Understanding Offers

OFFERS

An offer refers to a formal proposal made by an acquirer to the public shareholders of a listed company.

An offer is made in order to purchase their shares.

This offer is made through a public announcement, followed by a structured process.

This structured process is prescribed under the takeover regulations.

The purpose of an offer is to give public shareholders an exit opportunity when there is:

A substantial acquisition of shares or voting rights.

An acquisition of control over a target company.

Offers under the takeover framework can be of different types, including:

Mandatory open offers (Triggered by crossing thresholds or acquiring control),

Delisting offers (Where the acquirer seeks to remove the company from stock exchanges).

Voluntary open offers (Made even when no mandatory trigger exists, subject to conditions).

Every offer is governed by detailed rules relating to:

Timing.

Pricing.

Disclosures.

Eligibility of the acquirer.

Shareholder protections.

The framework to be followed is as laid down under the SEBI (Substantial Acquisition of Shares and Takeovers) Regulations, 2011.

DELISITING OFFER

A delisting offer is a process through which an acquirer seeks to remove a listed company’s shares from stock exchanges.

It is usually made along with an open offer under the SEBI Takeover Regulations.

When the acquirer plans to gain a large shareholding or control over the company and then remove it from the stock exchange.

A delisting offer allows the acquirer to buy out public shareholders, resulting in the company becoming privately held.

The process is highly regulated to ensure that public shareholders are given a fair exit at a transparent and justifiable price.

The acquirer must declare its intention to delist upfront and follow the procedure laid down under the takeover and delisting regulations.

A delisting offer can succeed only if the prescribed delisting thresholds are met, failing which the company continues to remain listed.

A delisting offer is governed by Regulation 5A of the SEBI (Substantial Acquisition of Shares and Takeovers) Regulations, 2011.

REGULATION 5A OF SUBSTABTIAL ACQUSITION OF SHARES AND TAKEOVER REGULATIONS 2011 , DELISTING OFFER

5A(1). Right to Delist After Making an Open Offer

Notwithstanding anything contained in these regulations and the Delisting Regulations, this provision overrides other conflicting rules.

Where an acquirer makes a public announcement of an open offer, for acquiring shares, voting rights, or control of a target company then:

Such open offer must be made under sub-regulation (1) of regulation 3, regulation 4, or regulation 5.

In such a situation, the acquirer is permitted to seek delisting of the target company.

The delisting must be carried out by making a delisting offer.

Such delisting offer must be made in accordance with the provisions of this regulation.

Upfront Declaration Required for Delisting

If an acquirer intends to delist the target company, this intention must be clearly declared upfront.

The acquirer must declare the intention to delist at the time of making the public announcement of the open offer.

The same intention must also be declared at the time of making the Detailed Public Statement (DPS).

A later or subsequent declaration of the intention to delist is not permitted.

Declaring the intent to delist only after the open offer has already been announced is not sufficient for making a valid delisting offer under this regulation.

Delisting Declaration at DPS Stage in Certain Indirect Acquisitions

Where the open offer arises from an indirect acquisition, and such indirect acquisition is not treated as a deemed direct acquisition under Regulation 5(2) then:

The acquirer is not required to declare the intent to delist at the stage of the public announcement.

In such cases, the acquirer must declare the intention to delist for the first time.

This declaration must be made only in the Detailed Public Statement (DPS).

Explanation 1 : Eligibility conditions for an acquirer making a delisting offer.

For a period of two years prior to the date of the public announcement, the acquirer must not have been:

(i). A promoter, part of the promoter group, or a person in control of the target company.

(ii). Directly or indirectly associated with the promoter or any person in control of the target company.

(iii). A person holding more than 25% of the shares or voting rights in the target company.

Explanation 2: Additional Eligibility Conditions for the Acquirer

The acquirer cannot acquire joint control of the target company.

Such joint control cannot be shared with an existing promoter or person in control of the company.

