

(3).

Any private company covered under (2), once it reaches the date by which it must comply with this rule, must follow an additional requirement when issuing or altering securities.

If such a company plans to:

Issue any securities.

Buy back securities.

Issue bonus shares.

Make a rights offer then :

It must first ensure that the entire holding of securities belonging to its:

Promoters.

Directors.

Key managerial personnel (KMPs) has been fully dematerialised.

The dematerialisation must comply with the Depositories Act, 1996 and the regulations made under it.

(4).

For every security holder of a private company covered under (2):

(a). If the holder wants to transfer any of their securities on or after the company’s compliance date, they must first dematerialise those securities before transferring them.

(b). If the holder wants to subscribe to any new securities of that company on or after the compliance date, they must ensure that all their existing securities are already in dematerialised form before subscribing.

(5).

The provisions of (4) to (10) of rule 9A shall, mutatis mutandis, apply to the dematerialisation of securities under this rule.

(6).

The provisions of this rule shall not apply in case of a Government company.

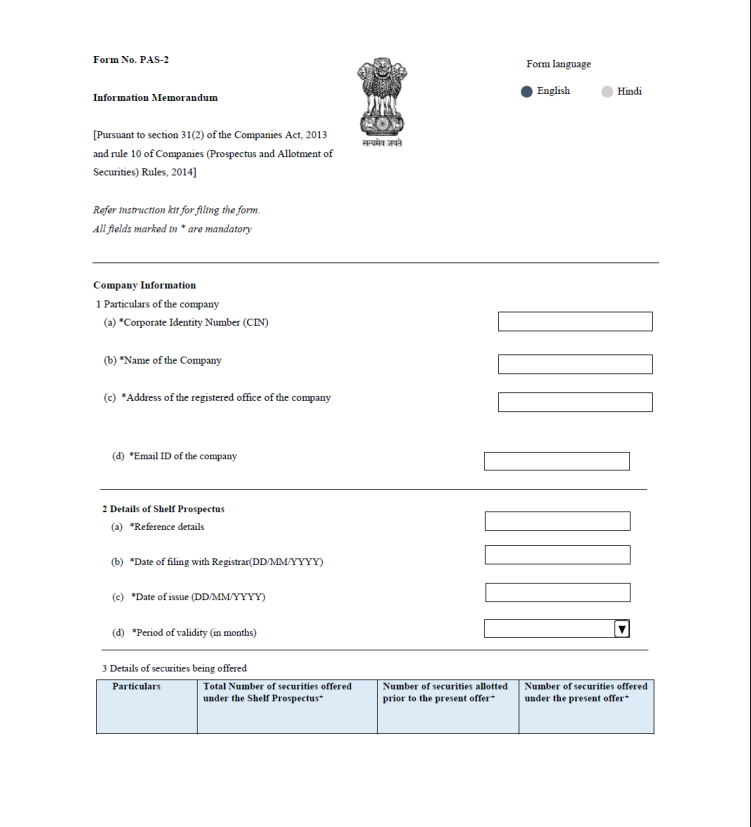

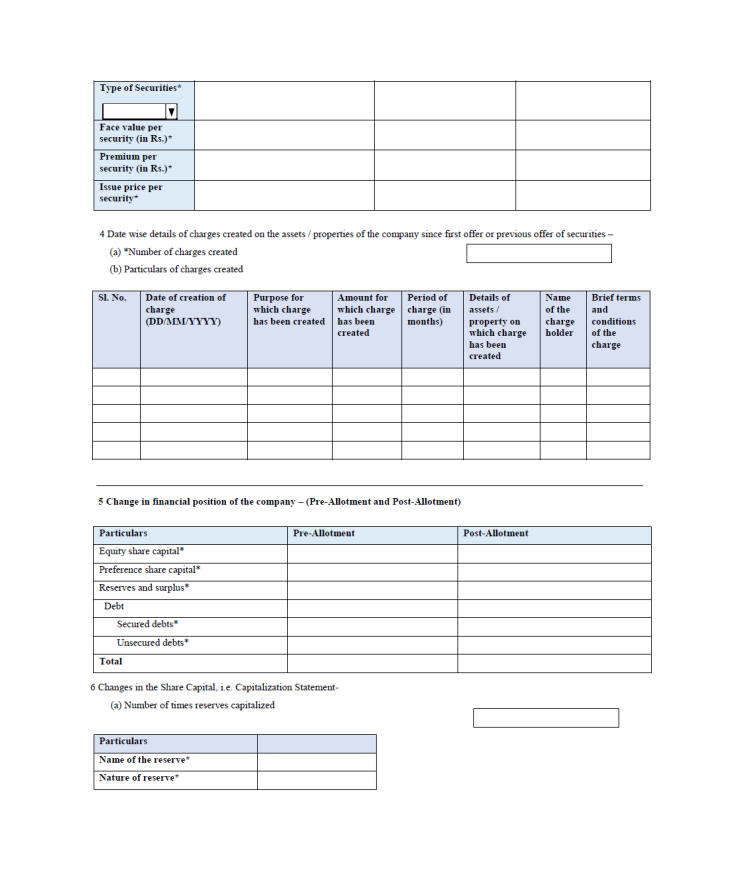

