Mode of Payments

Regulation 9(1) provides the offer price may be paid, —

a) in cash;

b) by issue, exchange or transfer of listed shares in the equity share capital of the acquirer or of any person acting in concert;

c) by issue, exchange or transfer of listed secured debt instruments issued by the acquirer or any person acting in concert with a rating not inferior to investment grade as rated by a credit rating agency registered with the Board;

d) by issue, exchange or transfer of convertible debt securities entitling the holder thereof to acquire listed shares in the equity share capital of the acquirer or of any person acting in concert; or

e) a combination of the mode of payment of consideration stated in clause (a), clause (b), clause (c) and clause (d): Provided that where any shares have been acquired or agreed to be acquired by the acquirer and persons acting in concert with him during the fifty-two weeks immediately preceding the date of public announcement constitute more than ten per cent of the voting rights in the target company and has been paid for in cash, the open offer shall entail an option to the shareholders to require payment of the offer price in cash, and a shareholder who has not exercised an option in his acceptance shall be deemed to have opted for receiving the offer price in cash:

Provided further that in case of revision in offer price the mode of payment of consideration may be altered subject to the conndition that the component of the offer price to be paid in cash prior to such revision is not reduced.

Regulation 9(2) provides that, for the purposes of clause (b), clause (d) and clause (e) of sub-regulation (1), the shares sought to be issued or exchanged or transferred or the shares to be issued upon conversion of other securities, towards payment of the offer price, shall conform to the following requirements, —

(a) such class of shares are listed on a stock exchange and frequently traded at the time of the public announcement;

(b) such class of shares have been listed for a period of at least two years preceding the date of the public announcement;

(c) the issuer of such class of shares has redressed at least ninety five per cent. of the complaints received from investors by the end of the calendar quarter immediately preceding the calendar month in which the public announcement is made;

(d) the issuer of such class of shares has been in material compliance with the listing regulations for a period of at least two years immediately preceding the date of the public announcement: Provided that in case where the Board is of the view that a company has not been materially compliant with the provisions of the listing regulations, the offer price shall be paid in cash only;

(e) the impact of auditors’ qualifications, if any, on the audited accounts of the issuer of such shares for three immediately preceding financial years does not exceed five per cent. of the net profit or loss after tax of such issuer for the respective years; and (f) the Board has not issued any direction against the issuer of such shares not to access the capital market or to issue fresh shares

Regulation 9(3) provides that, where the shareholders have been provided with options to accept payment in cash or by way of securities, or a combination thereof, the pricing for the open offer may be different for each option subject to compliance with minimum offer price requirements under regulation 8:

Provided that the detailed public statement and the letter of offer shall contain justification for such differential pricing. Regulation 9(4) provides that, in the event the offer price consists of consideration to be paid by issuance of securities, which requires compliance with any applicable law, the acquirer shall ensure that such compliance is completed not later than the commencement of the tendering period:

Provided that in case the requisite compliance is not made by such date, the acquirer shall pay the entire consideration in cash.

Regulation 9(5) provides that where listed securities are offered as consideration, the value of such securities shall be higher of:

i. the average of the weekly high and low of the closing prices of such securities quoted on the stock exchange during the six months preceding the relevant date;

ii. the average of the weekly high and low of the closing prices of such securities quoted on the stock exchange during the two weeks preceding the relevant date; and

iii. the volume-weighted average market price for a period of sixty trading days preceding the date of the public announcement, as traded on the stock exchange where the maximum volume of trading in the shares of the company whose securities are being offered as consideration, are recorded during the six-month period prior to relevant date and the ratio of exchange of shares shall be duly certified by an independent merchant banker (other than the manager to the open offer) or an independent chartered accountant having a minimum experience of ten years.

Explanation.— For the purposes of this sub-regulation, the “relevant date” shall be the thirtieth day prior to the date on which the meeting of shareholders is held to consider the proposed issue of shares under sub-section (1A) of Section 81 of the Companies Act, 2013.

Regulation 9(6) states that the effect on the price of the listed equity shares, which are offered as consideration, due to material price movement and confirmation of reported event or information may be excluded as per the framework specified under sub-regulation (11) of regulation 30 of the listing regulations for determination of the price of such equity shares under this regulation.

GENERAL EXEMPTIONS

Under Regulation 10(1) the following acquisitions shall be exempt from the obligation to make an open offer under regulation 3 and regulation 4 subject to fulfillment of the conditions stipulated therefor,—

a) acquisition pursuant to inter se transfer of shares amongst qualifying persons, being,—

i. immediate relatives;

ii. persons named as promoters in the shareholding pattern filed by the target company in terms of the listing regulations or as the case may be, the listing agreement or these regulations for not less than three years prior to the proposed acquisition;

iii. a company, its subsidiaries, its holding company, other subsidiaries of such holding company, persons holding not less than fifty per cent of the equity shares of such company, other companies in which such persons hold not less than fifty per cent of the equity shares, and their subsidiaries subject to control over such qualifying persons being exclusively held by the same persons;

