Registration of Charges

Rule 2. Definitions

(1).

In these rules, unless the context otherwise requires:

(a). Act means the Companies Act, 2013.

(b). Annexure means the Annexure appended to these rules.

(c). Fees means the fees as specified in the Companies (Registration offices and fees) Rules, 2014.

(d). Form’’ or e-forms means form set forth in Annexure to these rules which shall be used for the matter to which it relates.

(e). Regional Director means the person appointed by the Central Government in the Ministry of Corporate Affairs as a Regional ‘Director.

(f). Section means the section of the Act.

(2).

Words and expressions used in these rules but they are not defined here but

They are defined in the Act or in Companies (Specification of definitions details) Rules, 2014 then those meanings would apply the same here.

Rule 3. Registration of creation or modification of charge.

(1).

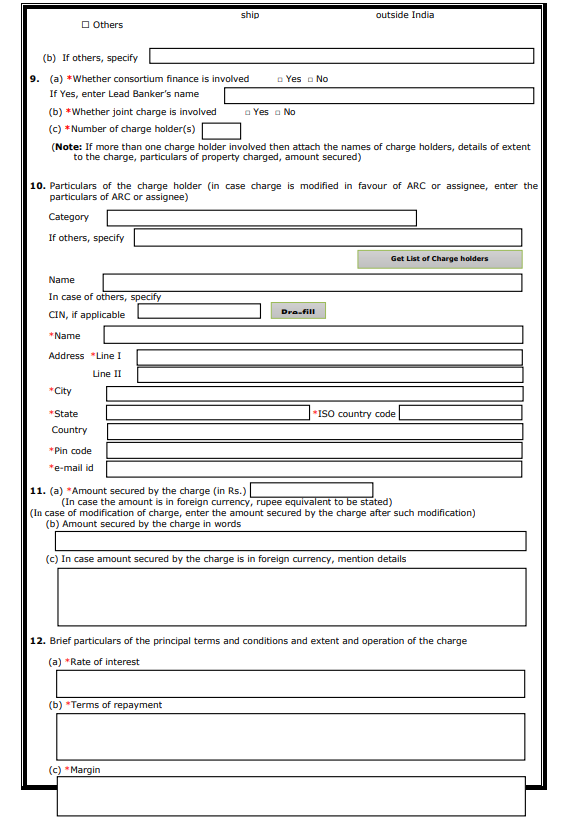

For registering a charge under Section 77(1), Section 78, or Section 79, the company must file the required particulars of the charge.

These particulars must be accompanied by a copy of the instrument, if any, that creates or modifies the charge.

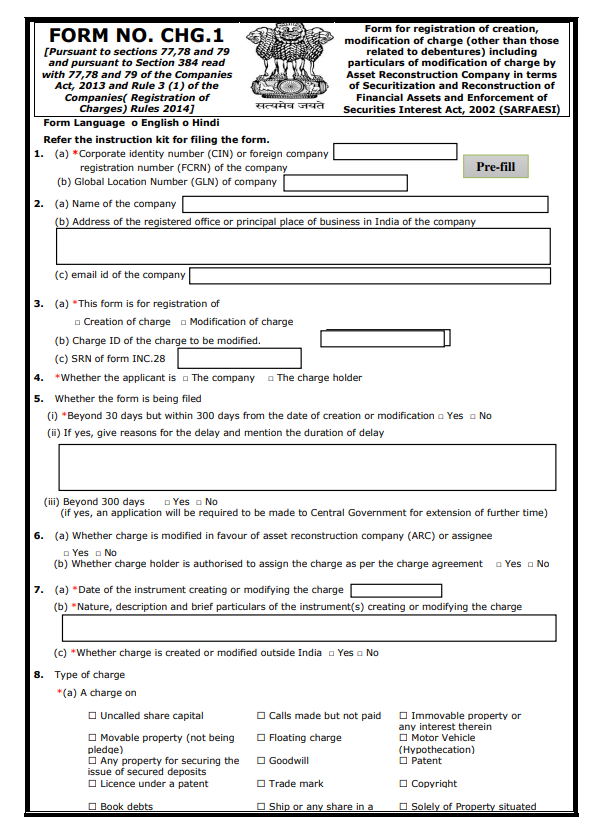

The filing must be done in Form No. CHG-1 when the charge relates to assets other than debentures.