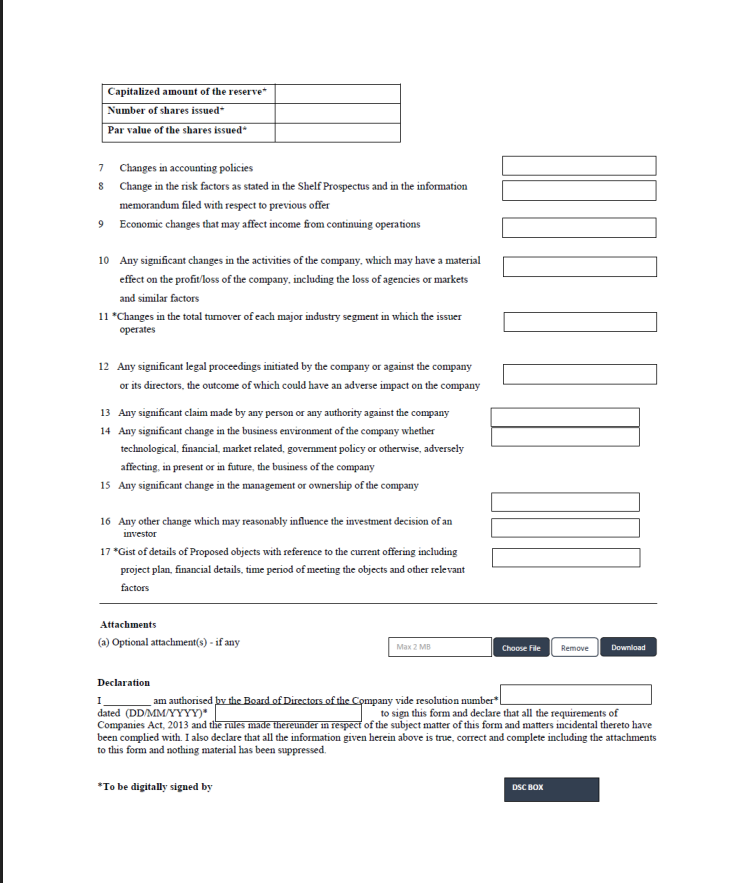

Rule 10.Shelf prospectus and Information Memorandum.

The information memorandum must be prepared in Form PAS-2.

It must be filed with the Registrar of Companies (ROC).

The filing must include the prescribed fee under the Companies (Registration Offices and Fees) Rules, 2014.

The filing must be done within one month before the company issues a second or subsequent offer of securities under a shelf prospectus.

To Access Form PAS -2: https://ca2013.com/wp-content/uploads/2023/01/PAS-2.pdf

Please note that this form should be filed electronically on the MCA website.

Rule 11. Refund of Application Money.

(1).

If the minimum subscription is not achieved and the application money for that minimum amount is not received within the specified period, the company must refund the application money.

This refund must be made within 15 days from the closure of the issue.

If the refund is not made within those 15 days, the directors who are officers in default become personally responsible.

Their liability is joint and several, meaning each one can be made to repay the full amount.

They must repay the pending application money with interest at 15% per annum.

(2).

The application money to be refunded shall be credited only to the bank account from which the subscription was remitted.

