Takeovers

Concept of Takeover and Substantial Acquisition under the Takeover Regulations

The term takeover is not expressly defined under the Takeover Regulations.

Instead of a strict definition, the concept is understood in a functional sense.

A takeover is where an acquirer purchases shares with the intention of acquiring control or management of another company.

This “another company” is known as the target company.

Control does not necessarily mean acquiring 100% of the shares.

It generally refers to the ability to influence:

Key decisions,

Management, or voting outcomes of the target company.

With respect to substantial acquisition:

Regulations 3(1), 3(2), and 4 create a clear, objective framework for determining when a substantial acquisition or takeover occurs.

Regulation 3(1) lays down the first trigger for substantial acquisition.

It provides that an acquirer, together with persons acting in concert, must make a public announcement of an open offer:

If their acquisition entitles them to 25% or more of the voting rights in a target company.

The calculation of this threshold includes existing shareholding plus the proposed acquisition.

Once the 25% voting rights threshold is crossed, the obligation to make an open offer automatically arises.

This obligation arises even if the acquirer does not acquire control over the target company.

Regulation 3(2) addresses the situation of creeping acquisition.

It applies where the acquirer already holds 25% or more voting rights in the target company.

It further requires that the acquirer must hold less than the maximum permissible non-public shareholding.

Under this regulation, the acquirer cannot acquire more than 5% of voting rights in a single financial year without triggering an open offer.

Any acquisition beyond the 5% annual limit results in a mandatory public announcement.

Regulation 4 operates independently of shareholding thresholds.

It mandates an open offer whenever control over the target company is acquired, whether directly or indirectly.

This obligation under Regulation 4 applies regardless of the percentage of shares or voting rights acquired.

Takeover of Listed Companies

Takeovers of companies whose securities are listed on one or more recognised stock exchanges in India are governed by:

The Securities and Exchange Board of India (Substantial Acquisition of Shares and Takeovers) Regulations, 2011.

These regulations lay down the framework for such transactions.

Understanding Acquisition

An acquisition generally involves the purchase of one entity by another.

The purchasing entity is often a financially or strategically stronger company which acquires a smaller or weaker one.

In an acquisition, no new company is created.

The acquired company, also called the target company, is usually absorbed into the acquiring company.

As a result, the target company may lose its independent identity, and its assets, business, and operations become part of the acquiring company.

Advantages of Acquisition

Acquiring an existing business allows the acquiring company to expand quickly.

Acquiring avoids the time, cost, and uncertainty involved in starting a new business from scratch.

The target company is already operational, with established infrastructure, employees, customers, and processes in place.

This enables the acquiring company to focus primarily on integration and strategic growth, rather than initial setup.

Since the objective is to take over control of another business, the acquiring company often offers to purchase shares at a premium price.

The premium represents the difference between the offer price and the current market price of the shares.

Offering a high premium incentivises shareholders of the target company to sell their shares and realise immediate gains.

Through this process, the acquiring company gradually or directly acquires a majority stake, enabling it to take over ownership and control.

OBJECTS OF TAKE-OVERS

1. Cost Reduction and Operational Efficiency

A takeover helps reduce overall costs by eliminating duplication of functions such as administration, finance, logistics, and infrastructure.

By combining resources, companies can achieve savings in overheads and routine working expenses, leading to more efficient operations.

2. Product Development and Technological Synergy

Acquiring companies with compatible products and strong technological or manufacturing capabilities enables faster product development.

The acquirer can leverage its existing marketing channels, dealer networks, and customer base to successfully commercialise these products.

3. Business Diversification and Risk Reduction

Takeovers allow companies to enter new product lines and markets, helping them diversify beyond their traditional core business.

Diversification reduces exposure to industry-specific risks and stabilises long-term business performance.

4. Improved Productivity and Profitability

Unified control after a takeover facilitates better coordination between technical, managerial, and operational teams of both companies.

Joint efforts and shared expertise lead to higher productivity and improved profitability.

5. Shareholder Value and Wealth Creation

Optimal utilisation of the combined assets and resources of both companies enhances earnings potential.

Improved financial performance and strategic positioning ultimately result in increased shareholder value and wealth creation.

6. Economies of Scale

Larger scale operations enable mass production at lower per-unit costs.

Economies of scale improve cost competitiveness and strengthen the company’s position in the market.

7. Access to Capital and Strategic Advantages of Scale

A larger combined entity enjoys better access to capital markets and financing options.