The objective is to prevent a delisting offer is to create shared or parallel control structures with existing controllers.

5A(2).

When an acquirer makes a delisting offer, certain disclosure obligations must be followed.

These obligations must be complied with in a prescribed manner.

(a) The public announcement, Detailed Public Statement (DPS), and the letter of offer must clearly mention:

the open offer price, determined in accordance with Regulation 8, and

the indicative price for delisting.

Where the open offer arises from an indirect acquisition,

and such indirect acquisition is not treated as a deemed direct acquisition under Regulation 5(2),

the acquirer is required to disclose the open offer price and the indicative delisting price

only at the stage of the Detailed Public Statement (DPS) and in the letter of offer, and not earlier.

The indicative price for delisting must include a suitable premium.

This premium should reflect the price the acquirer is willing to pay to successfully delist the company.

The acquirer must provide full disclosure of the rationale and justification for arriving at the indicative price.

The indicative price is not fixed at the initial stage.

The acquirer is permitted to revise the indicative price upwards.

Such upward revision must be done before the start of the tendering period.

Any revision in the indicative price must be clearly disclosed to the shareholders.

Explanation:

The indicative price for the delisting offer must be determined in accordance with clause (o) of sub-regulation (1) of Regulation 2 of the SEBI Delisting Regulations.

The indicative price cannot be lower than the book value of the company.

The book value must be calculated as per the Explanation to sub-regulation (5) of Regulation 22 of the Delisting Regulations.

(b).

This provision deals with how shareholders are paid, based on the outcome of the delisting offer.

If the response to the offer meets the delisting threshold specified under Regulation 21 of the Delisting Regulations:

(i) all shareholders who have tendered their shares shall be paid the indicative price.

If the delisting threshold is not met:

(ii) all shareholders who have tendered their shares shall be paid the open offer price.

Thus, the price payable to shareholders depends on whether the delisting succeeds or fails.

(3).

A delisting offer is treated as unsuccessful in any of the following situations:

(a) prior shareholders’ approval is not received as required under Regulation 11 of the Delisting Regulations;

(b) prior in-principle approval of the stock exchange is not received under Regulation 12 of the Delisting Regulations; or

(c) the delisting threshold prescribed under Regulation 21 of the Delisting Regulations is not achieved.

When the delisting offer fails for any of the above reasons, the acquirer must act promptly.

Within two working days of such failure, the acquirer must make an announcement.

This announcement must be published in all newspapers in which the Detailed Public Statement (DPS) was published.

After such failure, the acquirer must comply with all applicable provisions of the takeover regulations.

This includes completing the open offer in accordance with the prescribed requirements.

(4).

This provision applies where a competing offer is made under Regulation 20(1) of the takeover regulations.

In such a case, the original acquirer loses the right to delist the target company.

The acquirer is not required to pay interest to shareholders for any delay caused due to the competing offer.

Despite the competing offer, the acquirer must continue to comply with all applicable provisions of the takeover regulations.

The acquirer must also make a public announcement informing shareholders of this position.

Such announcement must be made within two working days from the date of the public announcement of the competing offer.

The announcement must be published in all newspapers in which the Detailed Public Statement (DPS) was published.

(5).

This provision grants a withdrawal right to shareholders.

Shareholders who have tendered their shares in acceptance of the offer under sub-regulation (1) are covered.

Such shareholders are entitled to withdraw the shares they have tendered.

The withdrawal can be made within five working days.

This five-day period is calculated from the date of the announcement made under sub-regulation (3).

(6).

This situation arises when a delisting offer under sub-regulation (1) is unsuccessful.

Even though delisting fails, the acquirer’s shareholding increases as a result of the offer.

After the offer, the acquirer’s shareholding exceeds the maximum permissible non-public shareholding threshold.

Thus, the company remains listed, but the acquirer now holds more than the allowed non-public shareholding limit.

(a).