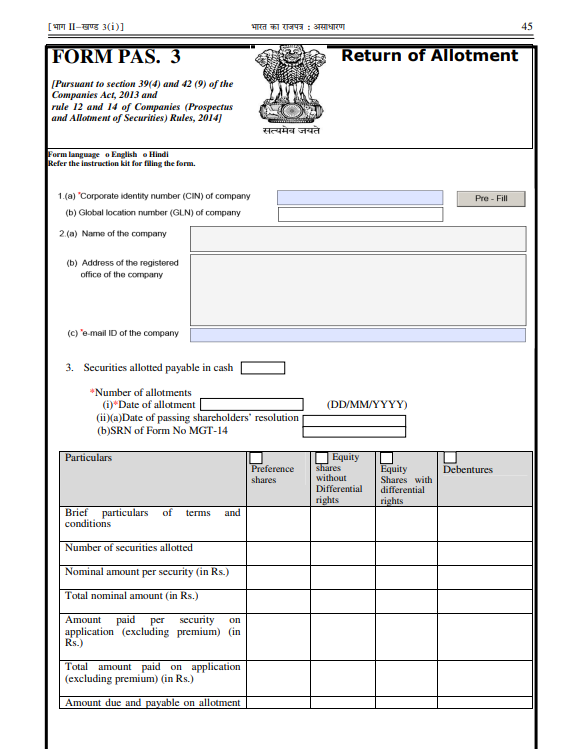

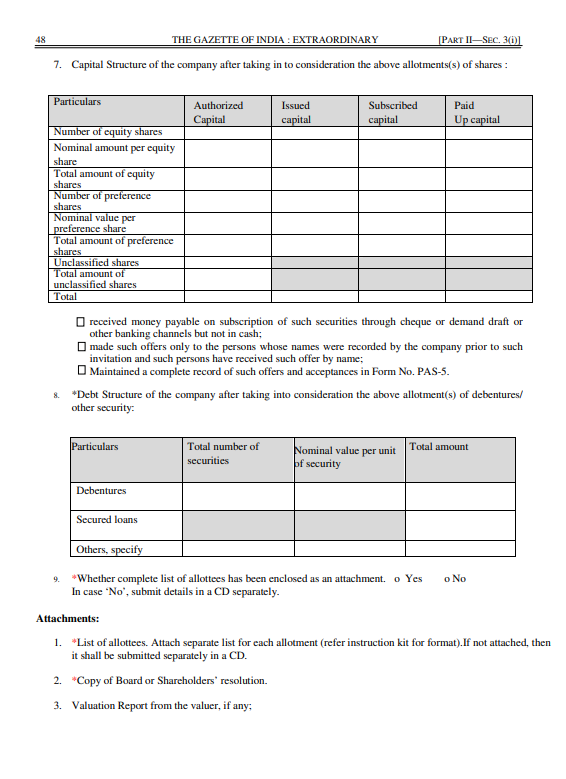

Rule 12. Return of Allotment.

(1).

When a company with share capital allots any securities, it must file a return of allotment.

This filing must be done within 30 days of making the allotment.

The return of allotment must be submitted in Form PAS-3.

The filing must be made with the Registrar of Companies.

The applicable fee must be paid as per the Companies (Registration Offices and Fees) Rules, 2014.

(2).

Form PAS-3 must include an attached list of allottees.

This list must contain:

Name of each allottee

Address

Occupation (if any)

Number of securities allotted to each person

The signatory of Form PAS-3 must certify that this list is complete and correct according to the company’s records.