It can expand its consumer base, negotiate better prices for raw materials.

It can invest more in research and development, and maintain a sustained competitive advantage in the industry.

8. Market Expansion and Geographic Growth

Takeovers help companies enter new geographical territories or market segments where they previously had little or no presence.

This expansion strengthens market reach, increases brand visibility, and supports long-term growth objectives.

KINDS OF TAKE OVER

There are 3 types of Take-Overs:

(a). Friendly Take-Over

A friendly takeover is a takeover that takes place with the consent and approval of the target company.

In such a takeover, the management of the acquiring company and the target company mutually agree to the transaction.

The takeover is usually preceded by detailed negotiations between the managements of both companies.

The negotiations are usually regarding:

Price.

Terms.

Control,

Future operations.

The takeover bid is made with the knowledge and support of the target company’s board of directors.

Consent may also be obtained from the majority or all of the shareholders of the target company.

Since the takeover is based on mutual understanding, there is no hostility or resistance from the target company.

The transaction is structured through formal agreements arrived at after negotiations between the two groups.

Because the takeover is completed through mutual negotiations rather than force, it is also referred to as a negotiated takeover.

(b). Hostile Take-Over

A hostile takeover occurs:

When the acquiring company attempts to take control of the target company without the consent or approval of the target company’s management.

In this type of takeover, the acquirer does not negotiate with or seek approval from the board of directors of the target company.

The acquisition strategy is pursued silently and unilaterally, often by directly approaching the shareholders of the target company.

The existing management of the target company opposes or resists the takeover attempt.

Control is usually sought by gradually acquiring a substantial number of shares or voting rights from the open market or through a public offer.

The acquirer bypasses the management and relies on shareholder acceptance to gain majority control.

Such takeovers are often seen as aggressive because they are carried out against the wishes of the existing management.

A hostile takeover may lead to management changes once the acquirer gains control of the target company.

(c). Bail-out Take Over

A bailout takeover refers to the acquisition of a financially weak or sick company by a financially sound and profit-earning company.

The primary objective of such a takeover is to rescue or revive the sick company from financial distress, insolvency, or potential closure.

The acquiring company steps in to bail out the struggling company by providing financial support, managerial expertise, and operational stability.

For the profit-making company, a bailout takeover presents several strategic advantages despite the target’s poor financial health.

One major advantage is the highly attractive acquisition price, since the sick company’s valuation is usually low.

Creditors of the sick company, particularly banks and financial institutions, are often willing to settle at reduced values to recover their dues.

Since these creditors usually hold a charge over the industrial assets, they prefer a takeover that allows partial or structured recovery.

The idea is to recover as much as possible rather than going under a complete loss.

The acquiring company may gain access to valuable assets, infrastructure, licenses, or market presence at a relatively low cost.

If successfully revived, the sick company can later contribute to the profitability and growth of the acquiring company.

LEGAL FRAMEWORK FOR TAKEOVERS UNDER THE COMPANIES ACT 2013 & SEBI TAKEOVER REGULATIONS

Section 186 of the Companies Act , 2013

Under the Companies Act, 2013, the acquisition of shares by one company in another company is regulated by Section 186.

Section 186 governs inter-corporate investments, loans, guarantees, and securities, and lays down limits and approval requirements for such acquisitions.

Section 235 and 236 of the Companies Act, 2013

For takeovers of unlisted companies carried out through the transfer of an undertaking from one company to another:

The applicable provisions are Sections 235 and 236 of the Companies Act, 2013.

Section 235 and 236 prescribe the legal framework and conditions for such takeover transactions.

Section 235. Power to acquire shares of shareholders dissenting from the scheme or contract approved by the majority

235(1).

A transfer scheme is proposed under which shareholders of the transferor company are offered to sell their shares to a transferee company.

This means that through the transferee makes a formal offer to those shareholders.

When checking whether the 90% acceptance level is reached, you cannot count the shares already owned by the buyer, its subsidiaries, or its nominees.

Only the shares that other shareholders agree to sell are counted toward the 90% requirement.

If within four months of the offer, shareholders holding 90% of the shares involved agree to sell, then the buyer (transferee) gets a legal right to force the remaining shareholders to sell their shares too.

So the buyer can buy out the small group that refused, even if they didn’t agree.

There are two time periods to remember:

A 4-month period to get the required 90% approval from shareholders.