Where the delisting attempt has failed but the acquirer’s shareholding exceeds the maximum permissible non-public shareholding,

the acquirer is permitted to make another attempt to delist the target company.

This further delisting attempt must be made in accordance with the Delisting Regulations.

The further attempt must be undertaken within twelve months from the date of completion of the open offer.

This option is available only so long as the acquirer continues to exceed the maximum permissible non-public shareholding in the target company.

(b).

A further delisting attempt will be considered successful only if certain conditions are satisfied.

Both conditions must be met simultaneously.

(i) The delisting threshold prescribed under Regulation 21 of the Delisting Regulations must be achieved.

(ii) In addition, the acquirer must acquire 50% of the residual public shareholding.

Only when both these requirements are fulfilled will the further delisting attempt succeed.

(c).

This provision applies if the further delisting attempt also fails.

In such a case, the acquirer is required to take corrective action.

The acquirer must ensure that the target company complies with the minimum public shareholding (MPS) requirement.

This compliance must be in accordance with the Securities Contracts (Regulation) Rules, 1957.

The MPS compliance must be achieved within twelve months.

This twelve-month period is counted from the end of the period mentioned in clause (a).

(d).

This provision deals with the floor price for a further delisting attempt referred to in clause (a).

The floor price for such further attempt cannot be arbitrarily fixed.

It must be the highest among the following three values:

(i) the indicative price offered during the first delisting attempt;

(ii) the floor price determined under the Delisting Regulations as on the relevant date of the subsequent delisting attempt; and

(iii) the book value of the company, calculated using the method specified in the Explanation to clause (a) under sub-regulation (2).

(7).

This provision applies to both the first delisting attempt and any subsequent delisting attempt.

While carrying out the delisting, the acquirer must follow all provisions of the Delisting Regulations.

These provisions apply mutatis mutandis, meaning with necessary changes and adaptations.

An exception is made only where this regulation specifically provides otherwise.

VOLUNTARY OFFER

6(1).

This provision deals with a voluntary open offer.

It applies where an acquirer, together with persons acting in concert (PACs), already holds 25% or more of the voting rights in a target company.

At the same time, such holding must be less than the maximum permissible non-public shareholding.

In this situation, the acquirer is allowed to voluntarily make a public announcement of an open offer.

The voluntary open offer must be made in accordance with the takeover regulations.

After completion of the open offer, the aggregate shareholding of the acquirer and PACs must not exceed the maximum permissible non-public shareholding.

This provision imposes a restriction on making a voluntary open offer.

If an acquirer, or any person acting in concert (PAC) with him, has acquired shares of the target company in the previous 52 weeks,

and such acquisition did not trigger a mandatory open offer,

then the acquirer is not eligible to make a voluntary public announcement of an open offer under this regulation.

This restriction was temporarily relaxed.

The relaxation from this restriction was available up to 31 March 2021.

This provision applies during the offer period of a voluntary open offer.

During this period, the acquirer cannot acquire shares through any other route.

The acquirer is permitted to acquire shares only through the open offer.

Any acquisition outside the open offer during the offer period is prohibited.

6(2).

This provision applies after the completion of a voluntary open offer.

The acquirer and persons acting in concert (PACs) who have made a public announcement under this regulation are covered.

Such acquirer and PACs cannot acquire any further shares of the target company.

This restriction operates for a period of six months after completion of the open offer.

The only exception is where the shares are acquired through another voluntary open offer.

This provision creates an exception to the six-month restriction on further acquisitions.

Even during the restricted period, the acquirer is allowed to make a competing offer.

This is permitted when another person makes an open offer for acquiring shares of the target company.

Thus, the restriction does not prevent the acquirer from participating in a competing bid.

6(3).

This provision clarifies what acquisitions are excluded from the restriction.

Shares received through a bonus issue are not counted for the purpose of the dis-entitlement under this regulation.