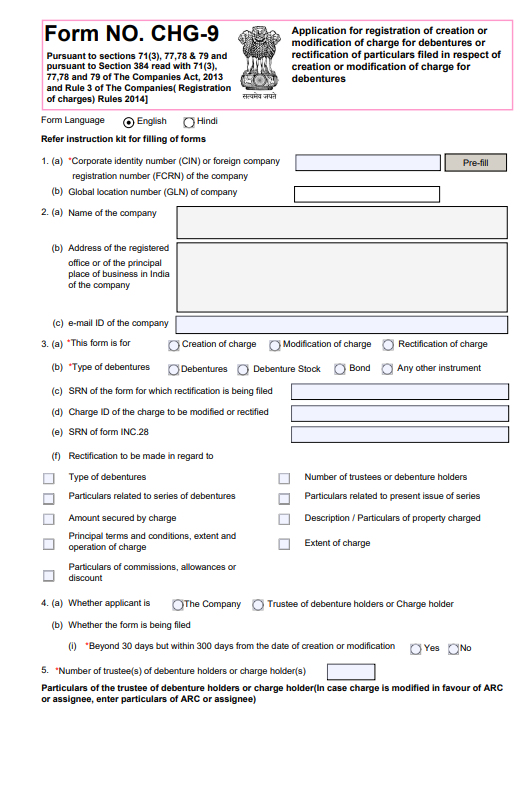

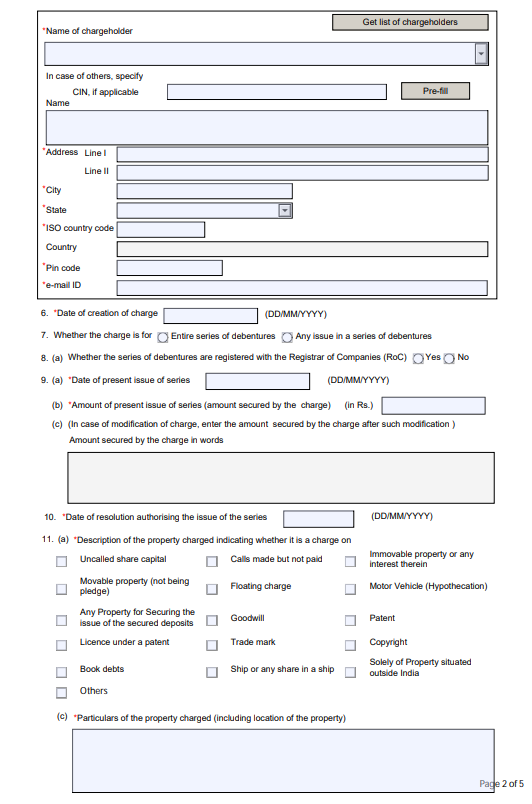

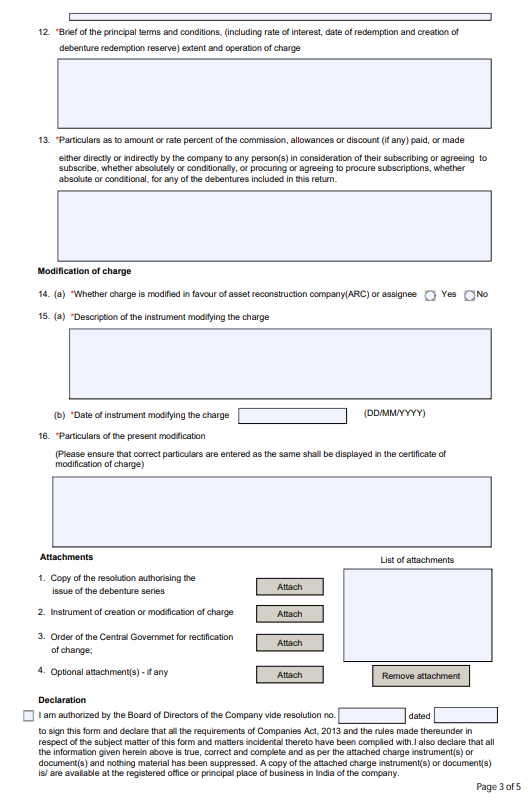

The filing must be done in Form No. CHG-9 when the charge relates to debentures.

The correct form must be chosen depending on whether the charge is connected to debentures or not.

The form must be duly signed by both:

The company, and

The charge holder (the person or entity in whose favour the charge is created).

These documents must be filed with the Registrar of Companies (RoC).

The filing must take place within 30 days from the date of creation or modification of the charge.

The required prescribed fee must also be paid along with the filing.

(2).

If the particulars of a charge are not filed within the initial 30-day period as required under Rule 3 (1), the filing can still be done later.

In such cases, the creation or modification of the charge must be filed in Form No. CHG-1 (For charges other than debentures).

For charges relating to debentures, the filing must be done in Form No. CHG-9.

This delayed filing must be completed within the extended period allowed under Section 77 of the Companies Act.

The company must pay the additional fee prescribed for late filing.

In applicable cases, the company must also pay the ad valorem fee as specified in the Companies (Registration Offices and Fees) Rules, 2014.

Ad Valorem means according to the value.

These additional fees are required because the filing is being made after the original time limit.

(3).

If the company fails to register the charge within the required time as stated in Rule 3(1), the charge-holder has the right to apply for registration.

In such a situation, the registration of the charge is completed based on the charge-holder’s application, not the company’s.

The charge-holder may have to pay fees, additional fees, or ad valorem fees to the Registrar in order to get the charge registered.

After paying these amounts, the charge-holder is entitled to recover the entire amount paid from the company.

