Significant Beneficial Owners Rules

Rule 2: Definitions

(1).

In these rules, unless the context otherwise requires:

(a).

Act means the Companies Act , 2013.

(b).

Control means control as defined in clause (27) of section 2 of the Act.

It means having the power to influence how the company is run, directly or indirectly.

This power may come from shareholding, management rights, shareholder agreements, or voting arrangements.

The power might be the right to appoint a majority of directors, or the ability to control management or policy decisions, whether exercised:

Directly or indirectly.

By virtue of shareholding, management rights.

Through agreements or other means.

(c).

Form means the form specified in Annexure to these rules.

(d).

Majority Stake.

Majority stake refers to a situation where a person or entity has control or dominant ownership in a body corporate.

A majority stake exists if any one of the following conditions is satisfied.

Holding more than 50% of the equity share capital of the body corporate.

Holding more than 50% of the voting rights in the body corporate.

Having the right to receive or participate in more than 50% of the distributable dividend or any other distribution made by the body corporate.

(e).

Partnership Entity.

Partnership Entity means a partnership firm registered under the Indian Partnership Act, 1932.

It could also be limited liability partnership registered under the Limited Liability Partnership Act, 2008.

(f).

Reporting company means a company as defined in clause (20) of section 2 of the Act.

A reporting company is a company or legal entity that is required by law to disclose specified information to a regulatory authority.

It must file reports on its ownership, financials, or compliance as mandated under the applicable statutes.

This company is required to comply with the requirements of section 90 of the Act.

(g).

Section means a Section of the Companies Act.

(h).

Significant Beneficial Owner

A significant beneficial owner is an individual who, whether acting alone, or together with others, or through one or more persons or through a trusts:

Holds certain rights or entitlements in a reporting company.

The individual will be treated as an SBO if he possesses any one of the following:

(i). If the individual holds 10% or more of the shares indirectly, or 10% or more when combined with their direct shareholding.

(ii). If the individual holds 10% or more of voting rights indirectly, or 10% or more when combined with direct voting rights.

(iii). If the individual is entitled to 10% or more of dividends or other distributions in a financial year, Either indirectly, or indirectly plus directly.

(iv). A person who has the right to exercise, or actually exercises significant influence or control in any manner other than through direct shareholdings alone.

Explanation I:

When checking whether an individual qualifies as a Significant Beneficial Owner (SBO):

An individual must hold a right or entitlement indirectly under sub-clauses (i), (ii), or (iii) of the SBO definition.

If the individual does not hold any such indirect right or entitlement, then he shall not be treated as a Significant Beneficial Owner.

Explanation 2:

If the individual directly holds shares, voting rights, or rights to receive distributions in his own name, he is treated as holding the right directly.

Explanation 3:

For this clause, an individual is considered to hold a right or entitlement indirectly in the reporting company if he satisfies any of the following in respect of a member of the reporting company:

(i). Where the member is a body corporate (Indian or foreign), other than an LLP, and the individual:

(a). Holds majority stake in that member.

(b). Holds majority stake in the ultimate holding company (Indian or foreign) of that member.

(ii). Where the member is a Hindu Undivided Family (HUF) (through karta), and the individual is the karta of the HUF.

(iii). Where the member is a partnership entity (directly or through a partner), and the individual:

(a). Is a partner.

(b). Holds majority stake in a body corporate which is a partner of the partnership entity.

(c). Holds majority stake in the ultimate holding company of that body corporate which is a partner of the partnership entity.

(iv). Where the member is a trust (through trustee), and the individual:

(a) Is a trustee in case of a discretionary trust or a charitable trust.

(b) Is a beneficiary in case of a specific trust.

(c). Is the author or settlor in case of a revocable trust.

(v) Where the member is:

(a). A pooled investment vehicle.

(b). An entity controlled by the pooled investment vehicle,

Such vehicle is based in a member State of the Financial Action Task Force (FATF) on Money Laundering.

The vehicle’s securities regulator is a member of IOSCO, and the individual in relation to that pooled investment vehicle:

(A). is a general partner.

(B). Is an investment manager.

(C). is a Chief Executive Officer where the investment manager is a body corporate or a partnership entity.