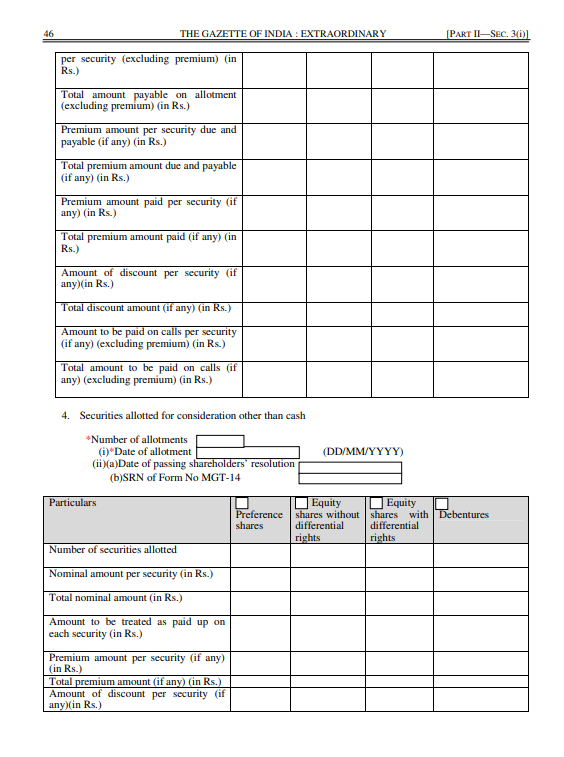

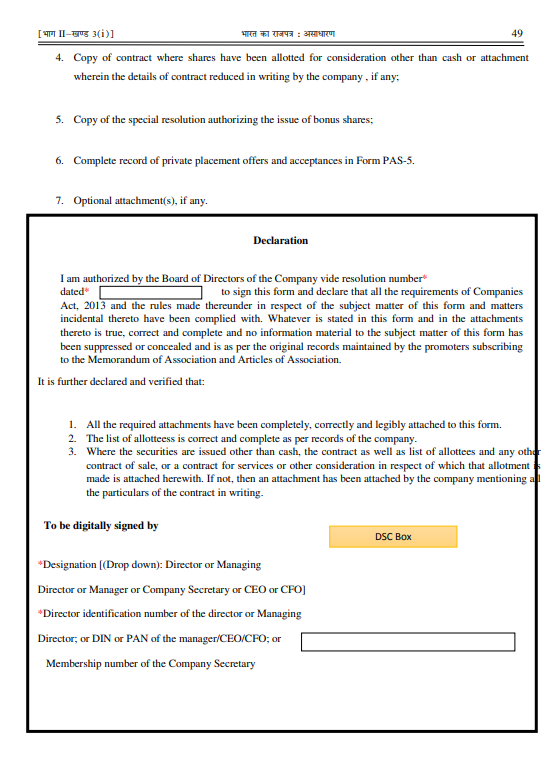

(3).

When securities (other than bonus shares) are allotted for consideration other than cash, additional documents must be filed with Form PAS-3.

A duly stamped copy of the contract under which such securities were allotted must be attached.

If the allotment relates to a property or asset, the relevant contract of sale must also be attached.

If the consideration is services or any other non-cash consideration, the related contract or agreement must be attached as well.

These documents collectively serve as proof of the non-cash consideration for the allotment.

(4).

If the contract for non-cash consideration is not in writing, the company must still submit details of it.

The company must file complete particulars of the contract along with Form PAS-3.

These particulars must be stamped with the same stamp duty that would have applied if the contract had been in writing.

Once filed, these particulars will be treated as an instrument under the Indian Stamp Act, 1899.

The Registrar may insist, as a condition for accepting the filing, that the stamp duty be adjudicated under Section 31 of the Indian Stamp Act, 1899.

(5).

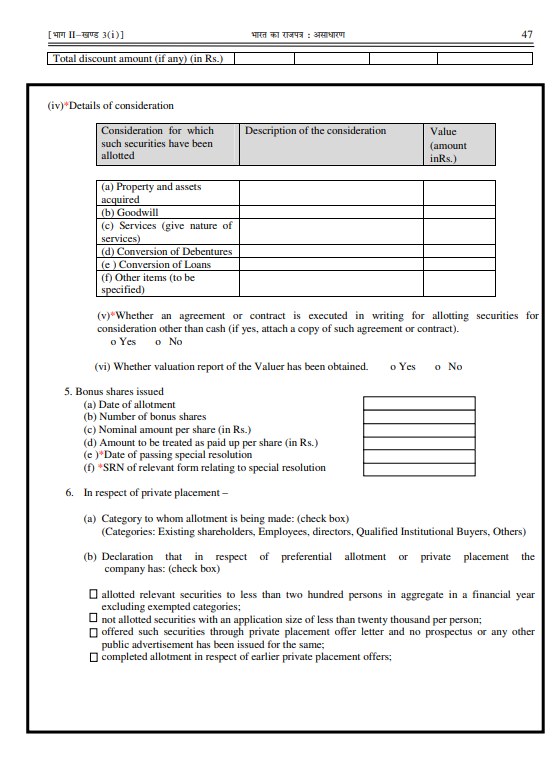

When securities are allotted for non-cash consideration, a registered valuer’s report must also be filed.

This report must state the valuation of the consideration being received by the company.

The valuer’s report must be attached along with the contract submitted under (3) & (4).

(6). Omitted

(7).

When a company issues shares under Section 62(1)(c) (Preferential allotment), it must attach a valuation report.

This requirement applies only to a non-listed company.

In such cases, the company must attach to Form PAS-3 the valuation report of a registered valuer.

This valuation report supports the price at which the preferential issue has been made

Explanation:

Section 247(1) of the Companies Act (relating to registered valuers) is not yet notified, and the qualifications/experience criteria for valuers are still pending.

Until these provisions are officially notified, valuation of stocks, shares, debentures, securities and similar assets must be done by specific independent professionals.

The valuation can be carried out by either:

An independent merchant banker registered with SEBI.