Explanation: For the purpose of this sub-clause, the company shall include a body corporate, whether Indian or foreign.

iv. persons acting in concert for not less than three years prior to the proposed acquisition, and disclosed as such pursuant to filings under the listing regulations or as the case may be, the listing agreement;

v. shareholders of a target company who have been persons acting in concert for a period of not less than three years prior to the proposed acquisition and are disclosed as such pursuant to filings under the 35[listing regulations or as the case may be, the listing agreement], and any company in which the entire equity share capital is owned by such shareholders in the same proportion as their holdings in the target company without any differential entitlement to exercise voting rights in such company:

Provided that for purposes of availing of the exemption under this clause,—

(a) If the shares of the target company are frequently traded, the acquisition price per share shall not be higher by more than twenty-five per cent of the volume-weighted average market price for a period of sixty trading days preceding the date of issuance of notice for the proposed inter se transfer under sub-regulation (5), as traded on the stock exchange where the maximum volume of trading in the shares of the target company are recorded during such period, and if the shares of the target company are infrequently traded, the acquisition price shall not be higher by more than twenty- five percent of the price determined in terms of clause (e) of sub-regulation (2) of regulation 8; and

(b) the transferor and the transferee shall have complied with applicable disclosure requirements set out in Chapter V.

b) acquisition in the ordinary course of business by,—

i. an underwriter registered with the Board by way of allotment pursuant to an underwriting agreement in terms of the Securities and Exchange Board of India (Issue of Capital and Disclosure Requirements) Regulations, 2009;

ii. a stock broker registered with the Board on behalf of his client in exercise of lien over the shares purchased on behalf of the client under the bye-laws of the stock exchange where such stock broker is a member

; iii. a merchant banker registered with the Board or a nominated investor in the process of market making or subscription to the unsubscribed portion of issue in terms of Chapter XB of the Securities and Exchange Board of India (Issue of Capital and Disclosure Requirements) Regulations, 2009;

iv. any person acquiring shares pursuant to a scheme of safety net in terms of regulation 44 of the Securities and Exchange Board of India (Issue of Capital and Disclosure Requirements) Regulations, 2009;

v. a merchant banker registered with the Board acting as a stabilising agent or by the promoter or pre-issue shareholder in terms of regulation 45 of the Securities and Exchange Board of India (Issue of Capital and Disclosure Requirements) Regulations, 2009;

vi. by a registered market-maker of a stock exchange in respect of shares for which he is the market maker during the course of market making; vii. a Scheduled Commercial Bank, acting as an escrow agent; and

viii. invocation of pledge by Scheduled Commercial Banks or Public Financial Institutions as a pledgee

c) acquisitions at subsequent stages, by an acquirer who has made a public announcement of an open offer for acquiring shares pursuant to an agreement of disinvestment, as contemplated in such agreement:

Provided that,—

i. both the acquirer and the seller are the same at all the stages of acquisition; and

ii. full disclosures of all the subsequent stages of acquisition, if any, have been made in the public announcement of the open offer and in the letter of offer.

d) acquisition pursuant to a scheme,—

i. made under section 18 of the Sick Industrial Companies (Special Provisions) Act, 1985 or any statutory modification or re-enactment thereto; ii. of arrangement involving the target company as a transferor company or as a transferee company, or reconstruction of the target company, including amalgamation, merger or demerger

iii. pursuant to an order of a court or a tribunal under any law or regulation, Indian or foreign; or iv. of arrangement not directly involving the target company as a transferor company or as a transferee company, or reconstruction not involving the target company’s undertaking, including amalgamation, merger or demerger, pursuant to an order of a court or a tribunal or under any law or regulation, Indian or foreign, subject to,—

(a) the component of cash and cash equivalents in the consideration paid being less than twenty-five per cent of the consideration paid under the scheme; and

(b) where after implementation of the scheme of arrangement, persons directly or indirectly holding at least thirty-three per cent of the voting rights in the combined entity are the same as the persons who held the entire voting rights before the implementation of the scheme.

da) acquisition pursuant to a resolution plan approved under section 31 of the Insolvency and Bankruptcy Code, 2016;

e) acquisition pursuant to the provisions of the Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002 ;

f) acquisition pursuant to the provisions of the Delisting Regulations; g) acquisition by way of transmission, succession or inheritance;

h) acquisition of voting rights or preference shares carrying voting rights arising out of the operation of sub-section (2) of section 47 of the Companies Act, 2013;

i) Acquisition of shares by the lenders pursuant to conversion of their debt as part of a debt restructuring implemented in accordance with the guidelines specified by the Reserve Bank of India: Provided that the conditions specified under sub-regulation (6) of regulation 158 of the Securities and Exchange Board of India (Issue of Capital and Disclosure Requirements) Regulations, 2018 are complied with

Explanation. – For the purpose of this clause, “lenders” shall mean all scheduled commercial banks (excluding Regional Rural Banks) and All India Financial Institutions. j) increase in voting rights arising out of the operation of sub-section (1) of section 106 of the Companies Act, 2013 or pursuant to a forfeiture of shares by the target company, undertaken in compliance with the provisions of the Companies Act, 2013 and its articles of association.