Explanation IV:

The member of the reporting company may be:

(i). A pooled investment vehicle.

(ii). An entity controlled by such a vehicle.

If this pooled investment vehicle is based in a country that does not meet the FATF/IOSCO conditions mentioned in clause (v) of Explanation III, then:

The Company cannot use the special rule for pooled investment vehicles.

Instead, it must identify the indirect Significant Beneficial Owner by applying the regular rules used for body corporates, HUFs, partnerships, or trust.

Explanation V:

If one / many individual’s acting through another person or through a trust, have a common intent or purpose, they are treated as acting together.

This common intent or purpose must relate to exercising rights or entitlements, or exercising control or significant influence over a reporting company.

The agreement or understanding between them may be formal or informal.

When such a common intent exists, all those individuals re deemed to be acting together for SBO determination.

They would still be considered as acting together even if they are acting directly or through another person or trust.

Explanation VI:

The following instruments are to be treated as shares:

Global Depository Receipts (GDRs).

Compulsorily Convertible Preference Shares (CCPS).

Compulsorily Convertible Debentures (CCDs).

Treating these instruments as shares means they are included when calculating ownership, voting rights, or entitlements for identifying a Significant Beneficial Owner (SBO).

(i).

Significant Influence.

Significant influence refers to the power to participate in a company’s financial and operating policy decisions.

This participation can be direct or indirect.

However, it does NOT amount to control over those decisions.

It also does not amount to joint control.

(2).

If any term or expression appears in these Rules but is not defined within these Rules themselves, then its meaning must be taken from:

The Companies Act, 2013.

The Companies (Specification of Definitions Details) Rules, 2014, whichever of these laws contains the definition.

Rule 2A. Duty of the reporting company.

(1).

Every reporting company must take necessary steps to determine whether any individual is a Significant Beneficial Owner (SBO) in relation to the company.

The SBO must be identified according to the definition given in rule 2(h).

If the company finds that an individual qualifies as an SBO, the company must identify that individual.

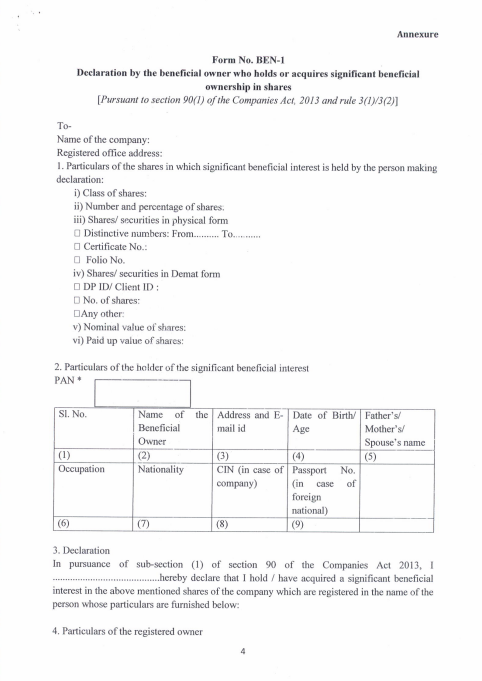

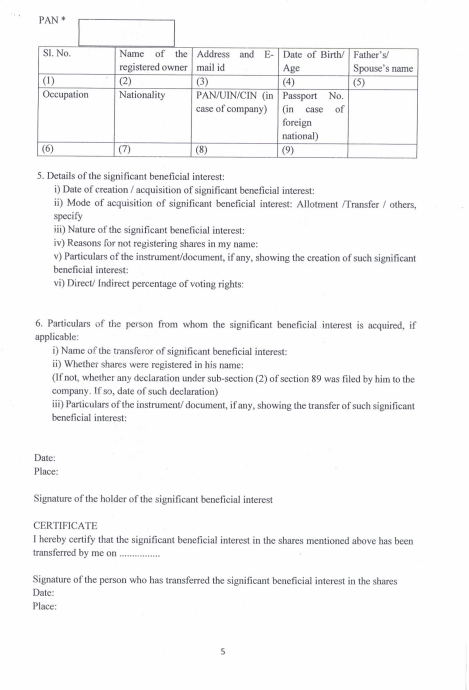

The company must also ensure that such an individual submits a declaration in Form BEN-1.