An independent chartered accountant in practice with at least 10 years of experience.

These professionals serve as the temporary authorised valuers until the rules under Section 247 fully come into force.

Note: Section 247(1) is notified and is in effect now.

To Access Form PAS - 3: https://ca2013.com/wp-content/uploads/2015/07/pas-3.pdf

Please note that this form should be filed electronically on the MCA website

Rule 13. Payment of commission.

A company is allowed to pay a commission to any person for getting subscriptions or securing subscribers to its securities.

It does not matter whether the arrangement is absolute or conditional.

But the commission is allowed only if certain conditions are met:

(a) The company’s Articles of Association must authorise payment of such commission.

(b) The commission may be paid from the issue proceeds, from the company’s profits, or a combination of both.

(c) The maximum commission permitted is:

For shares: Up to 5% of the issue price, or the rate allowed in the Articles, whichever is lower.

For debentures: Up to 2.5% of the issue price, or the rate allowed in the Articles, whichever is lower.

(d) The company’s prospectus must disclose the following details:

The name(s) of the underwriters.

The rate and the amount of commission payable to each underwriter.

The number of securities the underwriter has agreed to underwrite or subscribe, whether absolutely or conditionally.

(e).

A company can pay commission only for those securities that are actually offered to the public for subscription.

If the company issues securities privately, or on a rights basis, or in any manner not involving a public offer, then no underwriting commission can be paid for those securities.

(f).

Whenever a company issues a prospectus, and a commission is being paid for getting subscriptions or underwriting the issue, the company must submit a copy of that commission contract to the Registrar of Companies.

This filing must be done at the same time the prospectus is submitted for registration.

This ensures transparency and allows the ROC to verify that the commission arrangements comply with the law.

Underwriter:

A person (called an underwriter) agrees to take up the securities that the public does not subscribe to.

When a company issues shares or debentures to the public, there is a risk that the public may not buy all of them.

An underwriter steps in and guarantees that the company will receive a minimum amount of subscription.

If the public does not subscribe fully, the underwriter buys the remaining unsubscribed securities.

Rule 14. Private Placement.

(1).

A company cannot make a private placement offer (under Section 42(2) or 42(3)) unless shareholders have approved the proposal by a special resolution.

A separate special resolution is required for each private placement offer or invitation.

When seeking shareholder approval, the explanatory statement to the notice must include specific mandatory disclosures.

These Mandatory Disclosures must be included in the explanatory statement that accompanies the notice of the special resolution:

(a) Particulars of the offer, including the date on which the Board passed the resolution approving the private placement.

(b) The type of securities being offered and the price at which they are being offered.

(c) The basis or justification for the price, including any premium.

(d) The name and address of the valuer who carried out the valuation of securities.

(e) The total amount the company plans to raise through the private placement.

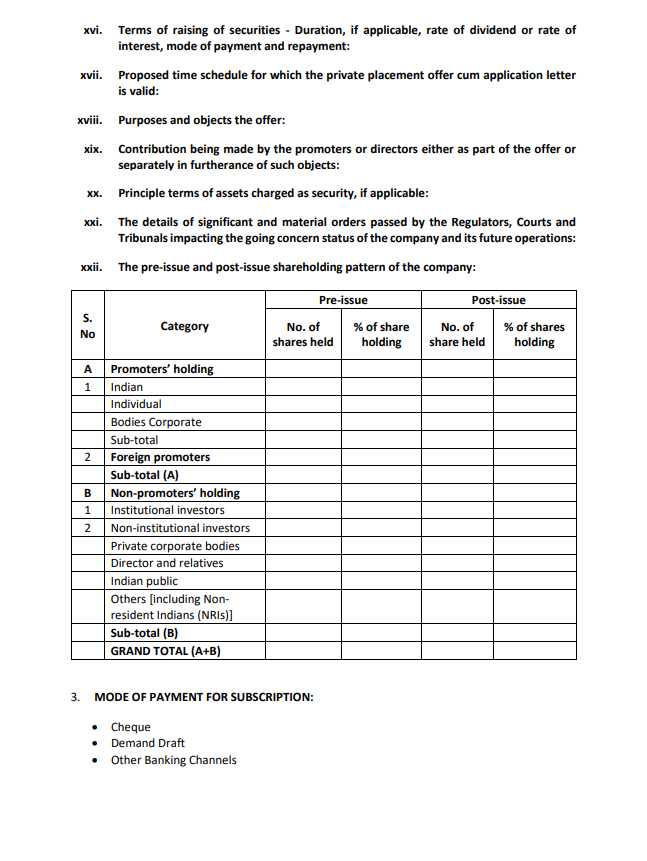

(f) The material terms relating to the issue, including:

Proposed time schedule.