Shares received due to a stock split are also not counted for this purpose.

Such acquisitions are ignored because they do not involve any fresh investment or change in control.

6(4).

This provision applies specifically to listed entities on the Innovators Growth Platform (IGP).

For such entities, the usual 25% threshold mentioned in this regulation is substituted.

Wherever the regulation refers to “twenty-five percent”,

it shall be read as “forty-nine percent” in the case of IGP-listed entities.

6A.

This provision overrides all other provisions of the takeover regulations.

A person who is classified as a wilful defaulter is barred from making a public announcement of an open offer.

Such a person is also not permitted to enter into any transaction.

The prohibition applies to any transaction that would trigger an obligation to make a public announcement of an open offer.

The objective is to prevent wilful defaulters from acquiring shares or control of listed companies through the takeover mechanism.

This provision creates an exception to the restriction on wilful defaulters.

A wilful defaulter is not barred from making a competing offer.

Such competing offer must be made in accordance with Regulation 20 of the takeover regulations.

The competing offer can be made only when another person has already made an open offer for acquiring shares of the target company.

6B.

This provision overrides all other provisions of the takeover regulations.

A person who is a fugitive economic offender is completely prohibited from participating in takeovers.

Such a person cannot make a public announcement of an open offer.

He is also not allowed to make a competing offer for acquiring shares of a target company.

Further, he cannot enter into any transaction, whether directly or indirectly,

for acquiring shares, voting rights, or control of a target company.

The restriction is absolute, leaving no exception for fugitive economic offenders under these regulations.

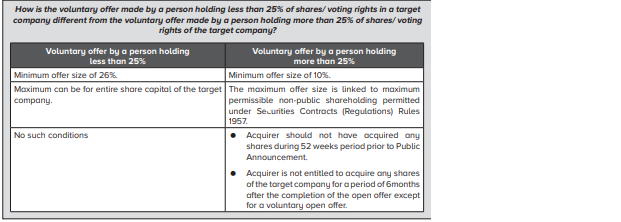

Can a person holding less than 25% of the voting rights/ shares in a target company, make an offer?

Yes, any person holding less than 25% of shares/ voting rights in a target company can make an open offer provided the open offer is for a minimum of 26% of the share capital of the company.

An acquirer and persons acting in concert with him, who have made a public announcement under this regulation to acquire shares of a target company shall not be entitled to acquire any shares of the target company for a period of six months after completion of the open offer except pursuant to another voluntary open offer:

Provided that such restriction shall not prohibit the acquirer from making a competing offer upon any other person making an open offer for acquiring shares of the target company.

What are the restrictions on acquirers making a voluntary open offer?

A voluntary offer cannot be made if the acquirer or PACs with him has acquired any shares of the target company in the 52 weeks prior to the voluntary offer. The acquirer is prohibited from acquiring any shares during the offer period other than those acquired in the open offer. The acquirer is also not entitled to acquire any shares for a period of 6 months, after completion of open offer except pursuant to another voluntary open offer.

Conditional Offer

19(1).

An acquirer is permitted to make an open offer subject to conditions.

One such condition can relate to the minimum level of acceptance of the offer.

This means the acquirer may specify that the open offer will be successful only if a minimum number or percentage of shares are tendered by shareholders.

If the specified minimum acceptance level is not met, the acquirer is not required to complete the acquisition.

This provision applies when an open offer is made pursuant to an agreement.

In such cases, the agreement itself must contain a specific condition.

The condition must state that if the minimum desired level of acceptance of the open offer is not achieved,

the acquirer shall not acquire any shares under the open offer.

In addition, the underlying agreement that triggered the open offer shall automatically stand rescinded.

19(2).

This provision applies when an open offer is made subject to a minimum level of acceptance.

During the offer period, the acquirer and persons acting in concert (PACs) are restricted from acquiring shares through other means.

They cannot acquire any shares of the target company in the market or otherwise during this period.