(2A) An increase in the voting rights of any shareholder beyond the threshold limits stipulated in sub-regulations (1) and (2) of regulation 3, without the acquisition of control, pursuant to the conversion of equity shares with superior voting rights into ordinary equity shares, shall be exempted from the obligation to make an open offer under regulation 3.

(2B) Any acquisition of shares or voting rights or control of the target company by way of preferential issue in compliance with regulation 164A of the Securities and Exchange Board of India (Issue of Capital and Disclosure Requirements) Regulations, 2018 shall be exempt from the obligation to make an open offer under sub- regulation (1) of regulation 3 and regulation 4.

Explanation.- The above exemption from open offer shall also apply to the target company with infrequently traded shares which is compliant with the provisions of sub- regulations (2), (3), (4), (5),(6), (7) and (8) of regulation 164A of the Securities and Exchange Board of India (Issue of Capital and Disclosure Requirements) Regulations, 2018. The pricing of such infrequently traded shares shall be in terms of regulation 165 of the Securities and Exchange Board of India (Issue of Capital and Disclosure Requirements) Regulations, 2018.

How is the offer price calculated in case shares are infrequently traded on the stock exchange? ‘

If the target company’s shares are infrequently traded, then the open offer price for acquisition of shares under the minimum open offer shall be highest of the following: Highest negotiated price per share under the share purchase agreement (“SPA”) triggering the offer; Volume weighted average price of shares acquired by the acquirer during 52 weeks preceding the public announcement (“PA”); Highest price paid for any acquisition by the acquirer during 26 weeks immediately preceding the PA; The price determined by the acquirer and the manager to the open offer after taking into account valuation parameters including book value, comparable trading multiples, and such other parameters that are customary for valuation of shares of such companies. It may be noted that the Board may at the expense of the acquirer, require valuation of shares by an independent merchant banker other than the manager to the offer or any independent chartered accountant in practice having a minimum experience of 10 years.

Under Regulation 10(3), an increase in voting rights in a target company of any shareholder beyond the limit attracting an obligation to make an open offer under sub-regulation (1) of regulation 3, pursuant to buy-back of shares by the target company shall be exempt from the obligation to make an open offer provided such shareholder reduces his shareholding such that his voting rights fall to below the threshold referred to in subregulation (1) of regulation 3 within ninety days from the date of the closure of the said buy-back offer

Under Regulation 10(4), the following acquisitions shall be exempt from the obligation to make an open offer under sub-regulation (2) of regulation 3, —’

a) acquisition of shares by any shareholder of a target company, upto his entitlement, pursuant to a rights issue;

b) acquisition of shares by any shareholder of a target company, beyond his entitlement, pursuant to a rights issue, subject to fulfillment of the following conditions,

— i. the acquirer has not renounced any of his entitlements in such rights issue; and

ii. the price at which the rights issue is made is not higher than the ex-rights price of the shares of the target company, being the sum of,—

A. the volume weighted average market price of the shares of the target company during a period of sixty trading days ending on the day prior to the date of determination of the rights issue price, multiplied by the number of shares outstanding prior to the rights issue, divided by the total number of shares outstanding after allotment under the rights issue: Provided that such volume weighted average market price shall be determined on the basis of trading on the stock exchange where the maximum volume of trading in the shares of such target company is recorded during such period; and

B. the price at which the shares are offered in the rights issue, multiplied by the number of shares so offered in the rights issue divided by the total number of shares outstanding after allotment under the rights issue:

c) increase in voting rights in a target company of any shareholder pursuant to buy- back of shares:

Provided that,—

i. such shareholder has not voted in favour of the resolution authorising the buy-back of securities under section 68 of the Companies Act, 2013;

ii. in the case of a shareholder resolution, voting is by way of postal ballot;

iii. where a resolution of shareholders is not required for the buy- back, such shareholder, in his capacity as a director, or any other interested director has not voted in favour of the resolution of the board of directors of the target company authorising the buy-back of securities under section 68 of the Companies Act, 2013; and

iv. the increase in voting rights does not result in an acquisition of control by such shareholder over the target company:

Provided further that where the aforesaid conditions are not met, in the event such shareholder reduces his shareholding such that his voting rights fall below the level at which the obligation to make an open offer would be attracted under sub-regulation (2) of regulation 3, within ninety days from the date of closure of the buy-back offer by the target company, the shareholder shall be exempt from the obligation to make an open offer.

d) acquisition of shares in a target company by any person in exchange for shares of another target company tendered pursuant to an open offer for acquiring shares under these regulations;

e) acquisition of shares in a target company from state-level financial institutions or their subsidiaries or companies promoted by them, by promoters of the target company pursuant to an agreement between such transferors and such promoter;

f) acquisition of shares in a target company from a venture capital fund or category I Alternative Investment Fund or a foreign venture capital investor registered with the Board, by promoters of the target company pursuant to an agreement between such venture capital fund or category I Alternative Investment Fund or foreign venture capital investor and such promoters.