Purpose/object of the offer.

Details of any contribution by promoters or directors, whether as part of the offer or separately.

Key terms of any assets to be charged as security (if applicable).

The requirement of a special resolution does not apply when the company is making a private placement of non-convertible debentures (NCDs).

This relaxation applies only if the amount the company proposes to raise does not exceed the borrowing limit specified in Section 180(1)(c).

If the proposed NCD issue stays within that Section 180(1)(c) limit, then:

A Board Resolution passed under Section 179(3)(c) is enough.

A special resolution of shareholders is not required.

If a company plans to raise more than the Section 180 limit through private placement of NCDs, then normally a special resolution would be required for each such offer.

However, the company does not need to pass a separate special resolution for every issue of NCDs during the year.

Instead, it is enough if the company passes one special resolution in a year, and that single resolution will cover all NCD private placement offers made during that financial year.

When a company makes a private placement to Qualified Institutional Buyers (QIBs), it normally requires shareholder approval by special resolution.

The company does not need to pass a separate special resolution for each offer made to QIBs.

Instead, the company may pass one special resolution in a year, and that single resolution will cover all private placement allotments made to QIBs during that year.

A company cannot make a private placement offer or invitation of securities to any body corporate that is:

Incorporated in a country sharing a land border with India.

To any national of such a country.

Countries sharing a land border with India include: China, Pakistan, Bangladesh, Nepal, Bhutan, Myanmar, Afghanistan.

Such an investment is allowed only if the body corporate or the national has already obtained Government approval under the Foreign Exchange Management (Non-Debt Instruments) Rules, 2019 (FDI rules).

The company must attach a copy of this Government approval with the private placement offer-cum-application letter.

(2).

Under Section 42(2), a company cannot make a private placement offer to more than 200 persons in total in a financial year.

This limit of 200 persons applies per financial year.

Exceptions to the 200-person limit

Offers or invitations made to the following are NOT counted in the 200-person limit:

Qualified Institutional Buyers (QIBs).

Employees of the company under an ESOP scheme issued under Section 62(1)(b).

Explanation:

The 200-person limit is calculated separately for each kind of security.

This means the following are independent limits:

Up to 200 persons for equity shares

Up to 200 persons for preference shares

Up to 200 persons for debentures

So, in a single financial year, a company may legally make private placement offers to:

200 persons for equity.

200 persons for preference shares.

200 persons for debentures without violating the rule.

(3).