(2).

In addition to the general duty to identify Significant Beneficial Owners (SBOs), every reporting company has a specific obligation.

This obligation applies when any of its members (other than an individual) hold 10% or more of any of the following:

(a). The shares of the company.

(b). The voting rights in the company.

(c). The right to receive or participate in dividends or any other distribution in a financial year.

In such cases, the reporting company must issue a notice to that member.

The notice must seek information as required under Section 90(5).

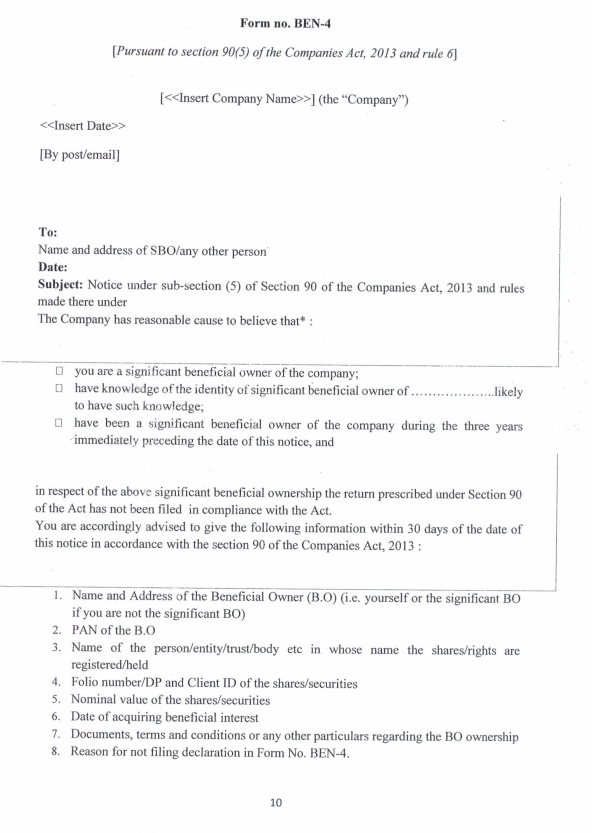

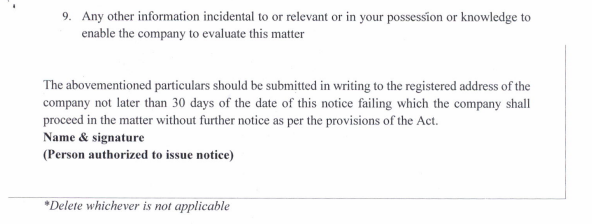

The notice must be issued in Form BEN-4.

Rule 3. Declaration of significant beneficial ownership under section 90.

(1).

When the Companies (Significant Beneficial Owners) Amendment Rules, 2019 came into force, certain obligations were triggered.

Every individual who is a Significant Beneficial Owner (SBO) in a reporting company as on the date of commencement of these Rules must file a declaration.

The declaration must be submitted in Form No. BEN-1.

This declaration must be given to the reporting company (not to the government directly).

The individual (SBO) must file this declaration within 90 days from the date the amended Rules commenced.

(2).

Every individual who subsequently becomes a Significant Beneficial Owner (SBO) in a reporting company must act.

If an individual’s significant beneficial ownership changes after they were already an SBO, that change must be reported.

The individual must file a declaration in Form No. BEN-1 with the reporting company.

The declaration must be filed within thirty days of:

Acquiring significant beneficial ownership.

Any change in their significant beneficial ownership.

Explanation.

When the 2019 SBO Amendment Rules started, the law gave everyone a 90-day buffer period to adjust.

If someone became a Significant Beneficial Owner (SBO) during those first 90 days, the law pretends (deems) that they became an SBO only on the 90th day and not on the actual earlier date.

Similarly, if someone’s SBO details changed (like % holding changed) during those first 90 days, the law treats the change as happening on the 90th day.

Because of this, the 30-day deadline for filing BEN-1 starts after the 90 days are over.

To give everyone extra time to comply during the initial rollout of the amended rules.