Under Regulation 10(5), acquisitions under clause (a) of sub-regulation (1), and clauses (e) and (f) of subregulation (4), the acquirer shall intimate the stock exchanges where the shares of the target company are listed, the details of the proposed acquisition in such form as may be specified, at least four working days prior to the proposed acquisition, and the stock exchange shall forthwith disseminate such information to the public.

Under Regulation 10(6), any acquisition made pursuant to exemption provided for in this regulation, the acquirer shall file a report with the stock exchanges where the shares of the target company are listed, in such form as may be specified not later than four working days from the acquisition, and the stock exchange shall forthwith disseminate such information to the public.

Under Regulation 10(7), any acquisition of or increase in voting rights pursuant to exemption provided for in clause (a) of sub-regulation (1), sub-clause (iii) of clause (d) of sub- regulation (1), clause (h) of sub-regulation (1), sub-regulation (2), sub-regulation (3) and clause (c) of sub-regulation (4), clauses (a), (b) and (f) of sub-regulation (4), the acquirer shall, within twenty-one working days of the date of acquisition, submit a report in such form as may be specified along with supporting documents to the Board giving all details in respect of acquisitions, along with a non-refundable fee of rupees one lakh fifty thousand by way of direct credit in the bank account through NEFT/RTGS/IMPS or any other mode allowed by RBI or by way of a banker’s cheque or demand draft payable in Mumbai in favour of the Board.

Explanation.— For the purposes of sub-regulation (5), sub-regulation (6) and sub- regulation (7) in the case of convertible securities, the date of the acquisition shall be the date of conversion of such securities.;

What are the threshold limits for acquisition of shares / voting rights, beyond which an obligation to make an open offer is triggered?

Acquisition of 25% or more shares or voting rights: An acquirer, who (along with PACs, if any) holds less than 25% shares or voting rights in a target company and agrees to acquire shares or acquires shares which along with his/ PAC’s existing shareholding would entitle him to exercise 25% or more shares or voting rights in a target company, will need to make an open offer before acquiring such additional shares. Acquisition of more than 5% shares or voting rights in a financial year: An acquirer who (along with PACs, if any) holds 25% or more but less than the maximum permissible non-public shareholding in a target company, can acquire additional shares in the target company as would entitle him to exercise more than 5% of the voting rights in any financial year ending March 31, only after making an open offer.

Exemptions by the Board

According to Regulation 11(1), the Board may for reasons recorded in writing, grant exemption from the obligation to make an open offer for acquiring shares under these regulations subject to such conditions as the Board deems fit to impose in the interests of investors in securities and the securities market.

According to Regulation 11(2), the Board may for reasons recorded in writing, grant a relaxation from strict compliance with any procedural requirement under Chapter III and Chapter IV subject to such conditions as the Board deems fit to impose in the interests of investors in securities and the securities market on being satisfied that,—

a) the target company is a company in respect of which the Central Government or State Government or any other regulatory authority has superseded the board of directors of the target company and has appointed new directors under any law for the time being in force, if,—

i. such board of directors has formulated a plan which provides for transparent, open, and competitive process for acquisition of shares or voting rights in, or control over the target company to secure the smooth and continued operation of the target company in the interests of all stakeholders of the target company and such plan does not further the interests of any particular acquirer;

ii. the conditions and requirements of the competitive process are reasonable and fair;

iii. the process adopted by the board of directors of the target company provides for details including the time when the open offer for acquiring shares would be made, completed and the manner in which the change in control would be effected; and

b) the provisions of Chapter III and Chapter IV are likely to act as impediment to implementation of the plan of the target company and exemption from strict compliance with one or more of such provisions is in public interest, the interests of investors in securities and the securities market.

According to Regulation 11(3), for seeking exemption under sub-regulation (1), the acquirer shall, and for seeking relaxation under sub-regulation (2) the target company shall file an application with the Board, supported by a duly sworn affidavit, giving details of the proposed acquisition and the grounds on which the exemption has been sought.

According to Regulation 11(4), the acquirer or the target company, as the case may be, shall along with the application referred to under sub-regulation (3) pay a non-refundable fee of rupees five lakh, by way of direct credit in the bank account through NEFT/RTGS/IMPS or any other mode allowed by RBI or by way of a banker’s cheque or demand draft payable in Mumbai in favour of the Board.

According to Regulation 11(5), the Board may after affording reasonable opportunity of being heard to the applicant and after considering all the relevant facts and circumstances, pass a reasoned order either granting or rejecting the exemption or relaxation sought as expeditiously as possible:

Provided that the Board may constitute a panel of experts to which an application for an exemption under sub-regulation (1) may, if considered necessary, be referred to make recommendations on the application to the Board.

According to Regulation 11(6), the order passed under sub-regulation (5) shall be hosted by the Board on its official website.

Open Offer Proces

Manager to the Open Offer

Regulation 12(1) states that, prior to making a public announcement, the acquirer shall appoint a merchant banker registered with the Board, who is not an associate of the acquirer, as the manager to the open offer.