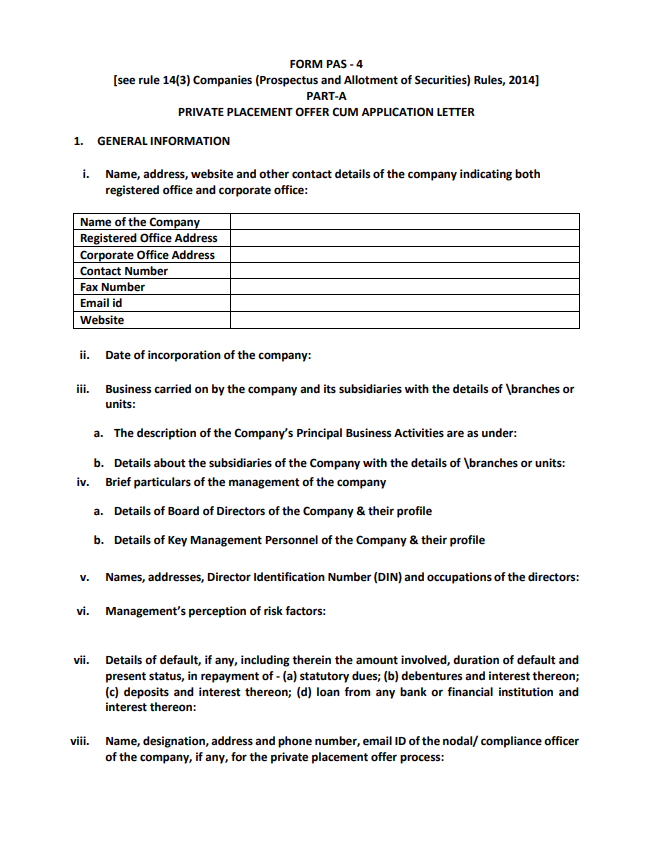

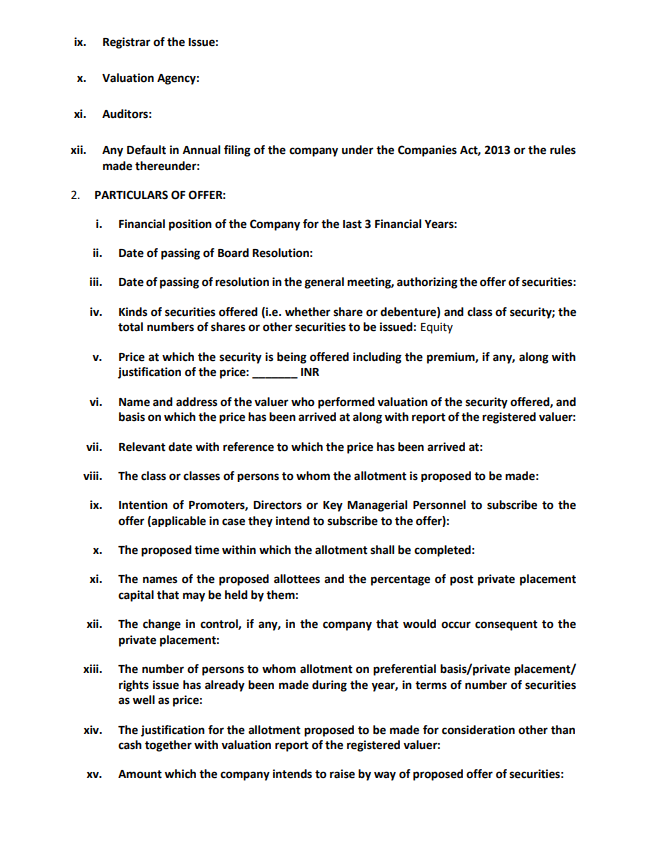

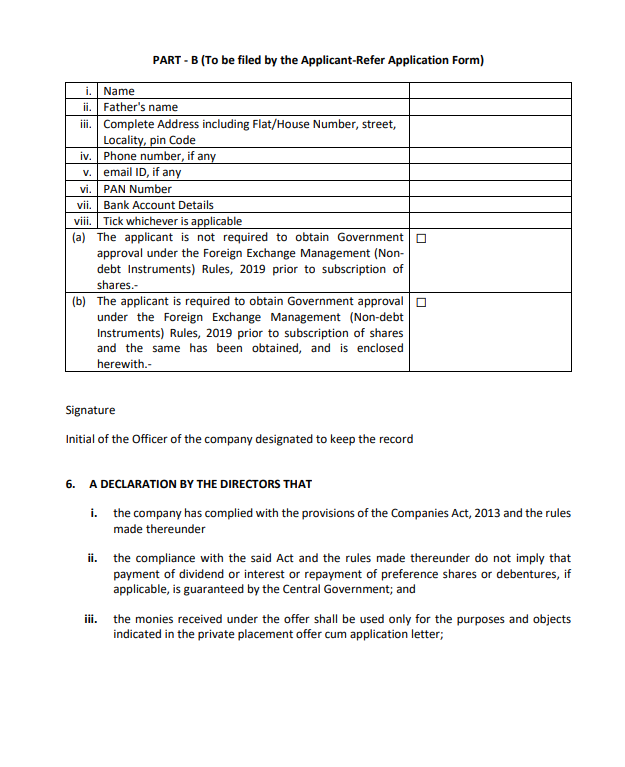

The private placement offer-cum-application letter must be in Form PAS-4.

The form must be serially numbered.

It must be specifically addressed to the individual person to whom the offer is being made.

It must be sent only to that person, either:

In physical writing.

In electronic mode.

The sending of PAS-4 must happen within 30 days of recording that person’s name in the company’s records under Section 42(3).

Only the person to whom the PAS-4 is addressed is allowed to apply.

No other person is permitted to use that application form.

If anyone else applies using that form, the application is treated as invalid.

(4).