(4).

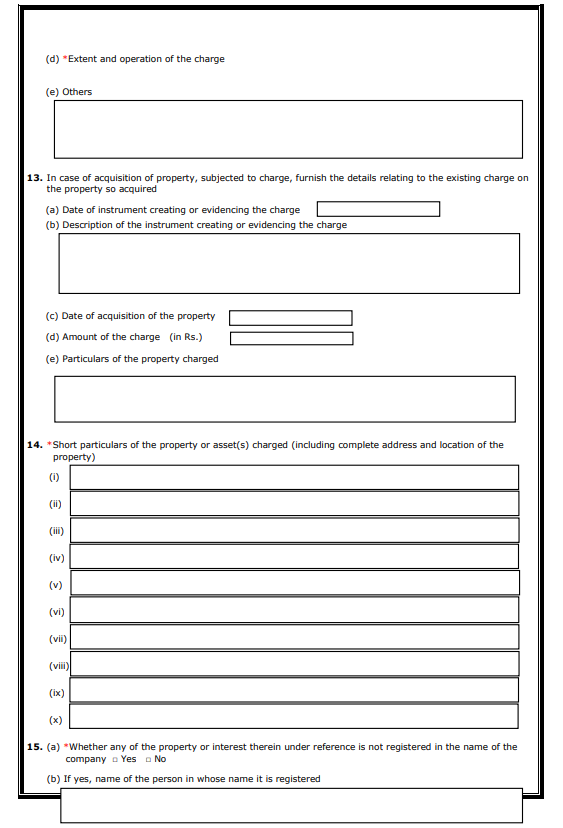

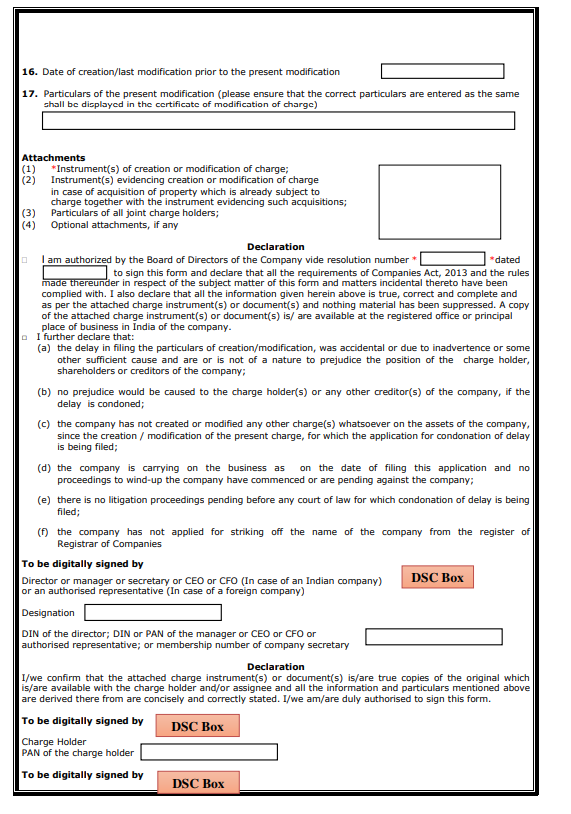

A copy of every instrument that evidences the creation or modification of a charge must be filed with the Registrar as required under Sections 77, 78, or 79.

Such copies must be verified before filing, and the method of verification depends on whether the property is located inside or outside India.

(a). Verification when the property is situated outside India:

If the instrument or deed relates solely to property outside India, the copy must be verified by a certificate issued in any of the following ways:

Under the seal of the company (if the company has a seal).

Under the signature of any director of the company.

Under the signature of the company secretary.

Under the signature of an authorised officer of the charge holder.

Under the signature of any person (other than the company) who is interested in the mortgage or charge.

(5).

The rule does not apply to certain types of charges.

Specifically, it does not apply to charges created or modified by a banking company under Section 77 of the Companies Act.

This exemption applies when the charge is created in favour of the Reserve Bank of India (RBI).

The exemption is triggered when the RBI has given the banking company a loan or advance.

Such loan or advance must be made under sub-clause (d) of clause (4) of section 17 of the Reserve Bank of India Act, 1934.

Therefore, when a banking company creates or modifies a charge in favour of RBI in these circumstances, the normal requirements of this rule do not apply.

Note: Please note that all the CHG forms 1 and 9 are to be filed online.

To Access Form CHG -1: https://ca2013.com/wp-content/uploads/2015/07/chg-1.pdf

To Access Form CHG -9: https://ca2013.com/wp-content/uploads/2015/08/Form_CHG-9.pdf

Rule 4. Application to Registrar

(1).

This rule applies for the purposes of:

The first proviso to Section 77(1).

Clause (b) of the second proviso to Section 77(1).

It deals with situations where a company fails to file the particulars of a charge and the instrument of charge, if any, within the initial 30-day period from the date of creation or modification of the charge.