After that, a 2-month period in which the buyer can send notice and complete the buyout of the remaining shareholders.

After the 4-month approval period ends, the buyer has 2 more months to act.

During this time, the buyer can send a notice to the shareholders who did not agree, telling them that it plans to compulsorily acquire their shares.

The buyer’s notice must offer the same price and terms to the dissenting shareholders that were given to the shareholders who agreed earlier.

If the offer starts on Day 0, the buyer has up to Day 120 to get 90% approval.

After that, from Day 121 to Day 180, the buyer can send notices to the remaining shareholders to buy their shares.

235(2).

Once the buyer sends the notice, it must buy the dissenting shareholders’ shares on the same terms as everyone else.

The dissenting shareholder can stop or change this only by applying to the Tribunal within one month of receiving the notice.

If they don’t apply, or if the Tribunal doesn’t interfere, the buyer automatically gets the right to acquire their shares.

235(3).

If no objection is raised by the Tribunal, or if the Tribunal rejects the dissenting shareholder’s application, then after one month, the transferee company must send:

A copy of the notice to the transferor company,

Along with an instrument of transfer executed on behalf of the dissenting shareholder (by a person appointed by the transferor company) and by the transferee company on its own behalf, and

Pay the price or consideration for the shares to the transferor company.

The transferor company must then:

(a) Register the transferee company as the new holder of those shares.

(b) Within one month, inform the dissenting shareholders that their shares have been transferred and the payment received on their behalf.

235(4).

Any money or consideration received by the transferor company for such shares must be kept in a separate bank account.

The company holds this amount in trust for the dissenting shareholders and must pay them within 60 days.

235(5).

For offers that were made before this Act came into force, the law allows some simplified procedures.

These changes mainly make the transfer process easier and remove some of the old technical steps that were required earlier.

Explanation

A “dissenting shareholder” refers to any shareholder who has not agreed to the scheme or refused to transfer their shares under it.

Section 236. Purchase of minority shareholding

236(1).

An acquirer, or any person acting along with the acquirer can become the registered holder of 90% or more of the company’s issued equity share capital.

This majority can be achieved through amalgamation, share exchange, conversion of securities, or any other method,

After acquiring the shares, the acquirer is required to notify the company once this 90% threshold is crossed.

The purpose of this notification is to state their intention to buy out the remaining minority shareholders.

236(2).

The acquirer or the majority shareholders must then offer to purchase the shares held by the minority shareholders at a fair price determined by a registered valuer, following the rules prescribed under this section.

236(3).

Similarly, the minority shareholders also have a right to offer their shares to the majority shareholders, asking them to buy the minority shareholding at the price determined in the same fair valuation manner.

Thus, both majority and minority shareholders have reciprocal rights.

236(4).

The majority shareholders must deposit the total amount payable for acquiring the minority shares in a separate bank account.

This bank account will be operated by the company whose shares are being transferred.

This deposit must remain for at least one year, and the payment must be made to the minority shareholders within 60 days.

If some shareholders fail to collect the payment, the company must continue to make disbursements for up to one year.

236(5).

The company acts as a transfer agent, responsible for receiving and paying the purchase price to minority shareholders.

The company is also responsible for completing the delivery and transfer of shares to the majority shareholder.

236(6).

If a minority shareholder fails to deliver the share certificates within the specified time, their shares are deemed cancelled.

The company will then be authorised to issue new shares in favour of the majority shareholder and make payment to the minority shareholder from the deposit amount.

236(7).

If the majority shareholder has already deposited the payment for minority shareholders who are deceased, untraceable, or whose legal heirs are not recorded, then:

The law preserves the rights of these shareholders or their heirs.

These shareholders or their legal heirs can claim and sell their shares for up to three years,

This three-year period is counted from the date on which the majority acquired 90% or more shareholding.

236(8).

If, after acquiring the minority shareholders’ shares, the majority shareholders later negotiate a higher sale price for their own shares then:

They are required to share the additional compensation they receive.

This extra amount must be shared proportionately with the former minority shareholders.

So that the majority does not unfairly benefit after having earlier compelled the minority to sell at a lower price.

236(9).

Even if the majority shareholder fails to buy all the remaining minority shares as required, the law does not take away the protections given to the minority.

The minority shareholders who are left out will still be protected under this section.

This protection continues even if the company’s shares get delisted, and it also continues even if the one-year deadline or any SEBI-prescribed time limit has passed.