Explanation.— For the purposes of this regulation the term “associate” has the same meaning as in the Securities and Exchange Board of India (Merchant Bankers) Regulations, 1992.

Regulation 12(2) states that, the public announcement of the open offer for acquiring shares required under these regulations shall be made by the acquirer through such manager to the open offer.

Timingg

Regulation 13(1) states that, the public announcement referred to in regulation 3 and regulation 4 shall be made in accordance with regulation 14 and regulation 15, on the date of agreeing to acquire shares or voting rights in, or control over the target company

Regulation 13(2) states that, such public announcement,— a) in the case of market purchases, shall be made prior to placement of the purchase order with the stock broker to acquire the shares, that would take the entitlement to voting rights beyond the stipulated thresholds; b) pursuant to an acquirer acquiring shares or voting rights in, or control over the target company upon converting convertible securities without a fixed date of conversion or upon conversion of depository receipts for the underlying shares of the target company shall be made on the same day as the date of exercise of the option to convert such securities into shares of the target company; c) pursuant to an acquirer acquiring shares or voting rights in, or control over the target company upon conversion of convertible securities with a fixed date of conversion shall be made on the second working day preceding the scheduled date of conversion of such securities into shares of the target company; d) pursuant to a disinvestment shall be made on the same day as the date of executing the agreement for acquisition of shares or voting rights in or control over the target company; e) in the case of indirect acquisition of shares or voting rights in, or control over the target company where none of the parameters referred to in sub-regulation (2) of regulation 5 are met, may be made at any time within four working days from the earlier of, the date on which the primary acquisition is contracted, and the date on which the intention or the decision to make the primary acquisition is announced in the public domain; f) in the case of indirect acquisition of shares or voting rights in, or control over the target company where any of the parameters referred to in sub- regulation (2) of regulation 5 are met shall be made on the earlier of, the date on which the primary acquisition is contracted, and the date on which the intention or the decision to make the primary acquisition is announced in the public domain; g) pursuant to an acquirer acquiring shares or voting rights in, or control over the target company, under preferential issue, shall be made on the date on which the board of directors of the target company authorises such preferential issue;

h) the public announcement pursuant to an increase in voting rights consequential to a buy-back not qualifying for exemption under regulation 10, shall be made not later than the ninetieth day from the date of closure of the buy-back offer by the target company; i) the public announcement pursuant to any acquisition of shares or voting rights in or control over the target company where the specific date on which title to such shares, voting rights or control is acquired is beyond the control of the acquirer, shall be made not later than two working days from the date of receipt of intimation of having acquired such title.

Regulation 13(2A) states that, notwithstanding anything contained in sub-regulation (2), a public announcement referred to in regulation 3 and regulation 4 for a proposed acquisition of shares or voting rights in or control over the target company through a combination of,- i. an agreement and any one or more modes of acquisition referred to in sub- regulation (2) of regulation 13, or ii. any one or more modes of acquisition referred in clause (a) to (i) of sub-regulation(2) of regulation 13, shall be made on the date of first such acquisition, provided the acquirer discloses in the public announcement the details of the proposed subsequent acquisition.

Regulation 13(3) states that, the public announcement made under regulation 6 shall be made on the same day as the date on which the acquirer takes the decision to voluntarily make a public announcement of an open offer for acquiring shares of the target company. Regulation 13(3) states that, pursuant to the public announcement made under sub-regulation (1) and sub- regulation (3), a detailed public statement shall be published by the acquirer through the manager to the open offer in accordance with regulation 14 and regulation 15, not later than five working days of the public announcement: Provided that the detailed public statement pursuant to a public announcement made under clause (e) of subregulation (2) shall be made not later than five working days of the completion of the primary acquisition of shares or voting rights in, or control over the company or entity holding shares or voting rights in, or control over the target company. Explanation.— It is clarified that in the event the acquirer does not succeed in acquiring the ability to exercise or direct the exercise of voting rights in, or control over the target company, the acquirer shall not be required to make a detailed public statement of an open offer for acquiring shares under these regulations.

Publication

Under Regulation 14(1), the public announcement shall be sent to all the stock exchanges on which the shares of the target company are listed, and the stock exchanges shall forthwith disseminate such information to the public. Under Regulation 14(2), a copy of the public announcement shall be sent to the Board and to the target company at its registered office within one working day of the date of the public announcement. Under Regulation 14(3), the detailed public statement pursuant to the public announcement referred to in subregulation (4) of regulation 13 shall be published in all editions of any one English national daily with wide circulation, any one Hindi national daily with wide circulation, and any one regional language daily with wide circulation at the place where the registered office of the target company is situated and one regional language daily at the place of the stock exchange where the maximum volume of trading in the shares of the target company are recorded during the sixty trading days preceding the date of the public announcement'

Under Regulation 14(4), simultaneously with publication of such detailed public statement in the newspapers, a copy of the same shall be sent to,— i. the Board through the manager to the open offer, ii. all the stock exchanges on which the shares of the target company are listed, and the stock exchanges shall forthwith disseminate such information to the public, iii. the target company at its registered office, and the target company shall forthwith circulate it to the members of its board.’’