The Registrar has the power to allow late registration if the company had sufficient cause for not filing within the first 30 days.

The Registrar must be satisfied that the reason for delay is genuine and justified.

If satisfied, the Registrar may permit the charge to be registered after 30 days.

However, the registration must still take place within the extended period allowed under the provisos to Section 77(1).

The company must pay the prescribed fee for registration.

In addition, the company must pay the additional fee applicable for delayed filing.

Where required, the company must also pay ad valorem fees as per the Companies (Registration Offices and Fees) Rules, 2014.

These fees compensate for the delay and ensure compliance with the statutory timelines

(2).

When a company applies for late registration of a charge under Rule 4(1), it must use the appropriate form.

The application must be filed in Form No. CHG-1 (for charges other than debentures).

If the charge relates to debentures, the application must be filed in Form No. CHG-9.

The application must be supported by a declaration from the company.

This declaration must be signed either by the company secretary or by a director of the company.

The declaration must state that the belated filing (late submission of charge particulars) will not adversely affect the rights of any other intervening creditors.

Filing this declaration is mandatory for the Registrar to consider and allow the late registration of the charge.

Rule 5. Application of rules in certain matters.

Rule 4 provisions will also apply mutatis mutandis to:

Registration of a charge on any property that is acquired with an existing (pre-attached) charge.

Modification of an existing charge under Section 79 of the Act.

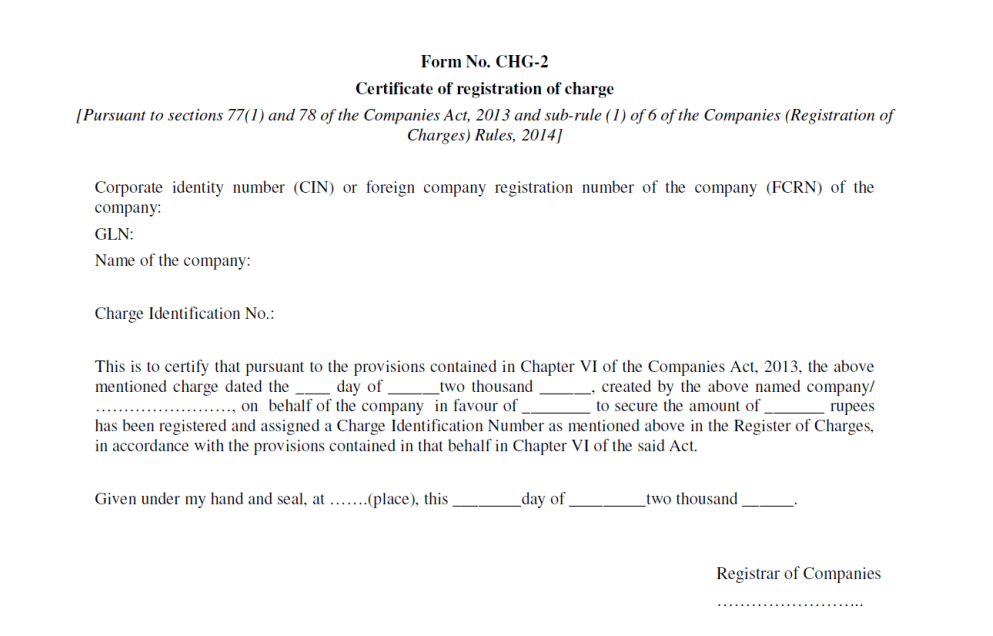

Rule 6. Certificate of registration.

(1).

When a charge is registered with the Registrar under Section 77(1) or Section 78, a certificate must be issued.

The responsibility to issue this certificate lies with the Registrar of Companies (RoC).

The certificate confirms the registration of the charge.

The certificate must be issued in Form No. CHG-2.

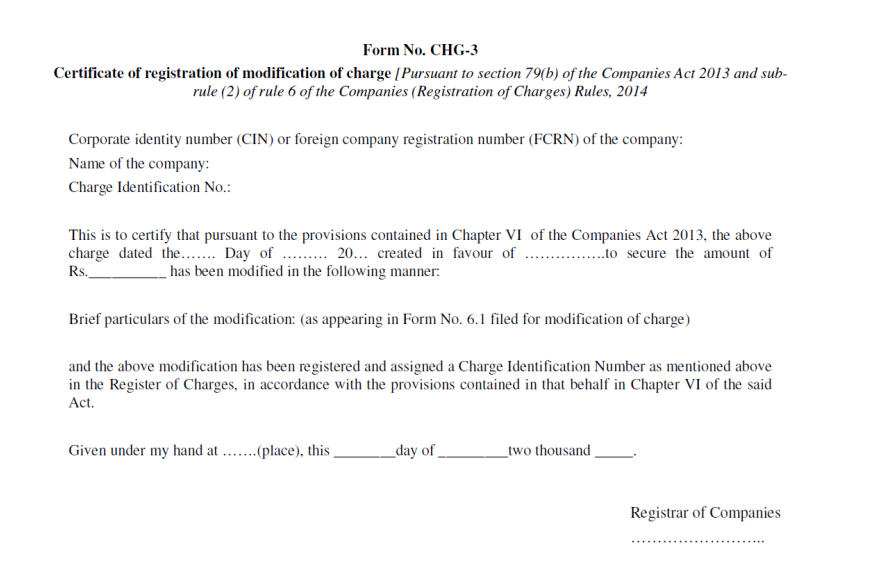

(2).