Explanation:

The terms Acquirer and Person acting in concert are as defined under the SEBI (Substantial Acquisition of Shares and Takeovers) Regulations, 1997, meaning a person or group working together to gain control over a company’s shares.

Acquirer

An acquirer is any person or entity that seeks to obtain shares, voting rights, or control of a target company.

They may acquire these directly or indirectly, or even just agree to acquire them in the future.

They can act alone or together with others (persons acting in concert).

Person acting in Concert

Individuals or entities who co-operate with the acquirer to acquire shares, voting rights, or control of a target company.

They share a common objective or purpose of taking over or influencing the target company.

Their actions are coordinated, directly or indirectly (e.g., financing the acquisition, jointly making decisions, supporting the acquirer).

Takeover Offers under Schemes of Arrangement: Role of Sections 230(11) and 230(12) of the Companies Act, 2013

Section 230(11)

Section 230(11) specifically recognises that a scheme of compromise or arrangement may include a takeover offer.

Provided such offer is made in the manner prescribed under the Act and the relevant rules.

With respect to Listed Companies:

Section 230(11) clearly provides that any takeover offer must be conducted strictly in accordance with the regulations framed by the SEBI.

SEBI’s takeover regulations have more importance over the general scheme provisions of the Companies Act.

Section 230(12)

Section 230(12) provides a statutory remedy to any aggrieved person in relation to a takeover offer.

This remedy is available only in cases involving companies other than listed companies (since listed company takeovers are governed by SEBI regulations).

An aggrieved party may apply to the National Company Law Tribunal (NCLT) in the prescribed manner.

Upon receiving such an application, the Tribunal has the power to examine the grievance.

The Tribunal may then pass such orders as it thinks fit, depending on the facts and circumstances of the case.

PURCHASE OF MINORITY SHAREHOLDING HELD IN DEMATERIALISED FORM

Rule 26A of the Companies (Compromises, Arrangements and Amalgamations) Rules, 2016 deals with Purchase of the Minority shareholding in Demat Form.

26A(1). Verification of Minority Shareholding After Deposit of Consideration

Once the acquirer deposits an amount equal to the price of the shares proposed to be acquired under Section 236 of the Companies Act, 2013 then:

The procedural timeline under Rule 26A is triggered.

From the date of receipt of such amount, the company is required to act within a strict time limit of two weeks.

Within this two-week period, the company must verify the details of the minority shareholders whose shares are proposed to be compulsorily acquired.

The verification specifically relates to minority shareholders holding shares in dematerialised form, as opposed to physical share certificates.

This verification process typically includes confirming the identity of shareholders, their demat account details, and the number of shares held by them.

26A(2). Notice to Minority Shareholders After Verification

Applies after completion of verification under sub-rule (1).

Company must send notice to the minority shareholders concerned.

Notice may be sent by:

Registered post.

Speed post.

Courier.

Email.

Notice must clearly specify a cut-off date.

Cut-off date cannot be earlier than one month from the date of sending the notice.

On the cut-off date:

Shares of minority shareholders shall be debited from their DEMAT account, and credited to the designated DEMAT account of the company.

If specified in the notice, shares may instead be credited directly to the DEMAT account of the acquirer.

Such credit to the acquirer’s account must be completed before the cut-off date.

26A(3). Publication and Disclosure of Notice to Minority Shareholders

Applies to the notice served under sub-rule (2).

A copy of the notice must be published simultaneously.

Publication must be made in two widely circulated newspapers.

One newspaper must be in English language.

One newspaper must be in the vernacular language of the district.

Newspapers must circulate in the district where the registered office of the company is situated.

The notice must also be uploaded on the company’s website, if the company has a website.

26A(4). Intimation to Depository and Mandatory Declarations

The company must inform the depository immediately after publication of the notice under sub-rule (3).

The intimation must include details of the cut-off date.

Along with the intimation, the company shall submit declarations stating that:

(a). The corporate action is being effected in pursuance of Section 236 of the Act.

(b). The minority shareholders holding shares in dematerialised form have been informed about the corporate action.

The copy of the notice served to such shareholders and published in the newspapers is attached.

(c). The minority shareholders shall be paid by the company immediately after completion of the corporate action.

(d). Any dispute or complaints arising out of such corporate action shall be the sole responsibility of the company.

26A(5). Board Authorisation for Corporate Action and Depository Intimation

Applies for the purpose of effecting transfer of shares through corporate action.