Contents

According to Regulation 15(1), the public announcement shall contain such information as may be specified, including the following,—

a) name and identity of the acquirer and persons acting in concert with him;

b) name and identity of the sellers, if any;

c) nature of the proposed acquisition such as purchase of shares or allotment of shares, or any other means of acquisition of shares or voting rights in, or control over the target company;

d) the consideration for the proposed acquisition that attracted the obligation to make an open offer for acquiring shares, and the price per share, if any;

e) the offer price, and mode of payment of consideration;

f) offer size, and conditions as to minimum level of acceptances, if any; and

g) intention of the acquirer to either delist the target company or retain the listing of the target company. In case of proposed delisting under regulation 5A, the proposed open offer price and indicative price as required under regulation 5A shall be disclosed along with an explanation setting out the rationale and basis for justifying the indicative price.

According to Regulation 15(2), the detailed public statement pursuant to the public announcement shall contain such information as may be specified in order to enable shareholders to make an informed decision with reference to the open offer.

According to Regulation 15(3), the public announcement of the open offer, the detailed public statement, and any other statement, advertisement, circular, brochure, publicity material or letter of offer issued in relation to the acquisition of shares under these regulations shall not omit any relevant information, or contain any misleading information

FILING OF LETTER OF OFFER WITH BOARD

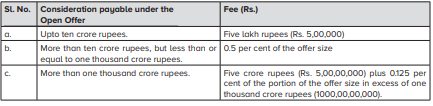

Regulation 16(1) provides that, within five working days from the date of the detailed public statement made under sub-regulation (4) of regulation 13, the acquirer shall, through the manager to the open offer, file with the Board, a draft of the letter of offer containing such information as may be specified along with a non-refundable fee, as per the following scale, by way of direct credit in the bank account through NEFT/RTGS/IMPS or any other mode allowed by RBI or by way of a banker’s cheque or demand draft payable in Mumbai in favour of the Board,—

Regulation 16(2) provides that, the consideration payable under the open offer shall be calculated at the offer price, assuming full acceptance of the open offer, and in the event the open offer is subject to differential pricing, shall be computed at the highest offer price, irrespective of manner of payment of the consideration:

Provided that in the event of consideration payable under the open offer being enhanced owing to a revision to the offer price or offer size the fees payable shall stand revised accordingly, and shall be paid within five working days from the date of such revision.

Regulation 16(3) provides that, the manager to the open offer shall provide soft copies of the public announcement, the detailed public statement and the draft letter of offer in accordance with such specifications as may be specified, and the Board shall upload the same on its website.

Regulation 16(4) provides that, the Board shall give its comments on the draft letter of offer as expeditiously as possible but not later than fifteen working days of the receipt of the draft letter of offer and in the event of no comments being issued by the Board within such period, it shall be deemed that the Board does not have comments to offer:

Provided that in the event the Board has sought clarifications or additional information from the manager to the open offer, the period for issuance of comments shall be extended to the fifth working day from the date of receipt of satisfactory reply to the clarification or additional information sought.

Provided further that in the event the Board specifies any changes, the manager to the open offer and the acquirer shall carry out such changes in the letter of offer before it is dispatched to the shareholders.

Regulation 16(5) provides that, in the case of competing offers, the Board shall provide its comments on the draft letter of offer in respect of each competing offer on the same day. Regulation 16(6) provides that, in the event the disclosures in the draft letter of offer are inadequate the Board may call for a revised letter of offer and shall deal with the revised letter of offer in accordance with sub-regulation (4).

What is a letter of offer? What are the disclosures required under the Letter of offer?

The letter of offer is a document which is dispatched to all shareholders of the target company as on identified date. This is also made available on the website of SEBI. Letter of offer contains details about the offer, background of Acquirers/PACS, financial statements of Acquirer/ PACs, escrow arrangement, background of the target company, financial statements of the target company, justification for offer price, financial arrangements, terms and conditions of the offer, procedure for acceptance and settlement of the offer. SEBI has prescribed the format for Letter of offer, which enumerates minimum disclosure requirements. The Manager to the offer/ acquirer is free to add any other disclosures which in his opinion are material for the shareholders. The format is available in the SEBI website.

Provision of escrow

Under Regulation 17(1), not later than two working days prior to the date of the detailed public statement of the open offer for acquiring shares, the acquirer shall create an escrow account towards security for performance of his obligations under these regulations, and deposit in escrow account such aggregate amount as per the following scale:

Provided that where an open offer is made conditional upon minimum level of acceptance, hundred percent of the consideration payable in respect of minimum level of acceptance or fifty per cent of the consideration payable under the open offer, whichever is higher, shall be deposited in cash in the escrow account.

Provided further that in case of indirect acquisitions where public announcement has been made in terms of clause (e) of sub-regulation (2) of regulation 13 of these regulations, an amount equivalent to hundred per cent of the consideration payable in the open offer shall be deposited in the escrow account.