To Access Form No. BEN -1: https://ca2013.com/wp-content/uploads/2018/06/BEN-1.pdf

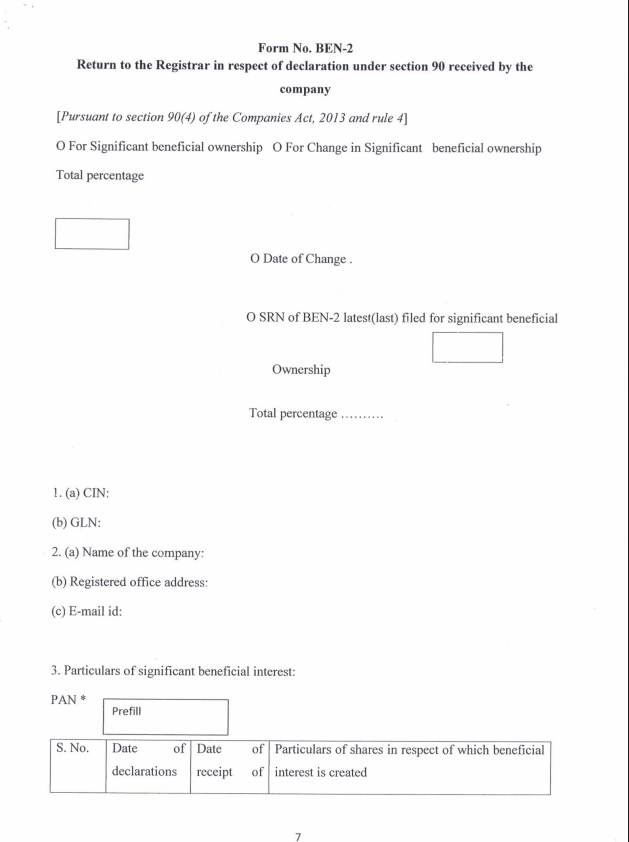

Rule 4. Return of significant beneficial owners in shares.

When the reporting company receives a declaration from an individual under Rule 3, it must take further action.

The company must file a return with the Registrar of Companies (RoC).

This return must be filed in Form BEN-2.

The filing must be done within 30 days from the date the company receives the BEN-1 declaration.

The company must also pay the prescribed fees as per the Companies (Registration Offices and Fees) Rules, 2014.

To Access Form No. BEN -2: https://ca2013.com/wp-content/uploads/2018/06/BEN-2.pdf