The Board of Directors must pass an authorisation.

The Board shall authorise the Company Secretary to act for this purpose.

In the absence of the Company Secretary, the Board may authorise any other person.

The authorised person shall:

Inform the depository under sub-rule (4).

Submit all documents as may be required under the said sub-rule.

26A(6). Action by Depository on Receipt of Company Intimation

Applies upon receipt of information from the company under sub-rule (4).

The depository is responsible for effecting the transfer of shares.

The transfer relates to minority shareholders who have not voluntarily transferred their shares in favour of the acquirer.

Such shares shall be transferred through corporate action.

The shares shall be credited to the designated DEMAT account of the company.

The transfer shall be effected on the cut-off date.

After effecting the transfer, the depository shall intimate the company accordingly.

26A(7). Disbursement of Consideration to Minority Shareholders

Applies after receipt of intimation from the depository under sub-rule (6) confirming successful transfer of shares.

The company shall immediately disburse the price of the shares so transferred.

Payment shall be made to each minority shareholder.

The disbursement shall be made after deducting applicable stamp duty.

The stamp duty shall be paid by the company.

Such payment is made on behalf of the minority shareholders.

Stamp duty shall be paid in accordance with the Indian Stamp Act, 1899.

26A(8). Transfer of Shares to Acquirer After Payment

Applies after successful payment to the minority shareholders under sub-rule (7).

The company shall inform the depository accordingly.

The shares concerned are those:

Belonging to the minority shareholders.

Kept in the designated DEMAT account of the company.

Upon such intimation, the depository shall transfer these shares.

The transfer shall be made to the DEMAT account of the acquirer.

Explanation:

Continuing Obligation to Disburse Payment and Transfer Share.

This applies where disbursement of payment could not be made within the specified time.

The company shall continue to disburse payment to the entitled shareholders.

Disbursement must be completed as and when it becomes possible.

After such disbursement, the company shall initiate transfer of shares.

The shares shall be transferred to the DEMAT account of the acquirer.

26A(9). Cases Where Transfer of Shares Is Restrained

Restraint may arise due to:

An order of a Court or Tribunal, or an order of a statutory authority.

The restraint may relate to Transfer of shares, and/or payment of dividend.

It Also applies where the shares are pledged, or hypothecated, under the Depositories Act, 1996.

In such cases, the depository shall not transfer the shares of minority shareholders.

The restriction applies to transfer to the designated DEMAT account of the company under sub-rule (6).

Explanation – Cut-Off Date Falling on a Holiday

If the cut-off date falls on a holiday,

The next working day shall be deemed to be the cut-off date.

Disclosure of Financial Readiness, Shareholder Approval, and Compulsory Acquisition of Minority Shareholding

Disclosure of Availability of Cash and Consequences of Misstatement

Every offer shall contain a statement by or on behalf of the Transferee Company.

The statement must disclose the steps taken to ensure that necessary cash will be available.

This requirement applies only where the terms of acquisition under the scheme or contract provide for:

Payment of cash.

In lieu of shares of the Transferor Company proposed to be acquired.

Any person who issues a circular that:

Contains any false statement, or gives any false impression, or contains any material omission, shall be punishable with fine.

Circulation of Scheme and Approval Requirements

The scheme or contract, along with the recommendation of the Board of Directors of the Transferor Company (if any), shall be circulated.

Approval of not less than 9/10th in value of the Transferor Company must be obtained.

Such approval must be secured within 4 months from the date of circulation.

The MOA of the Transferee Company must contain an object clause: Authorising it to take over controlling shares in another company.

If the Memorandum does not contain such a provision:

The company must alter the objects clause, by convening an Extraordinary General Meeting (EGM).

The required approval need not necessarily be obtained in a general meeting of the shareholders of the Transferor Company.

Compulsory Acquisition of Minority Interest – Post Approval Stage

Once the required approval is obtained, the Transferee Company becomes eligible to exercise the right of compulsory acquisition of minority interest.

The Transferee Company shall send notice to the shareholders who have not accepted the offer (i.e., dissenting shareholders),

Intimating them of the requirement to surrender their shares.

When acquisition of shares representing not less than 90% in value is registered in the books of the Transferor Company:

The Transferor Company shall, within one month from the date of such registration:

Inform the dissenting shareholders about:

The fact of such registration.

The receipt of the amount or other consideration representing the price payable to them by the Transferee Company.