When the particulars of modification of a charge are registered under Section 79, the Registrar must issue a certificate.

The responsibility to issue this certificate lies with the Registrar of Companies (RoC).

The certificate confirms that the modification of the charge has been officially registered.

The certificate must be issued in Form No. CHG-3.

(3).

The Registrar issues certificates under:

6(1) - Certificate of registration of charge (Form CHG-2).

6(2) - Certificate of modification of charge (Form CHG-3).

These certificates are treated as conclusive evidence.

Once the certificate is issued, it is legally accepted without requiring further proof.

The certificate confirms that all requirements of Chapter VI of the Companies Act have been complied with.

It also confirms compliance with all rules made under Chapter VI regarding:

Creation of a charge.

Modification of a charge.

So, after issuance of the certificate, no one can dispute that the statutory requirements for registration have been fulfilled.

To Access Form CHG -2: https://ca2013.com/returns/chg-3/

To Access Form CHG -3: https://ca2013.com/returns/chg-3/

Rule 7. Register of charges to be kept by the Registrar.

(1).

The Ministry of Corporate Affairs (MCA) maintains the particulars of charges on its online portal: www.mca.gov.in/MCA21.

These electronically maintained charge records are treated as the official register of charges.

This treatment is specifically for the purposes of Section 81 of the Companies Act.

Therefore, the MCA portal’s charge data is considered the legal and authoritative register.

This replaces the need for a separate physical register maintained by the Registrar.

Any person inspecting charges under Section 81 is effectively inspecting the MCA portal records, which serve as the statutory register.

(2).

These electronically stored charge records are treated as the official register of charges.

This status applies specifically for the purposes of Section 81 of the Companies Act.

Anyone inspecting charges under Section 81 is effectively inspecting the MCA portal data, which is legally recognized as the register of charges.

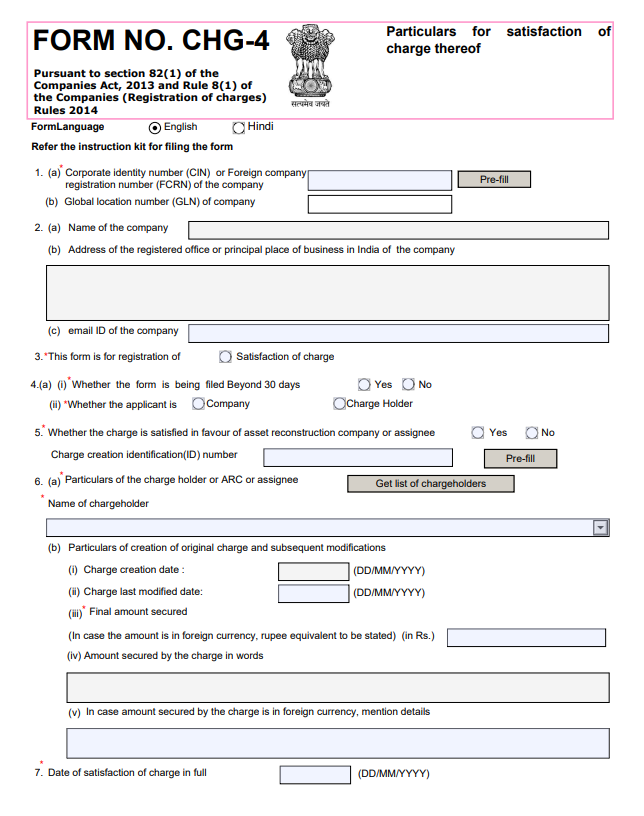

Rule 8. Satisfaction of charge.

(1).

When a charge registered under Chapter VI is paid off or fully satisfied, an intimation must be sent to the Registrar.

This obligation applies to either the company or the charge holder.

The intimation must be given within 300 days from the date of full payment or satisfaction of the charge.