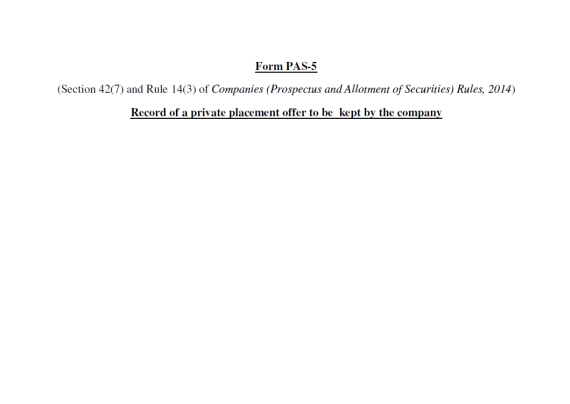

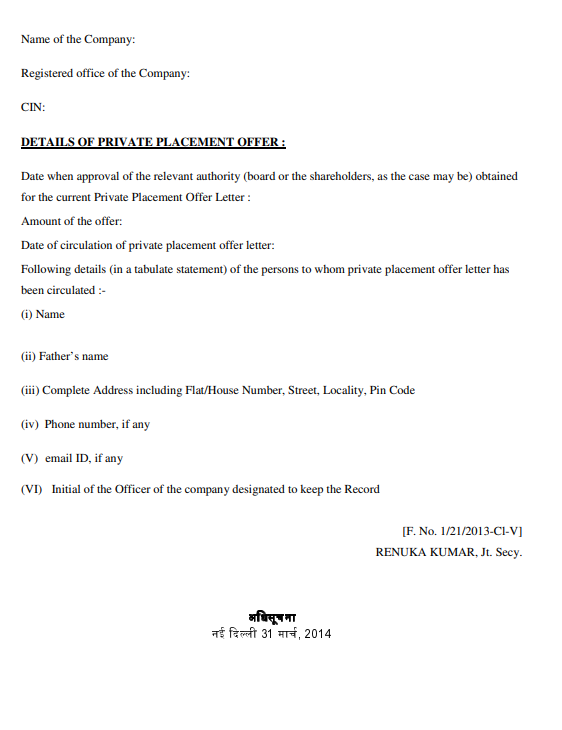

The company shall maintain a complete record of private placement offers in Form PAS-5.

(5).

When a person subscribes to securities under private placement, the subscription money must be paid from that subscriber’s own bank account.

The company must maintain a record of the bank account from which the subscription money was received.

If the securities are to be held jointly, the subscription money must be paid only from the bank account of the first named applicant.

It cannot come from the account of any other joint holder.

This entire rule does not apply when shares are issued for consideration other than cash.

In such cases, since no money is paid, there is no requirement relating to bank accounts.

(6).

When securities are allotted under Section 42 (private placement), the company must file a return of allotment with the Registrar.

This return must be filed in Form PAS-3.

Filing must be completed within 15 days of the date of allotment.

The prescribed fee under the Companies (Registration Offices and Fees) Rules, 2014 must be paid.

A full list of all allottees must be attached to PAS-3.

This list should include:

(i) The allottee’s:

Full name

Address

Permanent Account Number (PAN)

Email ID

(ii) The class of security allotted (equity, preference, debenture, etc.).

(iii) The date of allotment of the securities.

(iv) The number of securities allotted, the nominal value, and the amount actually paid on those securities.

(v) If securities were issued for consideration other than cash, full particulars of the consideration received must be stated.

(7).

This proviso creates an exemption for certain regulated financial institutions.

The 200-person limit does NOT apply to:

Non-Banking Financial Companies (NBFCs) registered with the Reserve Bank of India (RBI) under the RBI Act, 1934.

Housing Finance Companies (HFCs) registered with the National Housing Bank (NHB) under the NHB Act, 1987.

The exception only applies if they are complying with the private placement regulations issued by their respective regulators (RBI or NHB).

If RBI or NHB has NOT prescribed any regulations on private placement:

The NBFC or HFC must follow the 200 person limit under (2) of the Companies Act rules.

(8).

A company can issue the private placement offer-cum-application letter (Form PAS-4) only after the relevant approval resolution has been filed with the Registrar of Companies (ROC).

The Relevant Resolution means:

Special resolution (where required).

Board resolution.

For private companies, it is mandatory to file with the ROC:

A copy of the Board resolution.

A copy of the special resolution, passed under Section 179(3)(c).

Note:

Form PAS-4 is mandatory for private placements and preferential allotments, but it is no longer required to be filed with the ROC.

Instead, companies must issue it to investors and keep it as part of their internal records.

Form PAS-5, which is the record of persons to whom the offer letter is issued, is also maintained internally but is not required to be filed with the ROC

To Access PAS - 4: https://ca2013.com/wp-content/uploads/2022/05/PAS-4-Subsituted-w.e.f.-05.05.2022.pdf

To Access Form PAS-5: https://ca2013.com/returns/pas-5/