Definitions

CHAPTER I - PRELIMINARY

Regulation 1. Short-Title and Commencement

1(i).

These regulations may be called the Securities and Exchange Board of India (Buy - Back of Securities) Regulations, 2018.

1(ii).

These regulations shall come into force on the date of their publication in the Official Gazette.

Regulation 2. Definitions

2. (i)

The following definitions apply within these regulations.

They apply unless and until the context requires a different interpretation.

(a). Act

Act means the SEBI Act , 1992.

(b). Associate

Associate includes a person who:

(i). A person who directly or indirectly exercises control over the company, either by self or together with his relatives.

(ii) A person whose employee, officer, or director is also: A director, or An officer, or an employee of the company.

(c). Board

Board means the Securities and Exchange Board of India established under the Section 3 of the SEBI Act , 1992.

(d). Buy-Back-Period

Buyback period means the period between the following two points in time:

The starting point, which is either:

The date of the Board of Directors’ resolution authorising the buyback.

The date of declaration of results of the postal ballot for the special resolution authorising the buyback, as applicable.

The ending point, which is the date on which payment of consideration is made to the shareholders who have accepted the buyback offer.

Example:

A company’s Board of Directors passes a resolution on 1 March 2026 approving the buyback of its shares.

The company completes the buyback process and pays the shareholders who accepted the buyback offer on 30 April 2026.

Buyback Period:

The period from 1 March 2026 to 30 April 2026 will be the buyback period.

If a special resolution is used:

Shareholders approve the buyback through a special resolution via postal ballot on 10 June 2026.

The company pays the shareholders who tendered shares on 20 July 2026.

Buyback Period:

The period from 10 June 2026 to 20 July 2026 is the buyback period.

(e). Control

Control has the same meaning as the term defined in 2(1)(e), SEBI (Substantial Acquisition of Shares and Takeovers) Regulations, 2011.

In accordance with Section 2(1)(e) of the SEBI , SAST Regulations , 2011:

Control includes the following rights or powers:

The right to appoint the majority of the directors of a company.

The right to control the management or policy decisions of the company.

Such control may be exercised:

By a person individually.

By persons acting together (in concert).

The control may be exercised directly, or Indirectly.

Control may arise through:

Shareholding in the company.

Management rights.

Shareholders’ agreements.

Voting agreements.

Any other manner through which influence or decision-making power is exercised.

A director or officer of a target company will not automatically be considered to have control over the company.

Mere holding of such position (director/officer) does not amount to control.

For a person to be considered in control, there must be additional powers or rights beyond just the position.

(f). Company

Company means A company as defined under the Companies Act.

The company’s shares or other specified securities are listed on a Stock Exchange.

The company buys or intends to buy its own shares or other specified securities.

Such buyback is carried out in accordance with these regulations.

(g). Companies Act

Companies Act’ means the Companies Act, 2013.

(ga). Frequently Traded Shares

Frequently traded shares shall have the same meaning as assigned to them under the SEBI (Substantial Acquisition of Shares and Takeovers) Regulations, 2011.

Section 2(1)(j) of the Frequently Traded Shares of SEBI (SAST) Regulations , 2011 states that:

Frequently traded shares means shares of a target company where the following conditions are satisfied:

The traded turnover of the shares on any stock exchange is considered.

The turnover is calculated for the twelve calendar months preceding the calendar month in which the public announcement is required to be made under these regulations.

The traded turnover during this period must be at least 10% of the total number of shares of that class of the target company.

If the share capital of that particular class of shares changes during this twelve-month period, then:

The weighted average number of total shares of that class will be taken.

This weighted average will represent the total number of shares for the purpose of calculating the 10% traded turnover.

Example:

Suppose XYZ Ltd. has 1,000 equity shares of a particular class listed on a stock exchange.

A public announcement for buyback is required to be made in March 2026.

To check whether the shares are frequently traded, we look at the traded turnover during the 12 months before March 2026.

So this period would be from March 2025 – February 2026.

During this period, assume 120 shares were traded on the stock exchange.

Calculation:

Total shares of that class = 1,000

Shares traded in 12 months = 120

Turnover % = (120 / 1,000) × 100 = 12%

Since the traded turnover is more than 10%, the shares of XYZ Ltd. are considered “frequently traded shares.”