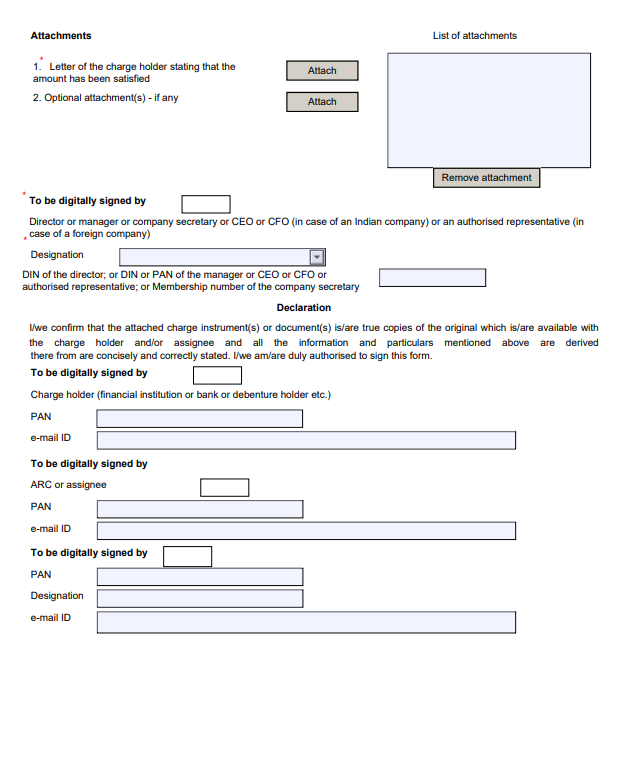

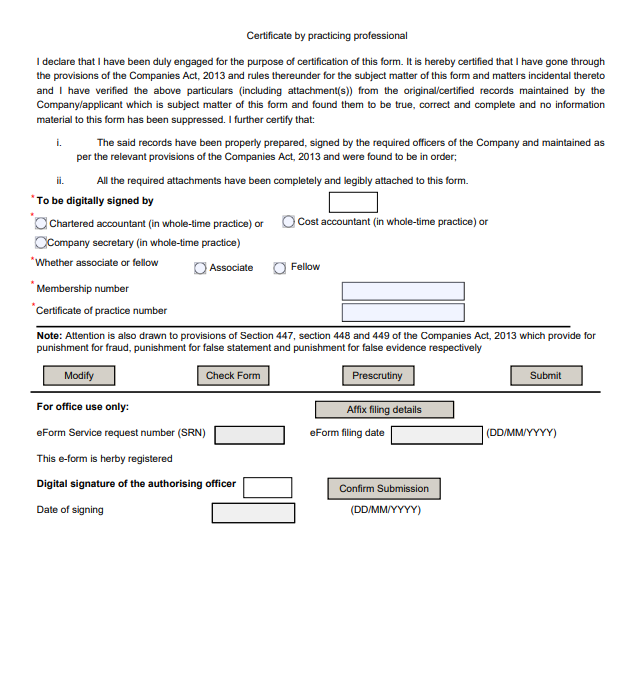

The intimation must be submitted in Form No. CHG-4.

The required prescribed fee must be paid along with the form.

This filing notifies the Registrar that the charge no longer exists and should be updated in the official records.

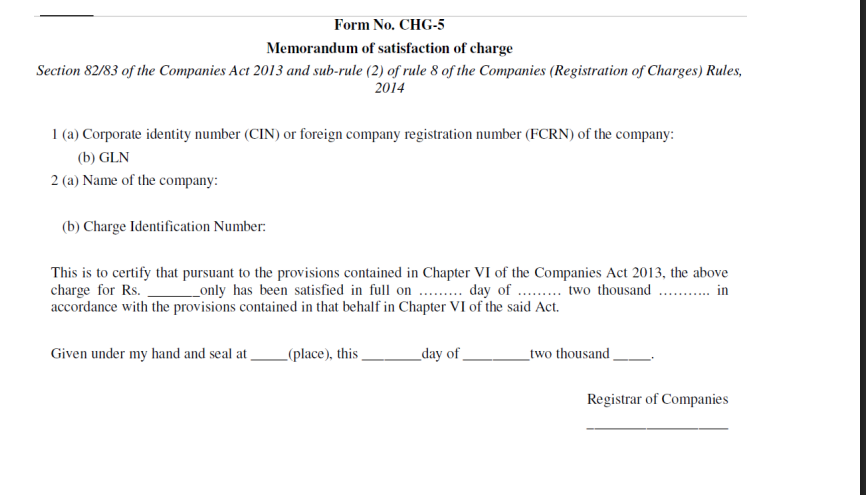

(2).

When a charge is fully satisfied and the Registrar records this by entering a memorandum of satisfaction under Section 82 or 83, a certificate must be issued.

The responsibility for issuing this certificate lies with the Registrar of Companies (RoC).

The certificate confirms the registration of satisfaction of charge.

This certificate must be issued in Form No. CHG-5.

The certificate serves as official proof that the charge has been fully discharged and is no longer active in the company’s records.

To Access Form CHG -4: https://ca2013.com/wp-content/uploads/2015/08/Form_CHG-4.pdf

Please note that the Form CHG -4 should be filed online.