The Transferee Company, having acquired not less than 90% in value, is mandatorily required to acquire the remaining minority stake.

Accordingly, the Transferee Company shall transfer the amount or other consideration required for acquiring the minority stake to the Transferor Company.

The amount or consideration so transferred shall not be less than the terms of acquisition offered under the scheme or contract.

Any amount or other consideration received by the Transferor Company shall be:

Paid into a separate bank account.

This will be held in trust by the Transferor Company for the persons entitled to the shares in respect of which such amount or consideration is received.

Tax Implications of Takeover Under Section 235

A takeover carried out under Section 235 of the Companies Act, 2013 does not qualify as an amalgamation under the Income-tax Act, 1961.

Consequently, tax benefits available to amalgamations under the Income-tax Act are not available to such an acquisition.

The takeover does not result in the transferor company losing its identity.

Due to the continued existence of the transferor company:

Unabsorbed depreciation and accumulated losses cannot be carried forward from the transferor company to the transferee company.

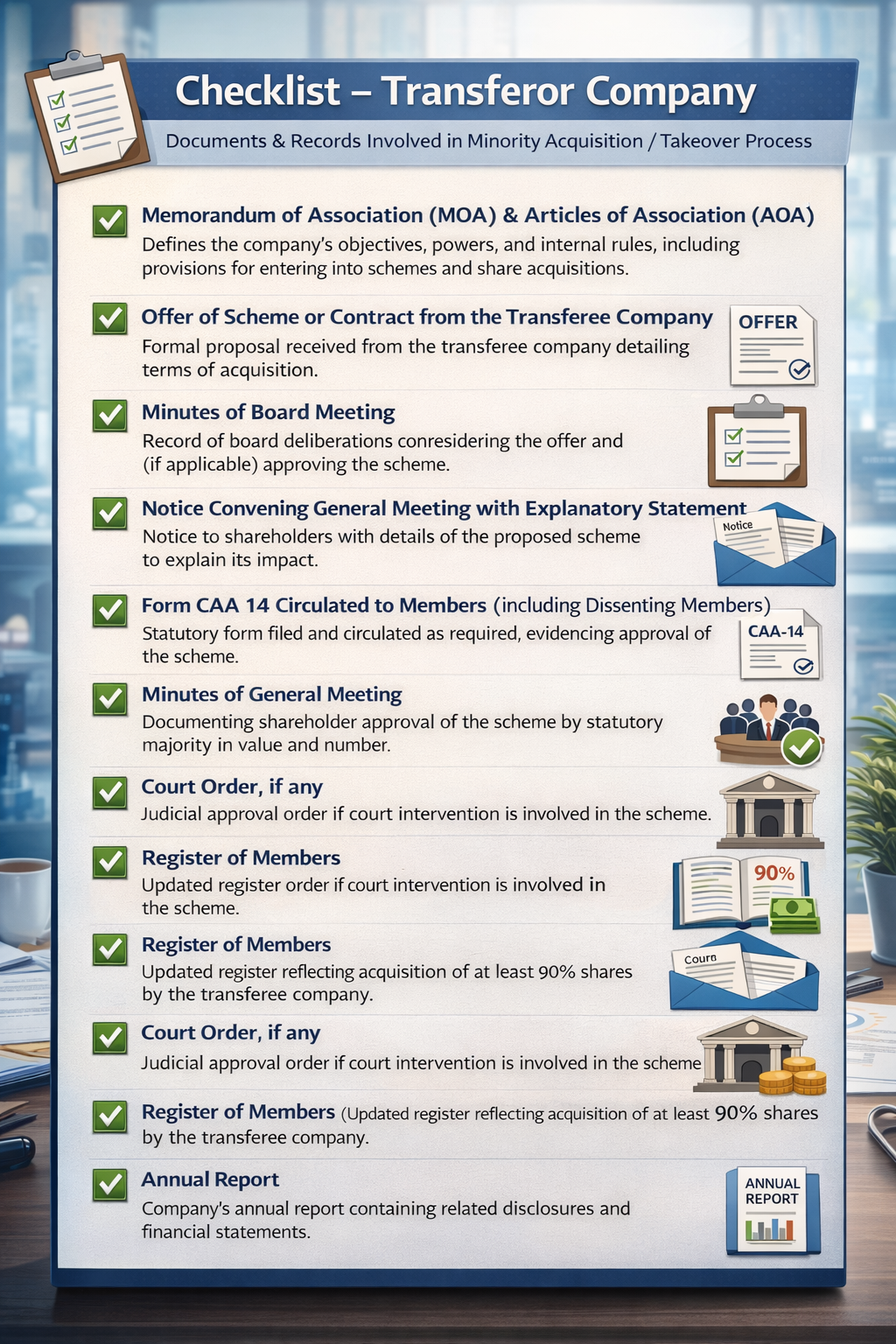

CHECK LIST FOR TRANSFEROR COMPANY

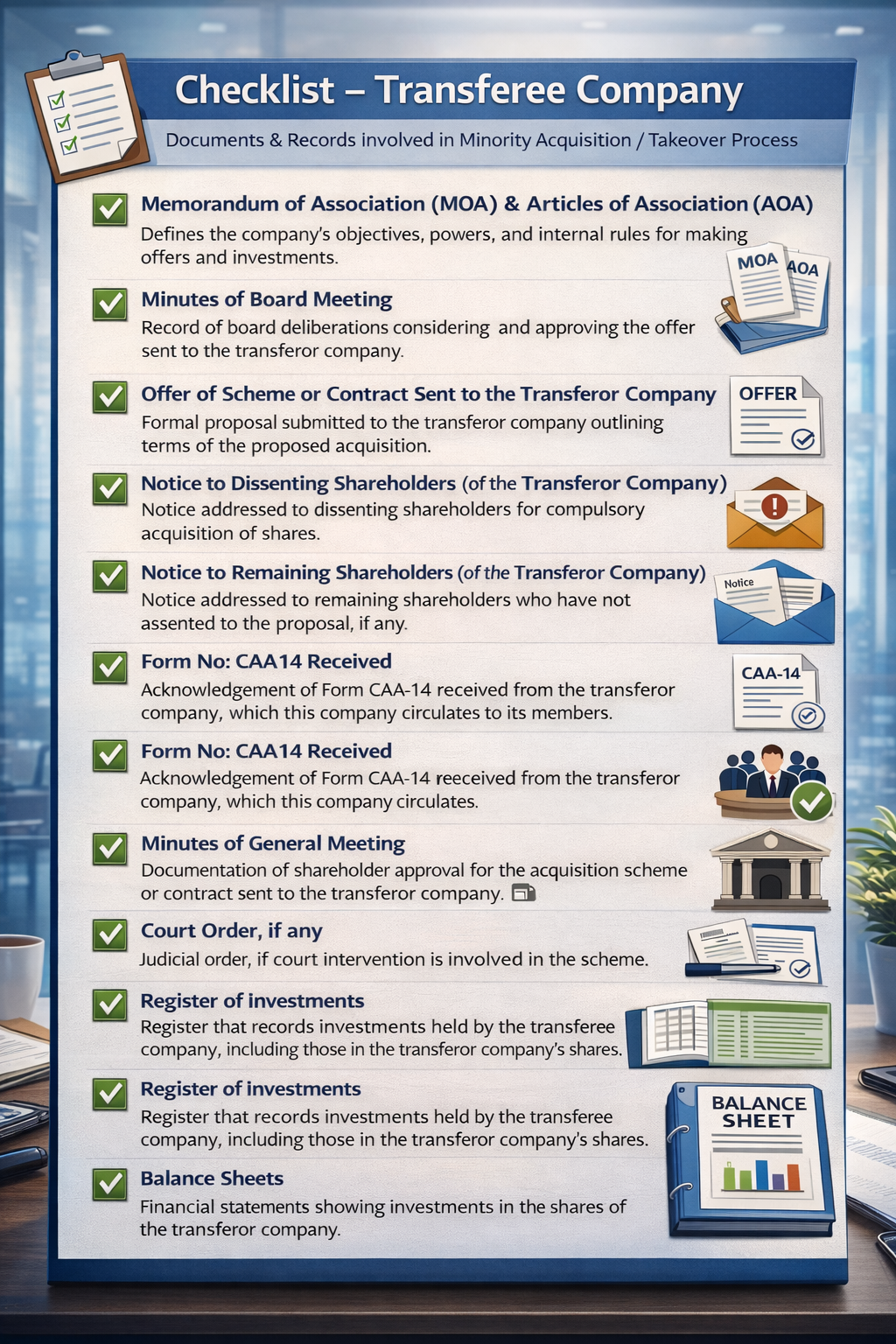

CHECK LIST FOR TRANSFEREE COMPANY