What happens if the Share Capital of that particular class changes during the 12 month period:

Suppose XYZ Ltd. initially has 1,000 equity shares from March 2025 to August 2025 (6 months).

In September 2025, the company issues 500 additional shares.

So from September 2025 to February 2026 (next 6 months), the total shares become 1,500.

Weighted Average is used in these scenarios.

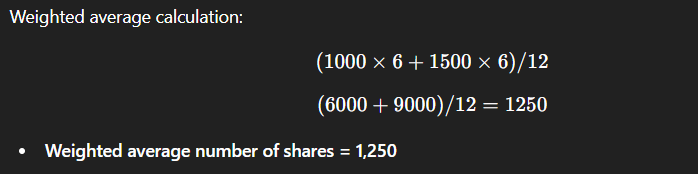

Step 1: Calculate the weighted average number of shares

For the first 6 months the total equity shares were 1,000 shares

For the next 6 months the total equity shares were 1,500 shares

Weighted average calculation for calculation of no. of shares

Step 2: Apply the 10% turnover rule

10% of 1,250 = 125 shares

Step 3: Determine whether shares are frequently traded

If more than 125 shares were traded during the 12-month period then the class of shares would be considered as Frequently traded shares.

If less than 125 shares were traded then the class of shares will not be considered as Frequently traded shares.

(h). Insider

Insider means an insider as defined in 2(1)(g) of SEBI (Prohibition of Insider Trading) Regulations, 2015.

(i). Merchant-Banker

merchant banker’ means a merchant banker as defined

in

clause (cb) of regulation 2 of the Securities and Exchange Board

of India (Merchant Bankers) Regulations, 1992 and re

gistered

under section 12 of the Act

(j). Omitted.

(k). Promoter

promoter’ means promoter as defined in clause (s) of sub

-

regulation (1) of regulation 2 of the Securities and Exchange Board

of India (Substantial Acquisition of Shares and Takeovers)

Regulations, 2011

(l). Registrar

egistrar’ means a registrar to an issue and includes a share

transfer agent

,

registered under section 12 of the Act

(la). Secretarial Auditor

secretarial auditor‘ means an auditor as defined in the Secretarial

Standards

–

I issued by the Institute of Company Secretaries

of

India

(m). Securities

securities’ mean securities as defined in clause (h) of section 2 of the Securities Contracts (Regulation) Act, 1956 (42 of 1956);

(n). Small Shareholder

small shareholder’ means a shareholder of a company, who holds

shares or other specified securities whose

market value, on the

basis of closing price of shares or other specified securities, on the

recognised stock exchange in which highest trading volume in

respect of such securities, as on record date is not more than two

lakh rupee

(n). Specified Securities

specified securities’

includes employees’ stock option or other

securities as may be notified by the Central Government from

time to time

Comment: (n) Is repeated twice in accordance to the recent act downloaded from the SEBI Website. This will be updated as and when the the Regulations in the website are updated. Please note that these regulations are last amended in November 28 , 2024 and we are following the same.

(o). Statutory Auditor

statutory auditor’ means an auditor appointed by a company

under section 139 of the Companies Act

(p). Stock Exchange

stock exchange’ means a stock exchan

ge which has been

granted recognition under section 4 of the Securities Contracts

(Regulation) Act, 1956 (42 of 1956)

(q). Tender Offer

tender offer’ means an offer by a company to buy

-

back its own

shares or other specified securities through a letter of offer from

the h

olders of the shares or other specified securities of the

company

(r). Unpublished Price Sensitive Information

unpublished price sensitive information

’

has the same

meaning as defined in clause (n) of sub

-

regulation (1) of

regulation 2 of the Securities and Exchange Board of India

(Prohibition

of Insider Trading) Regulations, 2015

(s). Working Day

working day’ means any working day of the Board

2(ii).

All other expressions unless defined herein shall have the same meaning

as has been assigned to them under the Act or the Securities Contracts

(Regulation) Act, 1956

, or Companies Act or any statutory modification or Page

5

of

51

re

-

enactment thereof, as the case may be.