Under Regulation 17(2), the consideration payable under the open offer shall be computed as provided for in sub-regulation (2) of regulation 16 and in the event of an upward revision of the offer price or of the offer size, the value of the escrow amount shall be computed on the revised consideration calculated at such revised offer price, and the additional amount shall be brought into the escrow account prior to effecting such revision.

Under Regulation 17(3), the escrow account referred to in sub-regulation (1) may be in the form of,—

a) cash deposited with any scheduled commercial bank;

b) bank guarantee issued in favour of the manager to the open offer by any scheduled commercial bank; or

c) deposit of frequently traded and freely transferable equity shares or other freely transferable securities with appropriate margin: Provided that securities sought to be provided towards escrow account under clause (c) shall be required to conform to the requirements set out in sub-regulation (2) of regulation 9.

Provided further that the deposit of securities shall not be permitted in respect of indirect acquisitions where public announcement has been made in terms of clause (e) of sub-regulation (2) of regulation 13 of these regulations Explanation: The cash component of the escrow account as referred to in clause above may be maintained in an interest bearing account, subject to the merchant banker ensuring that the funds are available at the time of making payment to the shareholders

Under Regulation 17(4), in the event of the escrow account being created by way of a bank guarantee or by deposit of securities, the acquirer shall also ensure that at least one per cent of the total consideration payable is deposited in cash with a scheduled commercial bank as a part of the escrow account.

Under Regulation 17(5), for such part of the escrow account as is in the form of a cash deposit with a scheduled commercial bank, the acquirer shall while opening the account, empower the manager to the open offer to instruct the bank to issue a banker’s cheque or demand draft or to make payment of the amounts lying to the credit of the escrow account, in accordance with requirements under these regulations.

Under Regulation 17(6), for such part of the escrow account as is in the form of a bank guarantee, such bank guarantee shall be in favour of the manager to the open offer and shall be kept valid throughout the offer period and for an additional period of thirty days after completion of payment of consideration to shareholders who have tendered their shares in acceptance of the open offer.

Under Regulation 17(7), for such part of the escrow account as is in the form of securities, the acquirer shall empower the manager to the open offer to realise the value of such escrow account by sale or otherwise, and in the event there is any shortfall in the amount required to be maintained in the escrow account, the manager to the open offer shall be liable to make good such shortfall.

Under Regulation 17(8), the manager to the open offer shall not release the escrow account until the expiry of thirty days from the completion of payment of consideration to shareholders who have tendered their shares in acceptance of the open offer, save and except for transfer of funds to the special escrow account as required under regulation 21.

Under Regulation 17(9), in the event of non-fulfilment of obligations under these regulations by the acquirer the Board may direct the manager to the open offer to forfeit the escrow account or any amounts lying in the special escrow account, either in full or in part

Under Regulation 17(10), the escrow account deposited with the bank in cash shall be released only in the following manner,—

a) the entire amount to the acquirer upon withdrawal of offer in terms of regulation 23 as certified by the manager to the open offer:

Provided that in the event the withdrawal is pursuant to clause (c) of sub-regulation (1) of regulation 23, the manager to the open offer shall release the escrow account upon receipt of confirmation of such release from the Board;

b) for transfer of an amount not exceeding ninety per cent of the escrow account, to the special escrow account in accordance with regulation 21;

c) to the acquirer, the balance of the escrow account after transfer of cash to the special escrow account, on the expiry of thirty days from the completion of payment of consideration to shareholders who have tendered their shares in acceptance of the open offer, as certified by the manager to the open offer;

d) the entire amount to the acquirer upon the expiry of thirty days from the completion of payment of consideration to shareholders who have tendered their shares in acceptance of the open offer, upon certification by the manager to the open offer, where the open offer is for exchange of shares or other secured instruments;

e) the entire amount to the manager to the open offer, in the event of forfeiture for non-fulfillment of any of the obligations under these regulations, for distribution in the following manner, after deduction of expenses, if any, of registered market intermediaries associated with the open offer,—

i. one third of the escrow account to the target company;

ii. one third of the escrow account to the Investor Protection and Education Fund established under the Securities and Exchange Board of India (Investor Protection and Education Fund) Regulations, 2009; and

iii. one third of the escrow account to be distributed pro-rata among the shareholders who have accepted the open offer.

OTHER PROCEDURES

Regulation 18(1) provides simultaneously with the filing of the draft letter of offer with the Board under subregulation (1) of regulation 16, the acquirer shall send a copy of the draft letter of offer to the target company at its registered office address and to all stock exchanges where the shares of the target company are listed.

Regulation 18(2) provides the letter of offer shall be dispatched to the shareholders whose names appear on the register of members of the target company as of the identified date, not later than seven working days from the receipt of comments from the Board or where no comments are offered by the Board, within seven working days from the expiry of the period stipulated in sub-regulation (4) of regulation 16:

Explanation:

i. Letter of offer may also be dispatched through electronic mode in accordance with the provisions of Companies Act, 2013.

ii. On receipt of a request from any shareholder to receive a copy of the letter of offer in physical format, the same shall be provided.

iii. The aforesaid shall be disclosed in the letter of offer

Provided that where local laws or regulations of any jurisdiction outside India may expose the acquirer or the target company to material risk of civil, regulatory or criminal liabilities in the event the letter of offer in its final form were to be sent without material amendments or modifications into such jurisdiction, and the shareholders resident in such jurisdiction hold shares entitling them to less than five per cent of the voting rights of the target company, the acquirer may refrain from dispatch of the letter of offer into such jurisdiction:

Provided further that every person holding shares, regardless of whether he held shares on the identified date or has not received the letter of offer, shall be entitled to tender such shares in acceptance of the open offer.