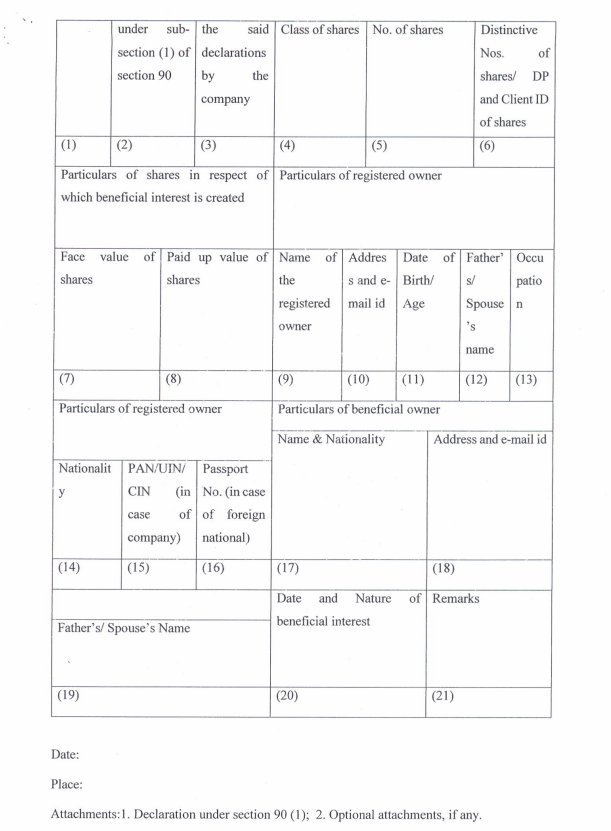

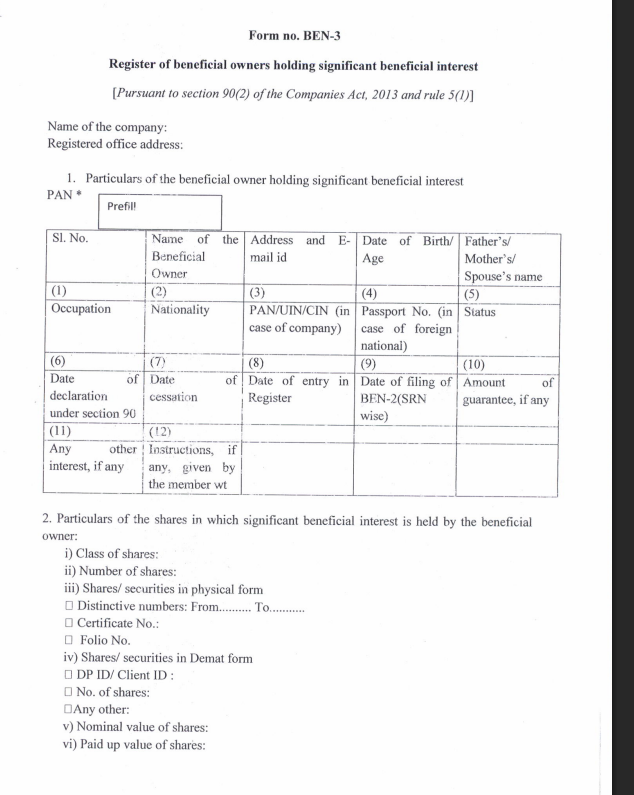

Rule 5. Register of significant beneficial owners.

(1).

The company shall maintain a register of significant beneficial owners in Form No. BEN-3.

(2).

The register must be open for inspection during business hours.

Inspection must be allowed for a reasonable period of at least two hours on every working day.

The specific time for inspection is to be decided by the Board of Directors.

Any member of the company is allowed to inspect the register.

The company may charge a fee for inspection, but the fee cannot exceed ₹50 per inspection.

The fee amount must be specified by the company.

To Access Form No. Ben -3: https://ca2013.com/wp-content/uploads/2018/06/BEN-3.pdf

Rule 6. Notice seeking information about significant beneficial owners

A company is required to seek information about significant beneficial ownership under Section 90(5) of the Companies Act.

For this purpose, the company must issue a notice to the concerned person.

The notice must be given in Form No. BEN-4.

This notice asks the person to provide necessary details regarding their significant beneficial ownership.

Rule 7. Application to the Tribunal

The reporting company must apply to the Tribunal in the situations described below.

An application is required when a person does not provide the information asked for in Form BEN-4 within the time specified.

An application is also required when the information provided is not satisfactory to the company.

The application is made under Section 90(7) of the Companies Act.

The company requests the Tribunal to order that the shares in question be subjected to restrictions, such as:

Restricting the transfer of interest attached to those shares.

Suspending the right to receive dividends or any other distribution related to those shares.

Suspending voting rights attached to those shares.

Imposing any other restriction on some or all rights associated with those shares.

To Access Form No. BEN -4: https://ca2013.com/wp-content/uploads/2018/06/BEN-4.pdf

Rule 8. Non-Applicability

The Significant Beneficial Ownership (SBO) Rules do not apply to the extent the shares of a reporting company are held by the following:

(a). The authority created under Section 125(5) of the Companies Act. (Investor Protection Fund)

(b) The holding reporting company of the reporting company.

However, the details of such holding reporting company must still be reported in Form BEN-2.

(c) The Central Government, State Government, or any local authority.

(d) Any of the following entities controlled by the Central Government, any State Government, or both:

(i). A reporting company.

(ii). A body corporate.

(iii). Any other entity.

(e) SEBI-registered investment vehicles, such as:

Mutual Funds.

Alternative Investment Funds (AIFs).

Real Estate Investment Trusts (REITs).

Infrastructure Investment Trusts (InvITs).

(f) Investment vehicles regulated by:

The Reserve Bank of India (RBI).

The Insurance Regulatory and Development Authority of India (IRDAI).

The Pension Fund Regulatory and Development Authority (PFRDA).