To Access Form No. CHG-5: https://ca2013.com/wp-content/uploads/2015/08/CHG_5.pdf

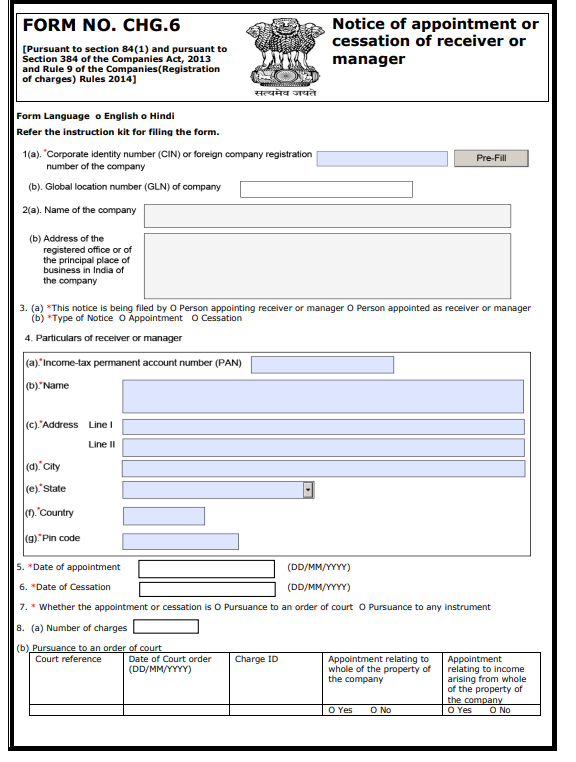

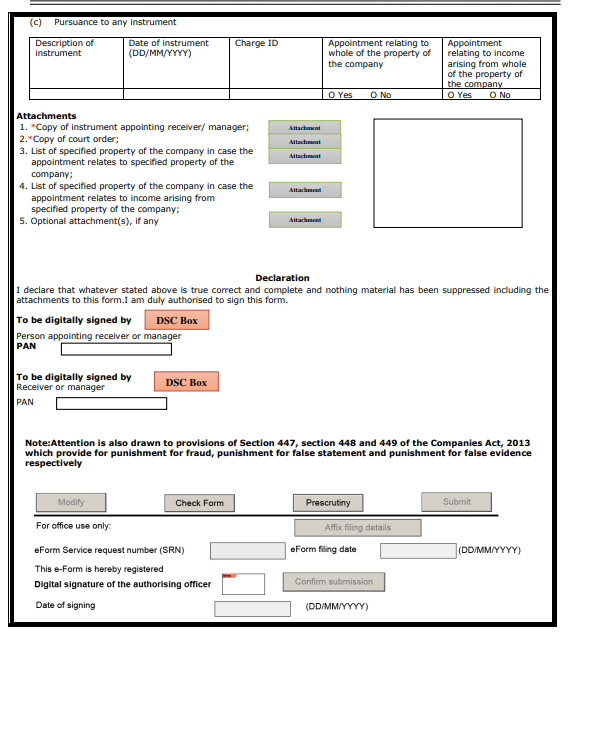

Rule 9. Intimation of appointment of Receiver or Manager

When a receiver is appointed for property that is subject to a charge then:

A notice of this appointment must be filed with the Registrar.

When a receiver ceases to hold office, a notice of such cessation must also be filed with the Registrar.

The same requirement applies when any person is appointed to manage charged property, or when such a person ceases to act.

The notice must be submitted in Form No. CHG-6.

The notice must be filed along with the prescribed fee.

A receiver is someone appointed to protect and manage assets that are charged.

They act on behalf of the charge holder when the company fails to meet its obligations.

To Access Form CHG -6: https://ca2013.com/wp-content/uploads/2015/08/chg-6.pdf

Please note that Form CHG -6 has to be filed online.

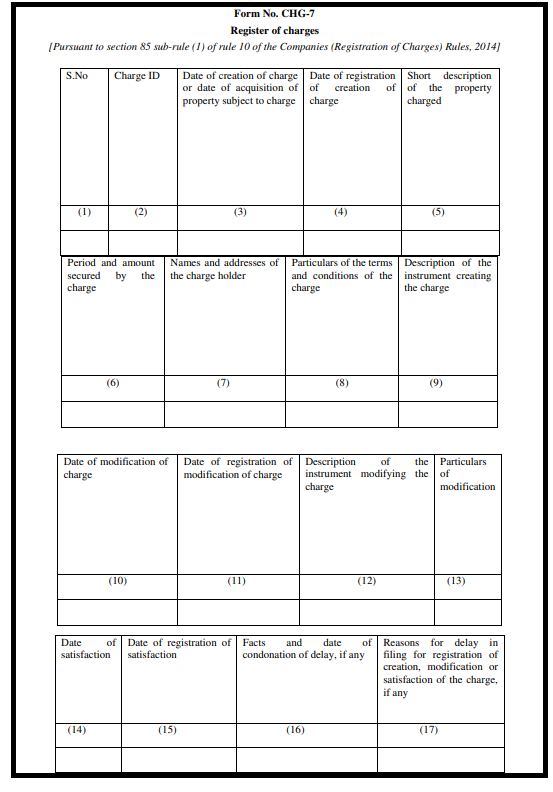

Rule 10. Company’s register of charges.

(1).

Every company is required to maintain a register of charges.