Regulation 18(3) provides simultaneously with the dispatch of the letter of offer in terms of sub-regulation (2), the acquirer shall send the letter of offer to the custodian of shares underlying depository receipts, if any, of the target company.

Regulation 18(4) provides irrespective of whether a competing offer has been made, an acquirer may make upward revisions to the offer price, and subject to the other provisions of these regulations, to the number of shares sought to be acquired under the open offer, at any time prior to the commencement of the last one working day before the commencement of the tendering period.

Regulation 18(5) provides that in the event of any revision of the open offer, whether by way of an upward revision in offer price, or of the offer size, the acquirer shall,—

a. make corresponding increases to the amount kept in escrow account under regulation 17 prior to such revision;

b. make an announcement in respect of such revisions in all the newspapers in which the detailed public statement pursuant to the public announcement was made; and

c. simultaneously with the issue of such an announcement, inform the Board, all the stock exchanges on which the shares of the target company are listed, and the target company at its registered office.

Regulation 18(6) provides the acquirer shall disclose during the offer period every acquisition made by the acquirer or persons acting in concert with him of any shares of the target company in such form as may be specified, to each of the stock exchanges on which the shares of the target company are listed and to the target company at its registered office within twenty-four hours of such acquisition, and the stock exchanges shall forthwith disseminate such information to the public

Provided that the acquirer and persons acting in concert with him shall not acquire or sell any shares of the target company during the period between three working days prior to the commencement of the tendering period and until the expiry of the tendering period.

Also, the acquirer shall facilitate tendering of shares by the shareholders and settlement of the same, through the stock exchange mechanism as specified by the Board.

Regulation 18(7) provides the acquirer shall issue an advertisement in such form as may be specified, one working day before the commencement of the tendering period, announcing the schedule of activities for the open offer, the status of statutory and other approvals, if any, whether for the acquisition attracting the obligation to make an open offer under these regulations or for the open offer, unfulfilled conditions, if any, and their status, the procedure for tendering acceptances and such other material detail as may be specified:

Provided that such advertisement shall be,—

a. published in all the newspapers in which the detailed public statement pursuant to the public announcement was made; and

b. simultaneously sent to the Board, all the stock exchanges on which the shares of the target company are listed, and the target company at its registered office.

Regulation 18(8) provides the tendering period shall start not later than twelve working days from date of receipt of comments from the Board under sub-regulation (4) of regulation 16 and shall remain open for ten working days.

Regulation 18(9) provides the shareholders who have tendered shares in acceptance of the open offer shall not be entitled to withdraw such acceptance during the tendering period.

Regulation 18(10) provides that, the acquirer shall, within ten working days from the last date of the tendering period, complete all requirements under these regulations and other applicable law relating to the open offer including payment of consideration to the shareholders who have accepted the open offer.

Regulation 18(11) provides that, the acquirer shall be responsible to pursue all statutory approvals required by the acquirer in order to complete the open offer without any default, neglect or delay:

Provided that where the acquirer is unable to make the payment to the shareholders who have accepted the open offer within such period owing to non- receipt of statutory approvals required by the acquirer, the Board may, where it is satisfied that such non-receipt was not attributable to any willful default, failure or neglect on the part of the acquirer to diligently pursue such approvals, grant extension of time for making payments, subject to the acquirer agreeing to pay interest to the shareholders for the delay at such rate as may be specified:

Provided further that where the statutory approval extends to some but not all shareholders, the acquirer shall have the option to make payment to such shareholders in respect of whom no statutory approvals are required in order to complete the open offer. It also states that, without prejudice to sub-regulation 11, in case the acquirer is unable to make payment to the shareholders who have accepted the open offer within such period, the acquirer shall pay interest for the period of delay to all such shareholders whose shares have been accepted in the open offer, at the rate of ten per cent per annum

Provided that in case the delay was not attributable to any act of omission or commission of the acquirer, or due to the reasons or circumstances beyond the control of acquirer, the Board may grant waiver from the payment of interest.

Provided further that the payment of interest would be without prejudice to the Board taking any action under regulation 32 of these regulation or under the Act. Sub clause 12 states that, the acquirer shall issue a post offer advertisement in such form as may be specified within five working days after the offer period, giving details including aggregate number of shares tendered, accepted, date of payment of consideration.

Such advertisement shall be,—

i. published in all the newspapers in which the detailed public statement pursuant to the public announcement was made; and

ii. simultaneously sent to the Board, all the stock exchanges on which the shares of the targ1et company are listed, and the target company at its registered office.