The only permitted acquisitions during the offer period are:

shares acquired under the open offer, and

shares acquired under the underlying agreement pursuant to which the open offer was made.

Competing Offer

20(1).

Once a public announcement of an open offer for acquiring shares of a target company is made,

any other person, except the acquirer who made the first public announcement,

is permitted to make a competing open offer.

Such competing public announcement must be made within 15 working days.

This 15-day period is counted from the date of the Detailed Public Statement (DPS) made by the first acquirer.’

20(2).

This provision applies to an open offer made by a competing acquirer.

The competing open offer must be for a sufficient number of shares.

When these shares are added to the shares already held by the competing acquirer and persons acting in concert with him,

the total holding must be at least equal to the holding of the first acquirer.

While calculating the holding of the first acquirer, the following are included:

shares already held by the first acquirer and his persons acting in concert,

shares proposed to be acquired under the open offer, and

shares proposed to be acquired under any underlying agreement pursuant to which the open offer was made.

20(3).

This provision overrides all other provisions of the takeover regulations.

An open offer made within the time period specified in sub-regulation (1) is covered by this rule.

Such an open offer shall not be treated as a voluntary open offer under Regulation 6.

As a result, the special conditions and restrictions applicable to voluntary open offers do not apply.

Instead, the open offer will be governed by the general provisions of the takeover regulations, as applicable to that offer.

20(4).

This provision deals with the treatment of multiple open offers for the same target company.

Every open offer made under sub-regulation (1) is covered by this rule.

The open offer first made by the original acquirer is also included.

Both the original open offer and the later open offer(s) are treated as competing offers.

They are therefore governed by the rules applicable to competing offers under the takeover regulations.

20(5).

This provision imposes a time bar on making open offers.

After the expiry of 15 working days referred to in sub-regulation (1),

no person is permitted to make a public announcement of an open offer.

During this period, no person may also enter into any transaction.

The prohibition applies to any transaction that would trigger an obligation to make a public announcement of an open offer.

This restriction continues until the offer period of the open offer comes to an end.

20(6).

This provision deals with conditions attached to competing open offers.

As a general rule, a competing open offer cannot be conditional on a minimum level of acceptances.

An exception is provided where the first open offer itself is conditional on a minimum level of acceptances.

Only in such a case, the competing acquirer is also permitted to make a conditional open offer.

20(7).

This provision imposes a restriction on making fresh open offers or triggering transactions.

No person is permitted to make a public announcement of an open offer,

or to enter into any transaction that would attract an open offer obligation,

until the expiry of the offer period of the existing open offer,

where the open offer is for acquisition of shares pursuant to disinvestment, as provided under Regulation 13(2)(d); or

where the open offer is made pursuant to a relaxation granted by SEBI from strict compliance with Chapter III or Chapter IV, under Regulation 11(2).

20(8).

When there are competing open offers, all such offers must follow the same schedule of activities.

The tendering period for every competing offer must run on identical timelines.

If a new competing offer is made later, the timelines are realigned.

The last date for tendering shares for all competing offers will be revised.

This revised last date will be the last date for tendering shares under the competing offer that was made last.

20(9).

This provision applies when a competing open offer is publicly announced.

An acquirer who had made an earlier competing offer is given a right to respond.

Such acquirer is allowed to revise the terms of his open offer.

Any revision is permitted only if the revised terms are more favourable to the shareholders of the target company.

This provision applies to acquirers making competing open offers.

Such acquirers are permitted to revise the offer price upwards.

The upward revision can be made at any time.

However, the revision must be completed up to one working day before the tendering period begins.

No upward revision of the offer price is permitted once the tendering period has commenced.

20(10).

This provision applies to every competing open offer.

Any variations or changes are allowed only to the extent specifically permitted under this regulation.

Apart from such permitted variations, all other provisions of the takeover regulations

apply fully and equally to every competing offer.