This register must be kept at the company’s registered office.

The register must be maintained in Form No. CHG-7.

The company must enter in this register the particulars of all charges that have been registered with the Registrar.

These particulars must include charges created on any property, assets, or undertaking of the company.

The register must also include particulars of any property acquired by the company that is already subject to a charge.

Further, the register must include particulars of any modification of an existing charge.

The register must also record the particulars of satisfaction of charge when the charge is fully paid off or discharged.

(2).

The company must make entries in its register of charges without delay.

The entries must be made immediately (forthwith) after any of the following events occur:

Creation of a charge.

Modification of a charge.

Satisfaction of a charge.

(3).

Entries in the register shall be authenticated by a director or the secretary of the company or any other person authorised by the Board for the purpose.

(4).

The register of charges maintained by the company must be preserved permanently.

So , the register cannot be destroyed or discarded at any time in the future.

The instrument creating a charge (Deed, agreement, mortgage document) must also be preserved.

The instrument relating to modification of a charge must likewise be preserved.

These instruments must be kept for a period of eight years.

The eight-year period is counted from the date on which the charge is fully satisfied or paid off.

To Access Form CHG -7: https://ca2013.com/register/form-no-chg-7-register-of-charges/

Please note that this form has to be filed online.

Rule 11. Register open for inspection.

The register of charges and the instruments of charges kept by the company must be made available for inspection.

These documents must be open for inspection by:

(a). Any member of the company, without payment of any fee.

(b). Any creditor of the company, also without payment of any fee.

(c). Any other person, but such a person must pay the prescribed fee to inspect the documents.

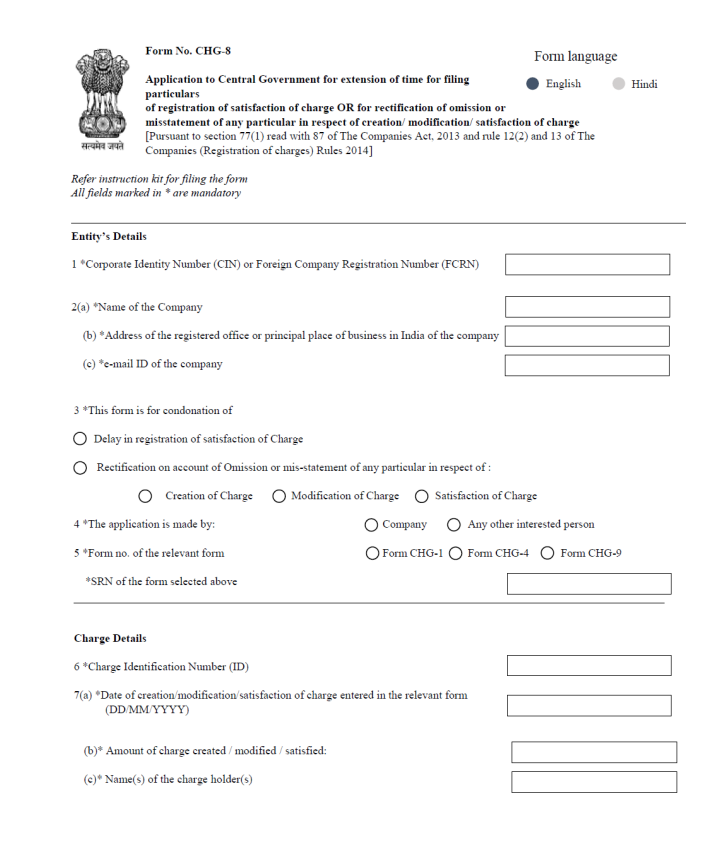

Rule 12. Rectification in register of charges on account of omission or misstatement of particulars in charge previously recorded and extension of time in filing of satisfaction of charge.

An application may be filed to the Central Government in Form No. CHG-8, as per Section 87 of the Companies Act.

Upon receiving such an application, the Central Government has the power to issue certain directions.

(a) Power to direct rectification of omissions or misstatements

The Central Government may order the correction of any omission or misstatement in filings related to charges.

This includes correcting errors in:

Particulars of a charge.

Particulars of a modification of a charge.

Any memorandum of satisfaction of charge.

Any other entry made under Section 82 or Section 83.

(b) Power to extend time for filing satisfaction of charge

If the company fails to file satisfaction of charge within 300 days from the date of full payment or satisfaction, the Central Government may grant an extension of time.

This extension allows the filing of satisfaction of charge even after the 300-day period has expired.

To Access Form No. CHG -8: https://ca2013.com/wp-content/uploads/2022/09/CHG-8.pdf

Please note that this form must be filed online.

Rule Signing of charge e-forms by insolvency resolution professional or resolution professional or liquidator for companies under resolution or liquidation.

The Forms No.

CHG-1

CHG-4

CHG-8

CHG-9

shall be signed by Insolvency resolution professional or resolution professional or liquidator for companies under resolution or liquidation, as the case may be.

Thereafter , they must be filed with the Registrar.